EMR November 2023

Dear Reader

TOUGH OUTLOOK

It is well known that the IMF has issued a specific warning, namely that “financing the fight against climate change, only by means of incentives, seriously risks putting states” budgets in crisis. The IMF warning makes explicit reference to competition in the context of the energy transition campaign, and in particular to the U.S. Inflation Reduction Act (IRA), of August 16, 2022, which in hindsight has much more to do with fighting against inflation than with climate change.

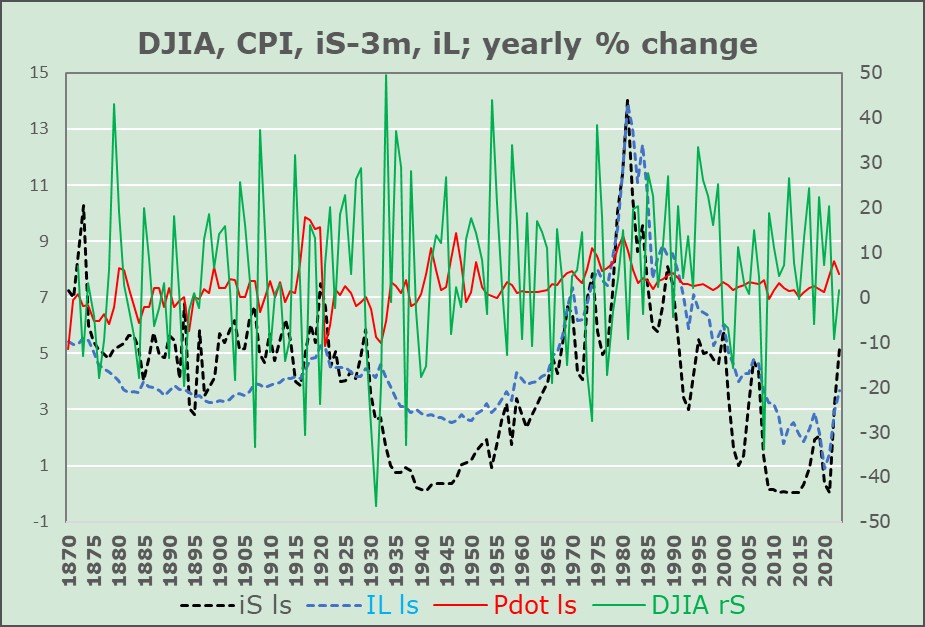

This very important caveat leads us to examine the relationships between inflation, interest rates, and stock indices to be able to present a likely or possible outcome in terms of investment diversification. The following chart indicates significant differences.

Labeling: DJIA = Dow Jones Index; iS = 3 months interest rates; iL= 10y Govt Bond yields; Pdot = Consumer Prices; ls = left scale, rs = right scale.

OUR ASSESSMENT

The graph based on long-term series indicates a complicated period. We would like to highlight that the outlook continues to be driven by a high degree of uncertainty and therefore it is very complex and difficult to define precisely, especially in the short to medium term. Monetary authorities remain primarily concerned with restoring price stability, while in our view there should be a much greater focus on international trade and the corresponding impact on consumption and investment spending (private and public). Recent actions and reactions by governments do not seem to have been very appropriate, do they? Against the background of the change in sourcing of electronic products (chips and their manufacturing content), we are called upon to carefully analyze the “cost-benefit” ratio of the threat of protectionism, especially also because of Russian aggression in Ukraine and fratricidal wars in the Middle East and elsewhere. Moreover, we should evaluate this complicated scenario not only against the backdrop of China’s loss of productive power, but also against the backdrop of the expected and much-needed turn in favor of free market economies. Recent real GDP data in the U.S. (Q3 2023) clearly point in this direction. Important issues in this context are undoubtedly the “subsidy war” related to the Inflation Reduction Act (IRA) and the rather worrying rise of government debt to unsustainable levels, with perhaps one particular exception, that of Switzerland. Compared to the EU countries and the United States, the relationship in Switzerland is rather limited.

