EMR July 2024

Dear Reader

ATTITUDES OF CENTRAL BANKS

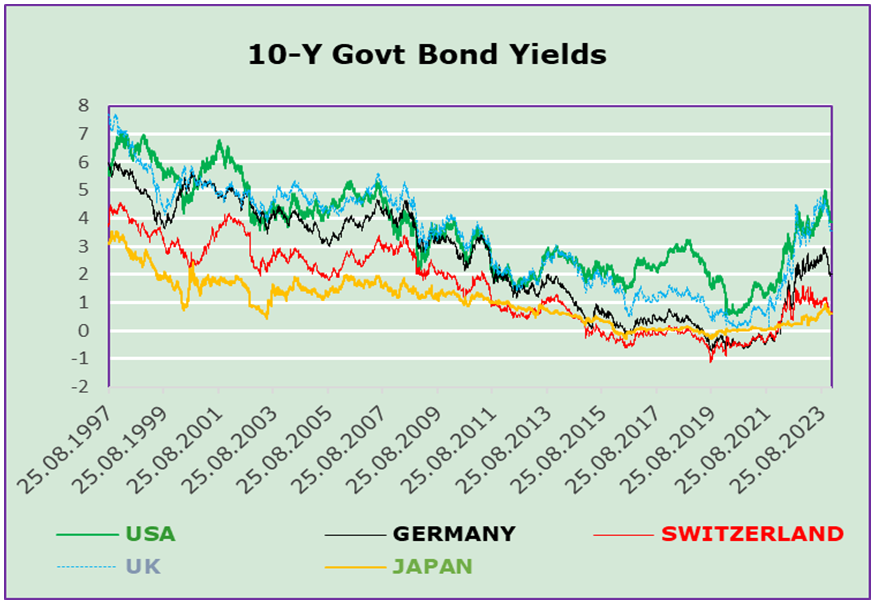

The latest actions by central banks are indeed astonishing. On 8 June 2024, the Neue Zürcher Zeitung wrote: “It rarely happens, for once the Europeans are ahead of the Americans”, citing the interest rate cuts by the Swiss National Bank and the European Central Bank. To make the connection clearer, it was the Swiss National Bank that was the first major central bank to announce an imminent turnaround, on 21 March 2024. The cut in the key interest rate by 25 basis points to 1.5% initially led to a depreciation of the CHF by 1% against the EUR. In the same period, the CHF fell by 1.2% against the USD, while the SMI rose by 0.9%. At the same time, the yield on 1-year Swiss government bonds fell by more than 20 basis points, from 1.22% to 0.99%. On 21 June 2024, the SNB confirmed the “interest rate turnaround” by lowering the interest rate again by 0.5 percentage points to 1.25%. This step confirms our assessment – for Switzerland – of how important currency changes are and can be.

On 8 June 2024, the European Central Bank (ECB) decided to change course, i.e. cut interest rates. The key interest rate was lowered by 0.25 percentage points to 4.25%. The ECB is thus following the example of the central banks in Canada, Switzerland and Sweden, which had lowered interest rates. The US Federal Reserve Board, on the other hand, decided on 12 June 2024 to postpone a reduction in the key interest rate. Chairman Powell announced that the Federal Reserve would maintain interest rates in their current range of 5.25% to 5.5%. At the same time, the forecast for interest rate cuts was revised to just one in 2024. The central bank’s policymakers noted that there had been “modest further progress” towards its 2% in-flation target. The chairman of the Federal Reserve stated during the press conference that the central bank did not yet have the confidence to cut interest rates even if inflation came back from its peak.

