EMR March 2023

Dear Reader

Industrial transformation, i.e., the change in the growth pattern of the last 20 to 30 years, is once again taking place at a rapid pace. Well, our search for evidence on the position of the global economy, and by extension the financial markets, led us to the Inflation Reduction Act of 2022 (IRA), passed by the U.S. Congress and signed into law by President Biden on August 16, 2022. Astonishingly enough, it goes almost unnoticed in the media. Now, one may ask what the scope of this act may be? Well, it is a law primarily aimed at curbing inflation by reducing the deficit and investing in domestic energy production while promoting clean energy. Among other things, the enacted legislation is expected to raise $738 billion and authorize $391 billion in energy and climate change spending and $238 billion in deficit reduction. Although the expected impact on inflation is somewhat controversial, it still indicates some economic progress. Indeed, the goal is to make substantial public investments in social, infrastructure and environmental programs throughout the country.

From this ambitious program, one can infer the implicit intention to promote domestic economic activity. In other words, this legislative text favors domestic investment, which in due course will also mean a reduction in certain imports. Certainly, it will take some time for this to become apparent in practice, but it nevertheless requires careful and continuous analysis of foreign trade.

The said act implies “regulation” with the specific aim of balancing/protecting the local competitiveness of the national market from the oligopolistic aggressiveness of mainly multinational technology corporations and especially nations like China. The “act” presupposes an initial reaction by the governments of democratic states and thus a clear response to the Russian invasion of Ukraine. At this juncture, it is worth mentioning that the EU faces similar difficulties as the US, namely rising import prices. A key difference between the U.S. and Europe, especially the EU, is the lack of “decision-making power,” which is still based on the authority of the respective national authorities. In addition, it should not be forgotten that the EU also decided to suspend state aid regulation with the Temporary State Aid Framework of March 2022. Strangely enough, the focus was mainly on Germany.

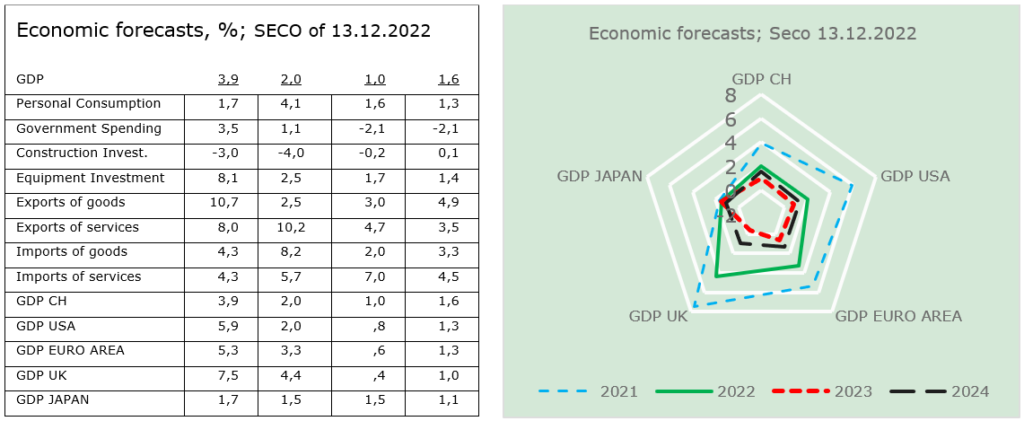

In the table and graph we show e.g., the SECO’s (State Secretariat for Economic Affairs) outlook in order to illustrate the specific interrelationships.

CONSEQUENCES

The annual data and forecasts tell us that the U.K. and U.S. real GDP growth rates were the highest in 2021 and 2022, while the other countries’ data were significantly more modest. The Brexit decision is somewhat visible in the UK GDP data. The Covid-19 years and recent actions on interest rates by central banks to reduce inflationary pressures are visible in the GDP data of the countries shown.

Recent weeks have witnessed a certain revival of optimism, albeit accompanied by understandable caution, especially in financial circles. This seems to be supported by an increasing number of macroeconomic signals, as evidenced by the recent “modest” increase in the benchmark interest rate by just 0.25 percent, which is a clear sign of the approaching end of the rate hike cycle.

The risk of recession is slightly decreasing, mainly due to the explicit willingness to give extensive support to fixed investment by local enterprises. In the context, there is talk of “repatriation” of production of technological goods, to reduce dependence on imports, from the Far East. The Seco data are really telling. We are often told that the rise in the consumer price index must be controlled by raising interest rates. The U.S. Federal Reserve took the lead and raised interest rates significantly. Other industrialized countries have followed suit. At this point, we would like to point out the potential impact of rising prices on asset allocation.

Nominal interest rate increases—such as those recently induced by central bank measures—argue in favor of exposure to fixed-income securities. This, due to the fact that increases in interest rates usually open up opportunities to earning money on fixed-income securities. However, there is also the risk of loss in times of rising inflation. It is necessary to check whether future real interest income is higher than the cost of inflation. If this is not the case, the risk of loss would have to be assessed. At this stage, we continue to favor investing in equities. Particular attention needs to be paid to various sectors such as technology and chemicals, with volatility to be closely monitored.

