EMR November 2022

Dear Reader

ENVIRONMENT

Both the Covid-19 pandemic and Putin’s war against Ukraine are increasingly determining economic analysis, both in the short and long term. Also going almost unnoticed by the public debate are the consequences of “digital nomadism” and, in particular, the tax consequences of the migration of highly qualified professionals who take advantage of the opportunity to work at a computer in places where taxes are low.

DEMAND VS. SUPPLY ANALYSIS

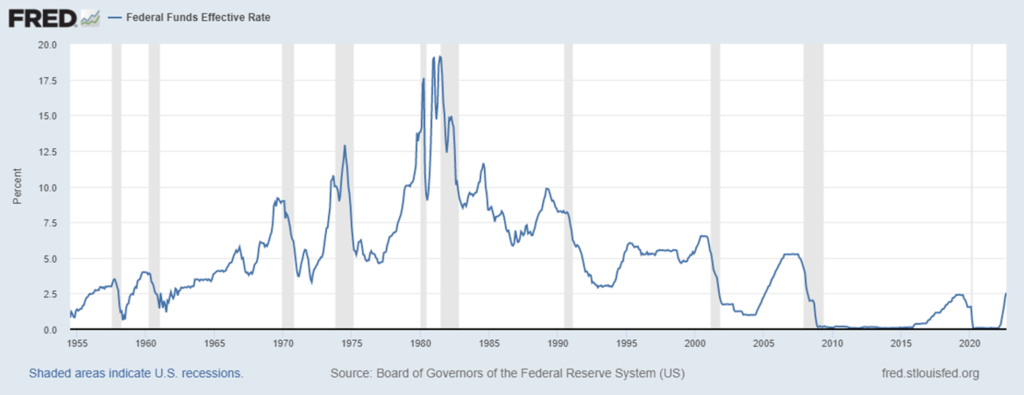

As a result of both the Covid 19 pandemic and the war against Ukraine, two specific and deterministic aspects can be found regarding the short- to medium-term economic outlook. Monetary authorities have emphasized a policy of “extraordinary” monetary tightening to combat inflation, i.e., unprecedented increases in interest rates, as evidenced by the recent trend in the federal funds rate relative to developments since 1955. See table and chart.

| FOMC Meeting Date | Rate of Change (bps) | Federal Funds Rate |

| Sept 21, 2022 | + 75 | 3.00% – 3.25% |

| July 27, 2022 | + 75 | 2.25% – 2.50% |

| June 16, 2022 | + 75 | 1.50% – 1.75% |

| May 5, 2022 | + 50 | 0.75% – 1.00% |

| March 17, 2022 | + 25 | 0.25% – 0.50% |

Indeed, it is instructive to elicit the logic behind policy responses. As far as policy adjustments are concerned, we face a real dilemma. Are the actions and reactions in curbing inflationary conditions more supply or more demand-driven?

By even superficially reading newspapers, listening to the radio or watching television, we find that the focus is on “demand.” Why is that? Well, Central banks are pushing interest rates sharply up to contain rising inflation. Thus, when interest rates are raised quickly and sharply, one must assume that the goal of containing rising inflation is to reduce demand, especially of business investment (i.e., fixed investment, construction activity, and net exports). At this point, it is worth recalling that the recent rise in prices in all major economies is not primarily due to an increase in demand, but to a sharp reduction in the supply of essential economic goods. More specifically, prices are being driven up by “policy-induced” cuts in crude oil and gas exports, primarily by Russia. Recently, there has also been a significant decline in imports of engineering components from China. It is a fact that the countermeasures taken by the EU and the U.S. should also be taken seriously.

We are currently facing a new phase in the economic cycle. The positive trends of the period prior to the advent of the Covid-19 pandemic and the invasion of Ukraine have turned into a restrictive phase, particularly in the area of procurement of vital goods and production components. In our view, this emerging change requires a radical rethinking of the economic behavior. This should entail a rethinking of the interdependencies between the economy, finance and monetary policy. In other words, it is not about inflation per se, as much as on rapidly improving the supply of key intermediate goods and products.

However, if we assume that policy should focus on supply-side rather than demand-side constraints, as has been the case recently, then we can assume a dramatic policy-driven shift away from rising interest rates toward improving domestic supply, with more emphasis on the local investment sector. What we can envision is a shift back in the production of intermediate goods and change in energy supply. This readaptation would require a shift away from “cheaper” imports to increasing domestic production. The focus should (and will) be on improvements for the local investment sector to the detriment of imports.

FINDINGS FOR INVESTORS

A closer look at the current environment shows that the focus is on raising interest rates to coun-ter inflationary pressures. The actual determinants of current inflation are almost ignored. As-suming that the rise in inflation is mainly due to factors (such as Covid-19 and especially the in-vasion of Ukraine and China’s threat to invade Taiwan), the rise in crude oil, gas and food prices would increase dramatically beyond the normal supply and demand trends. Therefore, the focus should rather be on how to solve the bottlenecks in the supply.

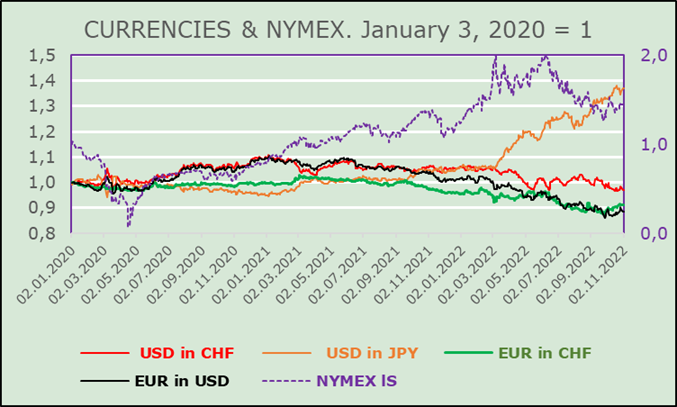

In October 2022, there were increasing calls from international institutions to slow the pace of monetary tightening because of the unexpected impact on exchange rates, as shown in the charts on currency and NYMEX.

It should be considered that the U.S. dollar increasingly tends to mimic crude oil and gas price trends. These similarities portend an imminent reversal in the fight against inflation. Thus, one may wonder whether the phase of interest rate hikes by central banks is coming to an end. Re-markably, so far, calls for moderation of the pace of monetary policy have not increased. An im-portant reason for a probable reversal of interest rates is given by the voices of international in-stitutions, speaking of an impending recessionary phase.

In the current economic policy environment, it is tricky to draw conclusions about a promising asset allocation. We believe that the Swiss investor should continue to focus primarily on the do-mestic currency market (and also the US dollar), as a positive development can be expected here. Secondly, we believe that it is premature to invest in money markets and/or fixed income instruments, at least as long as the high interest rate phase persists. Thirdly, it is necessary to quantify, as precisely as possible, the depth and duration of the much-touted recessionary phase. For our clients in particular, it seems advisable and necessary to assess the impact on the real estate market. An undoubtedly arduous task not only for the experts at Swisschange.

Comments are welcome.