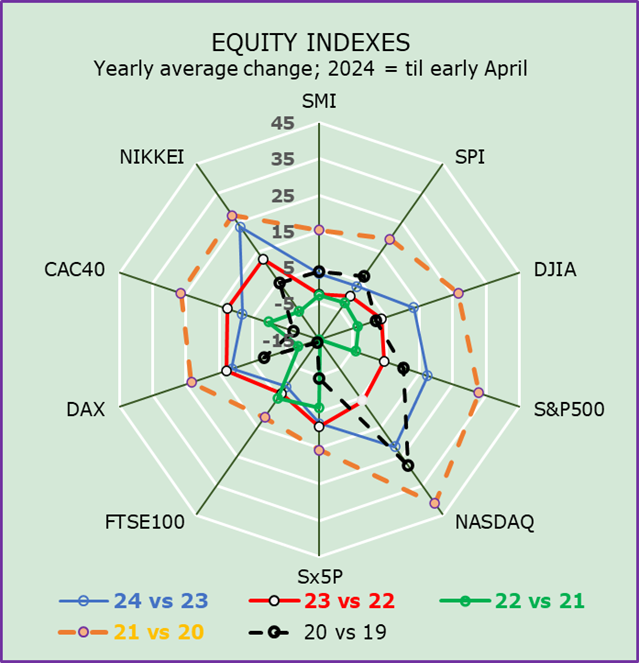

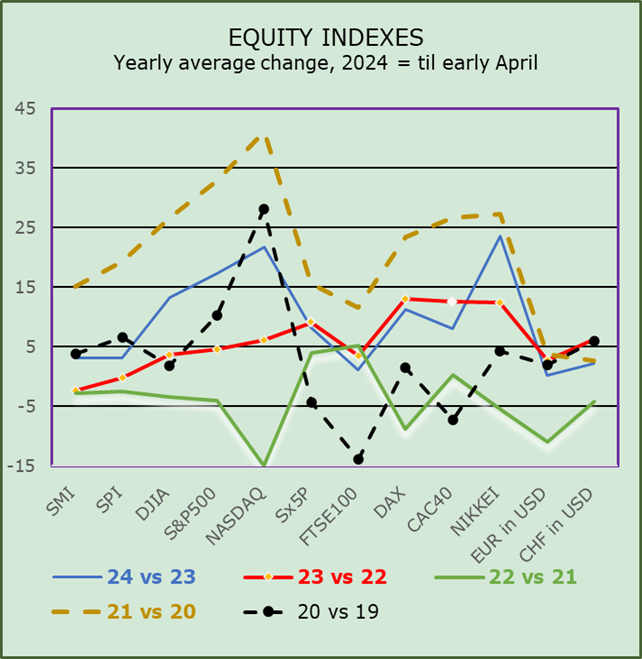

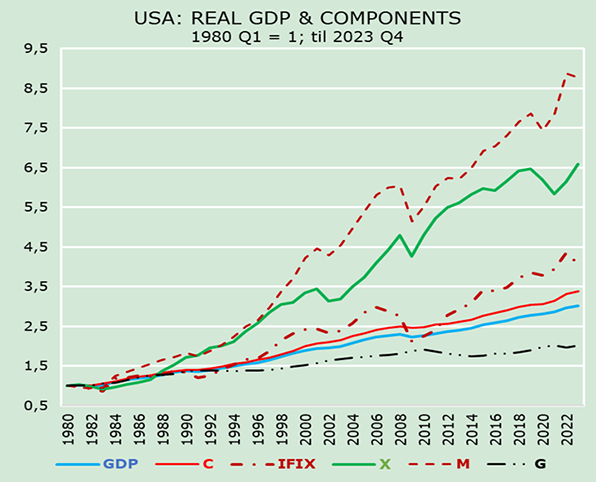

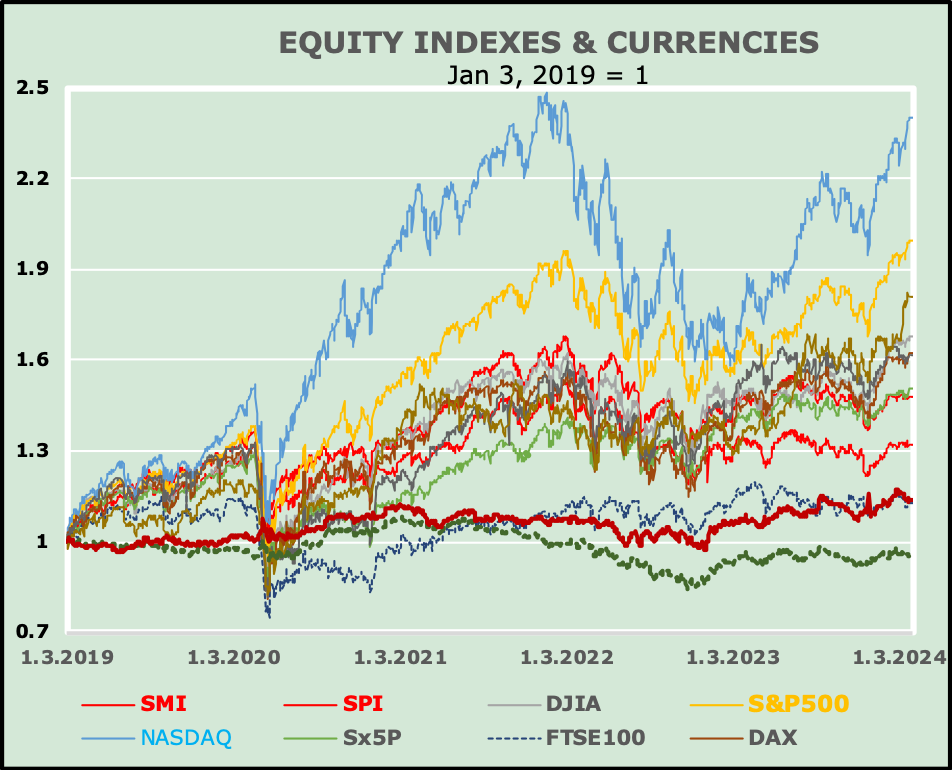

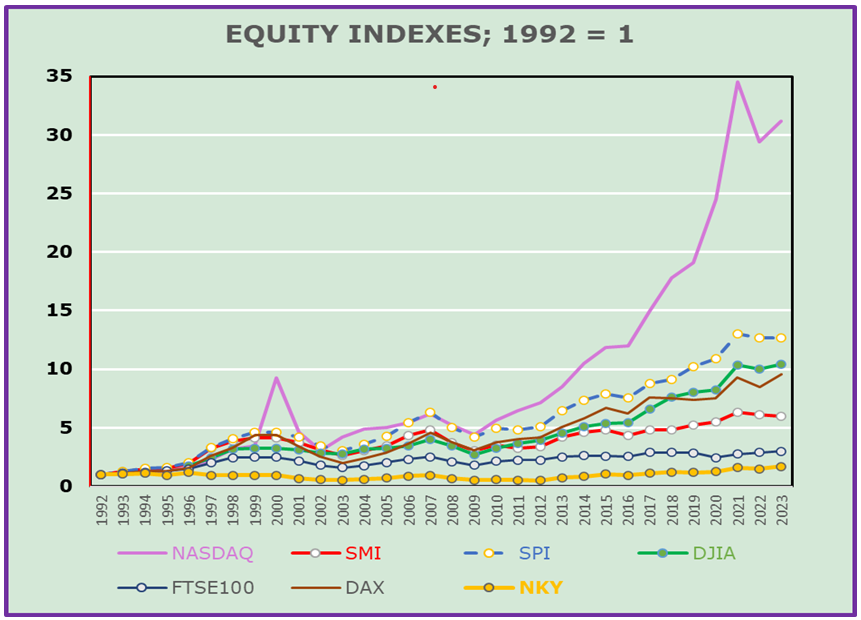

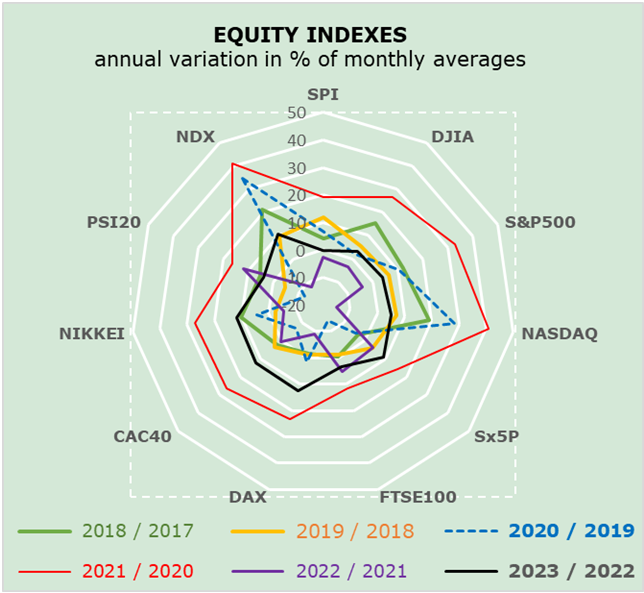

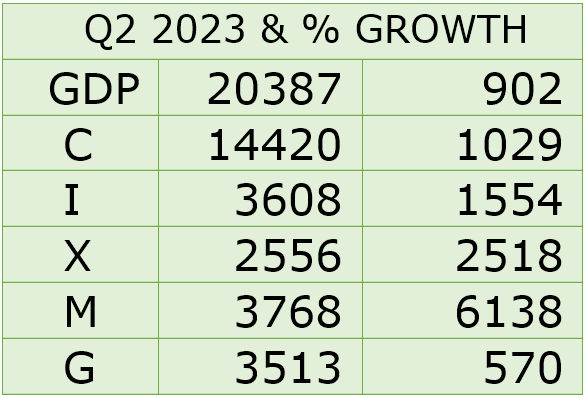

What do the developments of share indices indicate for the period since the end of 2021? The following chart points to two quite similar developments. The first refers to the period of the Covid pandemic, which peaked in late 2021 to early 2022, followed by a significant correction phase until the end of 2022. The second phase, which is similar to the first and extends from the end of 2022 to 2024, shows a fairly similar development. However, the growth rate of the equity indices, particularly the NDX, NASDAQ, NIKKEI and S&P500 compared to all other indi-ces, is revealing in the second phase. What conclusions can be drawn from these develop-ments is the real question at this point. Do you have any suggestions?

As the chart implicitly shows, it is impossible to explain why inflation can be contained pri-marily through interest rate cuts. What caused the correction in 2022 and the subsequent re-covery since the beginning of 2023 is the difficult contextual question?

Despite the rampant economic pessimism, share indices have recently reached new highs again. At this point, we would like to call the reader’s attention to a rather positive effect – the so-called “quantitative tightening” – a little-noticed approach, that is increasingly playing a decisive role on stock markets. This process is referred to as “buybacks”. Companies are increasingly buying up their own shares on the