EMR February 2024

Dear Reader

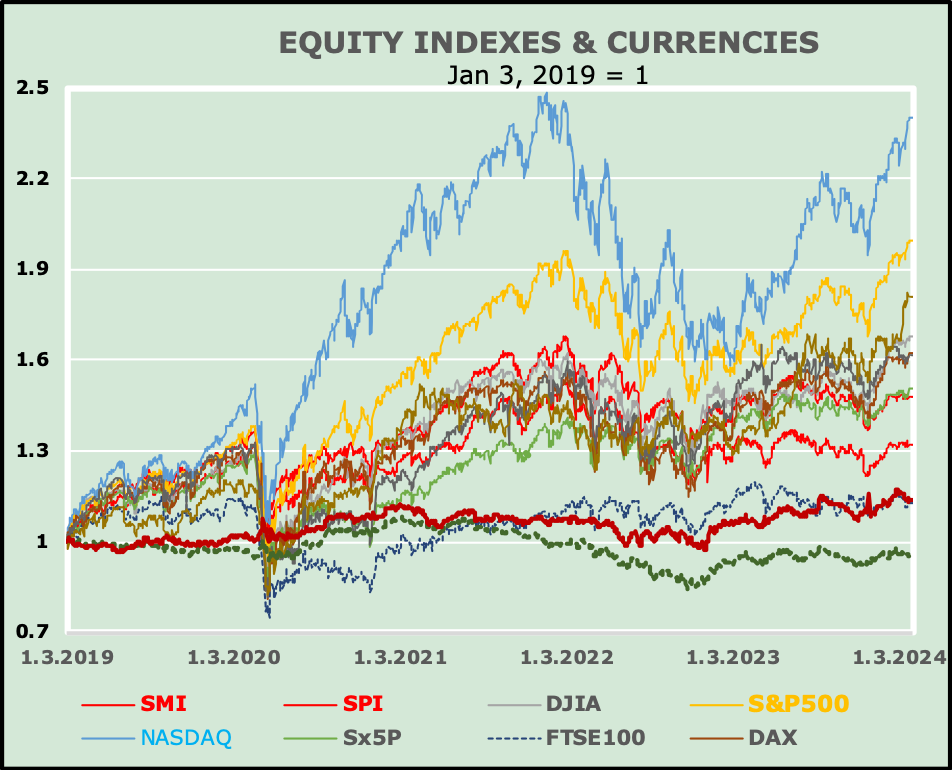

STOCK INDICES = EYE-OPENER?

Recent developments show on the financial markets that hope and fears are not and cannot be the only tools explaining their performance. Consequently, in this EMR we focus on the performance of selected equity indices. In addition, the environment continues to be characterized by absurd and unacceptable armed conflicts and other shocks that could shake the world.

The following chart raises the question: What can be deduced from the performance of the stock indices and currencies in the current uncertain and controversial environment? What follows is what we believe to know.

After increasing instability due to the COVID-19 pandemic, the markets collapse in February 2020. Overall, from January 3, 2023, the graph shows significant differences in growth, but rather congruent declines.

Significant differences in growth across countries are seen in the second period from 2021 and the interim peak on February 18, 2021 (1.58 indexed series or 16057.44 real closing prices of the Nasdaq index). It is worth recalling that 57.68% of the Nasdaq index is made up of technology and 17.59% of consumer discretionary stocks. In the S&P 500 Index, the main indicators are: 26.1% = Information Technology, 14.5% = Health Care and 12.9% = Financials. Consumer discretionary accounts for only 9.9% and industrials for 8.6%. The SX5P Index and the NIKKEI Index are the worst performers in our shortlist for the period from November 26, 2021 to early 2024.

DETERMINISTIC ASSUMPTIONS

The chart above prompts an inquiry into the primary factors influencing the fluctuations of the stock indices shown. Upon closer examination of the performance, the following observations can be made:

- Technological advancements have greatly influenced the performance of the analyzed indices. The NASDAQ and the S&P500 have particularly responded strongly to these innovations. It is important to note that the focus should not solely be on price changes, but also on the independence of the domestic economy. As mentioned in the previous EMR, these interdependencies should be taken into account. Therefore, it is crucial to provide a clear answer to the following question: Why is it that most analysts and forecasters have focused so much on inflation and not on technological innovation?

- We wonder why a large number of commentators, journalists, and economists continue to focus primarily, or even exclusively, on monetary policy as the primary influence on the markets.

- Analyzing the demand for technological inputs in economies with low-cost production presents a unique challenge. In our view, this approach is still not receiving enough attention.

- (d) When examining the long-term performance of the EUR/USD and CHF/USD exchange rates in comparison to the presented equity indices, it is apparent that their performance is relatively subdued in comparison to nearly all of the equity indices presented.

The global economy has proven to be more resilient than expected, with falling inflation and no sharp rise in unemployment. However, there is reportedly a shortage of skilled workers and experts in various sectors.

CONSIDERATIONS

Every forecast relies on assumptions, which can directly and indirectly affect the investment strategy and potential returns in the face of unforeseen events.

Since 1992 and over the past four years, the monthly performance of the stock indices is as follows:

- It is unclear why the central banks focus on fighting inflation through interest rate adjustments has such a significant impact on the performance of the DJIA (+10.4%) compared to the Nasdaq (31.2%) or NIKKEI (1.7%).

- Assuming that the planned interest rate cuts by the US, Eurozone and Swiss central banks would not have an equivalent and significant impact on private consumption and business fixed investment, what would be the impact on consumer spending and investment if there were to be a war trend, especially if this continued to hamper the development of international trade?

CONCLUSIONS

We continue to believe that war developments in Ukraine and the Middle East will remain more decisive than monetary interventions. We are concerned about the possible impact on world trade due to the uneven performance of China. Russia and other competitors in the free world.

In other words, we continue to anticipate high volatility in the first two quarters of 2024, which will have to be dealt with mainly by adjusting sector and stock selection beyond equities.

Our biggest fear is that the planned/feared interest rate adjustments by central banks in the free world will continue to be unsatisfactory due to the unbridled control of international trade by China, Russia and their respective alliances. In this context, it will be deterministic for the development of inflation over which period of time, the possible/highly feared difficulties concerning the freight transit in the Suez Canal cannot be managed via interest rate adjustments.

A specific factor that will accompany us in the course of 2024 are the Presidential Elections in the USA. We have a tremendous difficulty in assessing the possible outcome.

While the large majority of analysts set theirs focus on fighting inflation, we prefer to focus on economic growth especially international trade as the determinant of our Investment Outlook.

Suggestions welcome.