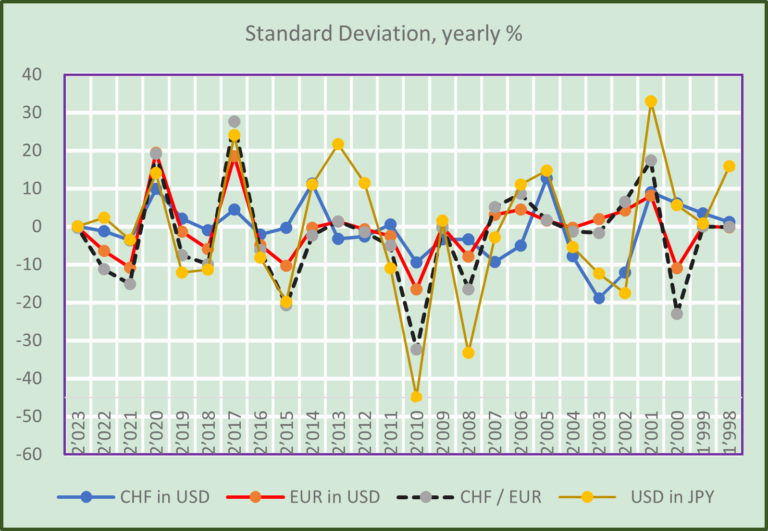

The fact is that the financial markets play an important role in the fluctuations of business cycles. Given that the current tightening policy could continue for some time, we think it is quite difficult to predict exactly which sector of the economy should be overexposed or underexposed and in which time frame. However, we consider the Russian invasion and war on Ukraine to be the most specific determinant of a worthwhile asset allocation. Geopolitical tensions aside, the impact on international trade and thus consumption and investment will need to be carefully monitored. In terms of international diversification, one should seriously consider the possible divergencies (STDEV) of the leading currencies in the following chart.

FOCUS ON SWITZERLAND

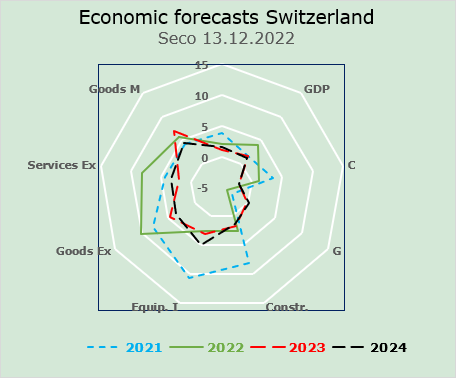

The Seco data on the primary sectors of the Swiss economy—see following chart—are telling indeed. Often, we are told, that the increase in the Consumer Price Index must be controlled via higher interest rates. The Federal Reserve Board has taken the lead in strongly pushing interest rates up. Other industrialized countries followed in a similar manner. Here, we would like to point to some other factors responsible for the increases in prices.

CONSEQUENCES

Undoubtedly, the Russian invasion of Ukraine will force the economies of the free world to reduce their dependence on autocratic, pro-communist countries as quickly as possible. This is bound to entail a return to local production of many goods and services and an orientation toward other producers of oil, gas, etc. First signs of this change are visible in the U.S. technology industry. See: Chips Act , in which special attention is given to short-term inflationary pressures and thus to the specific responses of central banks.

In Europe, too, there are proposals that go in the same direction, although there are still differences from country to country. There is no doubt that the invasion of Ukraine is a sign of an increasingly inevitable “de-globalization.”

Geopolitical tensions aside, the impact on international trade, and thus on consumption and investment, needs to be carefully monitored. The dreaded volatility of energy and gas prices will remain a source of confusion, both in terms of economic growth as a function of inflation, and in terms of the ups and downs of international trade, which currently speaks of continued volatility, and not just in the financial markets.

There is a further serious difficulty: the increasing and high indebtedness of countries, companies and the general public. Fortunately, the current situation does not resemble that of the late 1970s, when Paul Volcker, chairman of the FED, was forced to intervene aggressively to fight inflation.

In terms of international diversification, one should seriously consider the possible developments of the leading currencies.

OUTLOOK 2023

The above-outlined environment clearly indicates a dramatic change in the environment. Until recently, the focus was on fighting inflation; now the focus is much more on “repatriating” production. This is evident, for example, in the stimulus proposals [Inflation reduction ACT (IRA), Chips and Science Act, and Bipartisan Infrastructure Law]. Thus, the focus is clearly on renewable energy, semiconductors, and infrastructure, i.e., promoting local economic growth while reducing dependence on foreign manufacturers.

In both the United States and Europe, economic policy is no longer primarily focused on fighting inflation, but rather on rapidly renewing the domestic manufacturing sector to reduce dependence on imports from foreign manufacturers. This, if implemented coherently, would lead to a significant increase in local employment and economic activity. The specific objective is, among other things, to reduce dependence on China.

At this stage, our forecasts can be considered somewhat more optimistic than those currently circulating in the press. To some extent, our assessment is confirmed by a contradictory political attitude that is no longer so much determined by “cheaper producers” as much as by the “free market” or, at best, by an egalitarian mixture of both approaches.

FINDINGS FOR INVESTORS

Assuming that investment growth will replace government spending as the main determinant of future economic activity, one needs to look beyond infla-tion expectations and trends to define a successful investment approach. Therefore, we argue as follows:

- The era of runaway inflation is almost over; more attention needs to be paid to price stability.

- If the assumption is correct that inflation will not rise as strongly as it has recently, fixed-income investments should become somewhat more attrac-tive, at least in the short to medium term.

- A reduction in dependence on autocratic countries, combined with a not in-significant increase in domestic production, would stimulate optimism in fi-nancial markets.

- We continue to believe that the CHF remains promising, as does the USD.

Comments are welcome.