market. One might ask what effects these measures have or could have? A first answer that comes to mind, is undoubtedly the rise in share prices. Buying treasury shares on the market is reflected in higher earnings per share (EPS). These actions clearly point to high returns and prompt other market participants to take coherent action. It is indeed instructive to know how these developments play out. When the number of shares on the market is reduced, earnings per share increase, regardless of economic expectations. “Scarcer shares are the order of the day”.

As we know, there is another advantage: Buybacks are de facto an indirect form of remuner-ation for shareholders. The taxes due are delayed until the time the corresponding capital gain is realized, at a lower tax rate than dividends and at a time of the shareholder´s choos-ing.

Another important message relates to the prospect of a future, beyond the rampant negati-vism regarding inflation and lower expectations for economic activity. In this context, the question arises as to whether this attitude is not also relevant for the valuation of most major technology stocks. Let’s define this context as “corporate quantitative easing”! At this point, we wonder what the difference is between corporate quantitative easing and central bank quantitative tightening is – or ought to be. In other words, we ask ourselves which are the causes of the sharp rise in most technology stocks? Can we speak of technology-driven quan-titative easing? In the current environment, investors need to take a clear stance, because the quantitative tightening of central banks contrasts with the increase in liquidity available to shareholders in the market. In other words: Will politics prevail in the financial markets over increased liquidity? In this context, there is an interesting answer: The amounts that central banks withdraw from their own balance sheets flow into the financial markets through the windows of the buyback programs!

SHORT-TERM ASSESSMENT

As we write the July EMR, a so-called “tariff war” is imminent at a global level. When as-sessing the possible consequences of current events, we are reminded of the so-called tariff war that has raged at a global level in the past. In addition, recently, the press reports that the USA, Japan and South Korea are exerting increasing pressure on China to control exports of semiconductor technology and to co-operate in key sectors. What consequences this be-havior may have for the economy remains a difficult question.

An initial impact concerns the increase in prices for electric vehicles from China. As a result of the recently announced change, tariffs in Europe have risen by 38%, in addition to the 10% already in force. The increase in the United States is reported to be 102.5%. This politi-cal stance is currently being labelled as “economic self-destruction”. Let’s not forget that the International Monetary Fund found in 2019, based on data from 151 countries in the period from 1963 to 2014, that the introduction of measures to increase tariffs leads to negative effects on production volumes and productivity!

Given the ambivalent outlook, the conflicting expectations on the political front do not bode well. At this point, we could argue that Swiss investors could benefit from a significant home bias, mainly driven by a strong currency.

Suggestions are welcome.