EMR December 2023

Dear Reader

REVIEW 2023

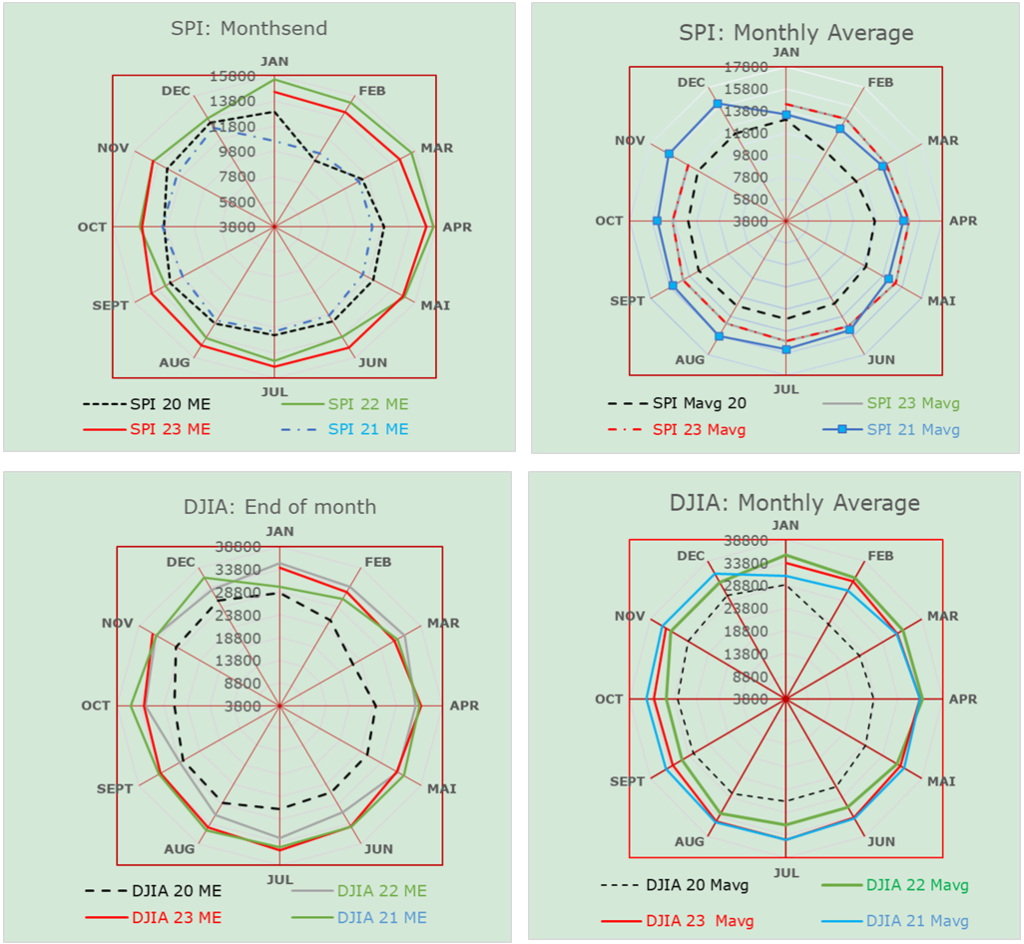

Examining the developments of the SPI (Swiss Performance Index) and the DJIA Index e.g., for the last four years, both on the end of month and on a monthly average basis, as implicitly shown in the following charts, is indeed highly revealing. What can be deduced from the following charts is here the following:

Although the graphs of the SPI and DJIA stock indexes do not show striking differences, indicating a rather stable environment, with the exception of the period between January and February 2020 and 2021, it should not be forgotten that in the years under review there have been divergences in their respective daily performances, although they have not been as significant as might be inferred from repeated comments by various experts. However, it should be noted that the differences in the monthly averages are rather small compared to the month-end averages.

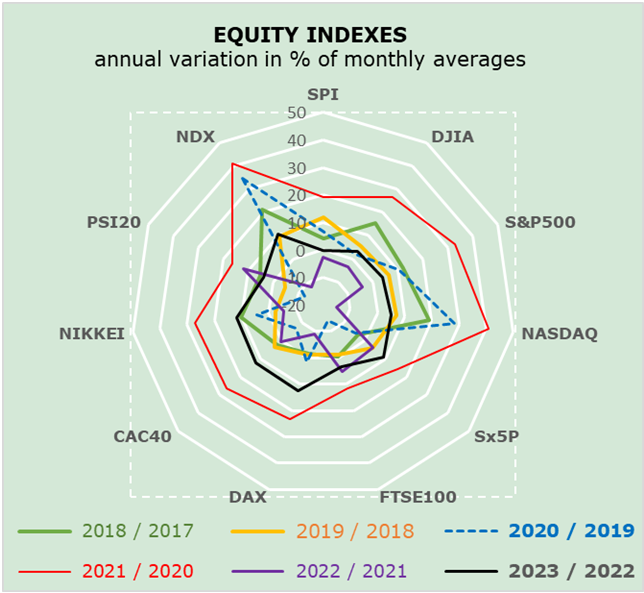

Readers might object that an analysis based on only two stock indexes is insufficient. For this very reason, we report the annual % change in the respective monthly averages for a number of stock indices, as shown in the following graph, which shows drastic differences, does it not?

