EMR July 2021

Upheavals

Not only as a result of the COVID 19 pandemic, investors and also the public at large, are experiencing a trend reversal, away from free trade via the introduction of a new global minimum tax rate of 15%, with the aim of generating even higher revenues for the government.

At stake are the benefits of free trade through the institution of politically induced changes in relative prices.

Policy interventions to correct distorted distortions

TYPES OF DISTORTIONS: In this issue all price ratios are referred as terms of trade, although with specific qualifications.

We define the rate at which goods may be exchanges domestically in production as the marginal rate of transformation in production (TTP).

The rate at which goods may be exchanged domestically in consumption is defined as the marginal rate of substitution in consumption (TTC).

The rate at which goods may be exchanged through international trade relations is referred to as the foreign terms of trade (FTT).

What says the economic theory hereabout?

The argument put forward by various political entities calls for corporations around the world to pay at least a 15% tax on their earnings. The final rate could go even higher than that, as here and there the 15% is meant as a “floor”. Such a policy e.g., in the case of the USA, is a dramatic and dangerous policy reversal as compared to the policy advanced by the previous Administration. This “political jargonizing” is meant to discourage companies from relocation domiciles to foreign countries.

This “political approach” could have far-reaching economic effects, as not all countries will participate and thus trade conditions could be distorted. In addition, we see important implications for the domestic side of the economy as well as the international side.

Let us thus return to the implications on TTP, TTC and FTT. Following Bhagwati et al.[1] in the sixties and early seventies one can summarize the dangerous distortions as into the following three categories: production, consumption and foreign trade distortions.

The current discussion has not yet focused on the real implications of this political exercise. A production distortion results when the marginal cost to a business of a specific good differs from the cost to society (domestic and international). In terms of the above quoted abbreviations the result of the proposed tax may be defined as TTP ≠ FTT = TTC. At this stage it is impossible to quantify the cost of the singly enterprise vs. those of each country. In other words which are the marginal costs for an enterprise point of view vs the marginal costs from the society`s point of view?

A further distortion can be seen in the context of the marginal rate of substitution in consumption i.e., TTC ≠ FTT = TTP. Assuming that the envisaged policy distorts consumption to the community vs. the goods that can be exchanged in the world markets, one can assume that the price ratio facing the local community would undoubtedly differ from the relative value to individuals.

Surely enough there will also be trade distortions. In the above context we portray the trade distortion as FTT ≠ TTP = TTC.

Summarizing, we ask the following question: What is the result of the proposed tax increase if either a production or consumption (or in the worst case both) distortion(s) exist? No doubt the nature of the distortion must be determined. At least over the short to medium term we thus remain confronted with sizeable market volatility. In addition, we must recon with differential repercussions in the case that a country has market power or hasn`t enough market power, because market power allows a country to render its exports of goods. The argument speaks either of technical advantage or disadvantages. A recent example is the development of electronic semiconductors.

Disturbing at this crossing is what Treasury Secretary Janet Yellen said “that the international tax architecture must be stabilized, that the global playing field must be fair, and that we must create an environment in which countries work together to maintain our tax bases and ensure the global tax system is equitable and equipped to meet the needs of for the 21st century global economy.”

Nice words, but who will and can accept simply to follow the interest of large entities like the USA, China, and the EU. Is there enough room for countries like Switzerland to follow their own needs and requirements? The news came following meetings with a steering group within the Organization for Economic Cooperation and Development that the Treasury said featured “earnest” talks of a global tax? Somehow, we doubt it.

Nature of the recent distortions

Notably the distortions are both domestic as well international. Domestically they concern consumer and production inefficiencies, while internationally we see it in the growing discrepancies between exports and imports growth putting pressure on the negative and still growing international trade imbalances. In this context we ask ourselves if the proposed tax increase of 15% is the necessary and sufficient policy to cure the distortions? We believe that the nature of the distortion lies mainly in the international trade imbalances, although their impact is concentrated mainly on production and productivity. In the context of the “low-cost producer”, China, it should be remembered that it does not have to abide by international rules and regulations. At the top of the list is a production distortion of which there is no equal history. The price of imports from low-cost countries hinders, in due turn, the production lines of the industrialized world. The result is undoubtedly a currency readjustment. In the midst of the recent developments governmental indebtedness has skyrocketed. In other words, public and entrepreneurial indebtedness cannot be solved with a unilateral 15% tax increase.

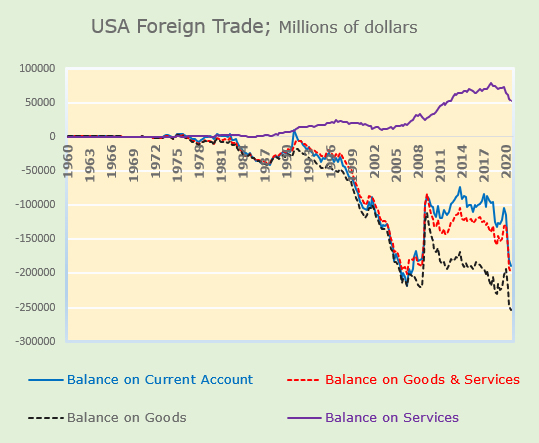

It is worth noticing that the major distortion in the US Foreign Trade data concern primarily the balance of goods. The US are undoubtedly the importer of last resort.

Conclusions for investors

Our conclusions are to be seen as a specific consequence of an extraordinary accumulation of governmental indebtedness and the “Covid-19 opening”. We are not aware of any comparable past period, thus have difficulties in being specific about future developments. Economic challenges are not easy to quantify either in the short or medium to long term. Consequently, we will focus our attention to the short-term. No doubt, the financial sector remains crucial for a smooth functioning of the world economy. Consequently, we assume – as a working hypothesis – that the measures ought to have an impact on inflation preponderantly over a longer period of time. In our investment outlook we also focus on the change in international trade flows, as we must reckon with a new fact, i.e. that the U.S. will increasingly cease to be the “buyer (i.e. the importer) of last resort”. In our scenario domestic economic growth gains in importance as an indicator for the financial markets’ whereabouts.

Consequently, we do not expect a sharp longer-term increase in inflation, as it cannot simply be passed on, neither domestically nor to foreign countries. As a working consequence we continue to see potential in the stock markets compared to fixed income and money market investments. Currency hedging will have to be considered in the international portfolio diversification approach.

Overall, we fear that the current “political induced approach” simply calls for a prolongation of the period of uncertainty and volatility. Why, you may ask? Well, the proposed policy does not address the DISTORTIONS mentioned above. The primary purpose of levying taxes is to finance government deficits without significantly improving output and productivity and/or to increase consumption and employment in a timely manner.

Any suggestion is highly welcome.

1 Jagdish Bhagwati. The Generalized Theory of Distortions and Welfare, 1969 (https://dspace.mit.edu/bitstream/handle/1721.1/63654/generalizedtheor00bhag.pdf)