In this context, we ask ourselves what this reversal towards “domestic production” might imly for international investment diversification. Any suggestions?

Dramatic changes in the production process are in the air. We expect an increasing focus on domestic content, especially in the technological environment. However, this trend-reversal is not expected to evolve at high speed. This will be a determining factor in the long run. A second aspect we see will be the found in the evolution of labor markets, a change in trend from production offshoring to relocation to the local markets. Although this change may not be felt in the short term, it will have an impact on employment, especially in the field of technology. There is no doubt in our mind that international trade can modify the expectations of economic growth of those countries that are willing and able to finance new investment factories. Moreover, free trade will have to, increasingly, take into account the fact that it will move from being a promoter of the economy into second position, after local production. The well-known and much-vaunted virtues of global free trade in capital and goods as engines of economic growth will have to be consistently changed and adapted.

DETERMINISTIC RELOCATION

In the context of the expected shift in production, we focus on the following three factors, which we consider to be highly deterministic means of profitable investment allocation:

1. The relocation of production from abroad to the home markets or shores.

2. The deterministic importance of the availability of domestic inputs relative to imported inputs; and

3. The availability of domestic developped and produced technologies.

Recently, we have witnessed a deterministic revision of the importance of domestic versus imported production. Costs and benefits are more and more evaluated from the perspective of increasing protectionist interventions. In the international competition of free markets, the advantages and disadvantages are increasingly evaluated dynamically rather than predominantly statically. These shifts are increasingly seen as a reassessment of the concept “cheap” is no longer as deterministic as “on-time availability.”

A second aspect relates to the “content” of the means of production. The “low-cost production countries” began to raise prices and/or introduce specific costs. Production in China was defined as profitable compared to local production. In the context of the IRA mentioned above, the U.S. determined that production quotas were essential because computers could not function as expected without certain components that were only available in the U.S. The IRA was a major step in this direction.

The third aspect, which may be the most determinative, relates to the availability of domestically developed and produced technologies, i.e. an increased focus on domestic production. In terms of economic activity, we expect a significant impact on consumption and investment spending as we face, in a sense, a resurgence of protectionism. This trend is clearly visible with regard to the production of electric vehicles, but not exclusively so.

IMPACTS ON INVESTMENT POLICY

Currently, investors expect further, moderate, interest rate hikes as well as further exchange rate adjustments. As Swiss investors with a relatively high home bias, we continue to expect the CHF to outperform the EUR, USD and GBP as well as the YEN.

Economic activity is likely to remain subdued despite recent interest rate hikes, mainly driven by consumer spending. In addition, we are concerned about the weakness of the European economy, mainly due to German weakness, and the ongoing difficulties in China.

Nevertheless, stagflation is currently assumed. The global economy is suffering from a weak economic outlook and inflation that is difficult to control, especially through further interest rate hikes. Moreover, a growing number of analysts are asking: How can inflation be reduced, primarily by further interest rate hikes? Our answer, as expressed in previous EMRs, requires a rapid reduction in certain imports – especially crude oil and gas and an increase in domestic production of essential goods. The arguments outlined are our main reasons for focusing on investments in our local market, especially into account the expected and feared currency changes and also the technological developments triggered by an increasing focus on domestic activities.

Although the impact of political changes should mainly affect the medium to long-term outlook, we believe it will be imperative to closely monitor any feared economic recession. At this point in time, our outlook is also determined by the outcome of the war between Russia and Ukraine.

Behind the recent political, economic and social developments, which speak of a destructive competition, there seems to be an increasingly negative future, the so-called “chip war” (between the United States, China (including Taiwan and other manufacturers not only from Asia, but also from Europe). A further example is the electric car market. The graph on interest rate differentials points to an imminent reversal, doesn’t it?

Comments are welcome.