The annual variations, as shown in the graph above, are indeed remarkable, both in terms of size and from index to index. A first specific argument, inherently contained but not deducible from the graph, concerns the fluctuations in the respective currencies (not shown in the graph). A further argument concerns the “technology” content of each index. Recall that during the period analyzed, technology has played – and will continue to play – a decisive role, not only for stock markets, but especially by virtue of the differential in economic activity between countries. At this point it is worthwhile, at least as a mere example, to compare the fluctuations of the DJIA with those of the S&P500 and/or the Nasdaq.

CURRENT ENVIRONMENT

Contextual analysis reveals to us that there are no “additional and decisive factors” to take into account. The Russian war against Ukraine and the war in Gaza continue to remain deterministic. The expectations remain conditioned by geopolitical instability, while technological innovation and central bank measures aim to fuel certainty. As a consequence, we find the economic outlook to be far from rosy. Crude oil producers continue to play a rather dangerous role. Their goal is to keep energy prices as high and as long as possible, essentially to be able to finance absurd and devastating wars.

In addition to the fact that consumption is the engine of economic activity and thus has been and continues to be the promoter of prosperity, we also expect several stimuli from international trade in essential goods and services. It will be difficult to contain price increases. Consequently, the actions and responses of monetary authorities should not focus excessively on fighting inflation, but rather on stimulating domestic economic activity, which requires a shift from foreign investment to domestic renewal. It should be noted that the other components of GDP have apparently not contributed as significantly to economic activity, which is a surprising sign.

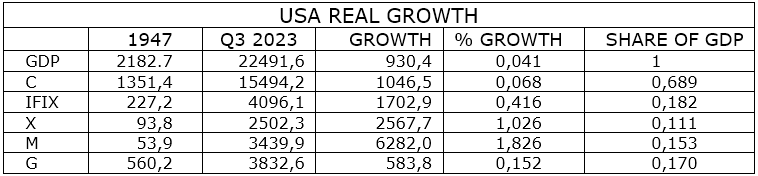

To explain what we mean, and for simplicity’s sake, we limit our analysis to the developments in the United States, assuming that the impact may be somewhat similar in other industrial countries. U.S. data since 1947 show that consumer spending remains the largest contributor to GDP. Nevertheless, the following table of U.S. GDP and its major components reveals rather surprising results. Over time, consumer spending has tended to be less pronounced, that is, less driving. The spread has widened over time. The growth differential is clearly visible in the data (see table), while all other GDP components seem to make only a marginal contribution. Whether this assessment is “right” or “wrong” as a measure of the respective levels, is the appropriate question at this stage. is it not?

In order to analyze the U.S. economic activity data shown in the following table, let us first define the headings: GDP = Gross Domestic Product; C = Consumption Expenditure; IFIX = Investment Expenditure; X = Exports; M = Imports; and G = Government Expenditure. The overall rates are summarized in the following table:

A close examination of the data in the table above speaks volumes. Although the data point to consumption spending as the driver, the growth rates of the other components of GDP suggest to us that imports are the key determinant of GDP growth, followed by exports and investment. Consumption spending ranks only fourth, while government spending precedes all other major GDP components. The table confirms our conclusion that the causes of the current disorder lie not so much in interest rate trends as in international social and moral disorder (Russia’s war in Ukraine)!

OUR EXPECTATIONS

The interpretation remains controversial and it is difficult to define a plausible and credible scenario. Volatility affects both the short and medium term. The monetary authorities and most forecasters are primarily concerned with restoring price stability, e.g., through higher interest rates. Against this backdrop, we continue to favor quality stocks, especially in the technology sector. The level of long-term interest rates is favorable for quality bonds, at least in the medium term, which promise attractive yields and opportunities for capital appreciation for the first time in a long time. Overall, we remain strongly focused on the domestic market for both equities and currencies. Never before in human history has a pandemic caused governments around the world to shut down their economies so abruptly and almost simultaneously, only to revive them with massive stimulus. The result remains uncertain, somehow pointing to the return of inflation, contraction in the labor market, rising bond yields expectations, and persisting high government indebtedness, continuing to nourish volatility.

MERRY CHRISTMAS & A HAPPY NEW YEAR

Comments are welcome.