EMR September 2021

Causes, Effects and History

A look at the following chart of the Dow Jones Industrial Average (DJIA) and the Consumer Price Index (CPI, referred to here as Pdot) raises some questions, doesn’t it?

Why the focus on inflation?

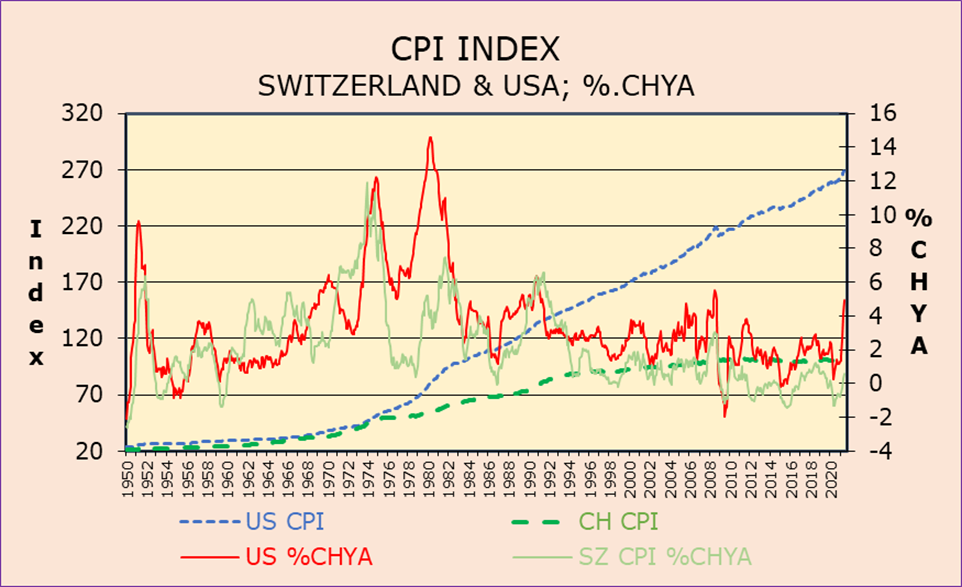

The latest data point to a pickup in inflation. For example, inflation as measured by the Swiss national consumer price index stood at 0.7% in July 2021, while it rose by an average of 2% in the Euro Area and by 5.4% in the U.S.A., representing at this time the highest level in 13 years. In this EMR issue, we are interested in the causes of the feared/expected rise in the inflation rate. In the past, developments comparable to those of the current economic policy developments were known as “the power to tax is the power to destroy.” Surely, a valid reason to inquire into the whereabouts of inflation.

Known causes of inflation

History tells us that there are several reasons why prices rise and fall, thus implying that there are many causes of inflation. At present ii is widely assumed that prices are rising as a result of a strongly expanding money supply. In other words, it is stated that there is too much money chasing too few goods and services. In the economic literature, this approach is referred to as “Demand pull inflation”.

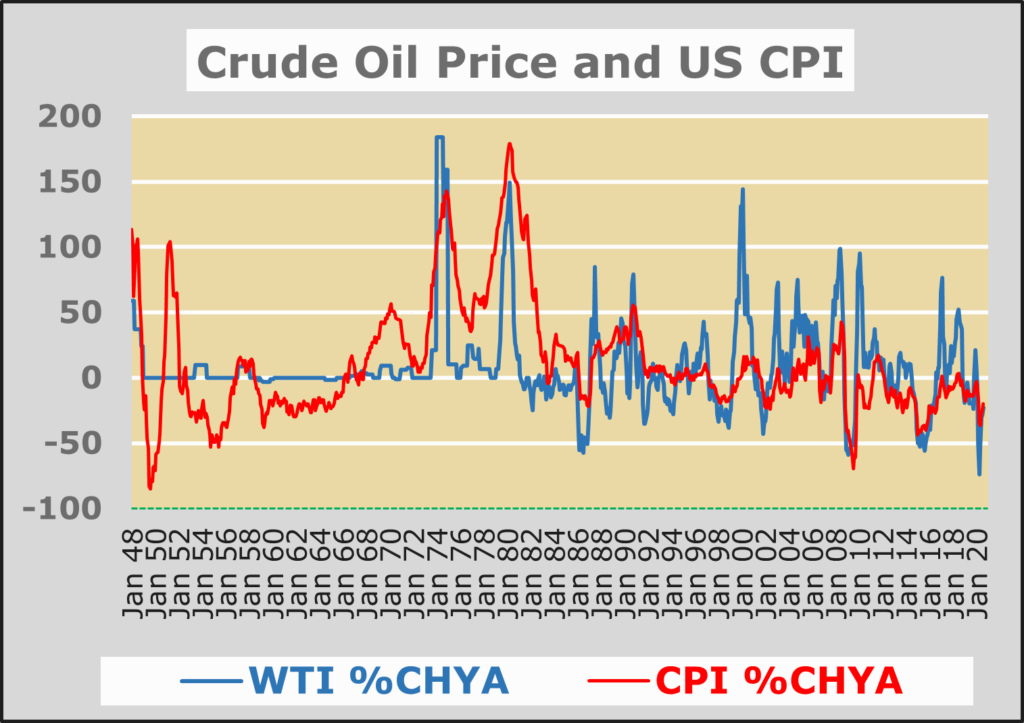

Demand pull inflation occurs also when supply falls while demand remains constant. A well-known example is the rise in OPEC prices in the late 1960s, early 1970s. The historic development on Crude oil price and CPI inflation are portrayed in the following chart.

If labor costs are arbitrarily increased, the affected producer will have to pay the price and/or suffer profit losses or even go out of business. This is certainly the case if the entrepreneur cannot improve productivity or reduce other costs. These are developments known as “Cost push inflation”.

When the government of a country – which issues its own currency – spends more than it takes in, prices will tend to rise. This approach is known as monetary debasement, which most governments have resorted to as a result of the Covid 19 pandemic. In earlier times this political refuge was also known as printing press inflation.

In recent weeks, governments have begun to focus on avoiding tax increases by taxing certain companies (see: Global minimum tax deal in our August 2021 EMR) and telling the public that their government will not raise taxes because they argue that certain companies will bear the cost. Not only economists, but also more and more people know that companies will treat taxes like other costs. If the costs cannot be passed on to consumers or other businesses, corporate profits and thus overall productivity will fall and/or there will even be wage cuts or even job losses. There is also a risk that certain companies will give up because they have difficulty raising capital. This means nothing else than Taxation decreases disposable income.

The chart of the US long-term inflation trends is telling indeed. Volatility has been highest from 1913 to the early 1950’s. The index rose dramatically, without great corrections since end 1960’s. Contextually, the question to be answered is: why the differences? Any suggestion concerning the near future? Does the chart say something about productivity?

Before assessing the current situation let us examine the developments of interest rates. In the following chart we find a significant correlation between the 3-months rate and the 10-year bond yields.

“Assessment through the looking glass”

Although the focus in this EMR is on inflation, we would argue that the outlook for productivity is the most crucial determinant for overall economic activity, interest rates, inflation and foreign trade. We argue that expanding and contracting credit demand has a much larger impact on short- and long-term interest rates than anything else.

We will therefore try to present a possible outcome in order to be able to define a promising investment strategy. The focus of our consideration is on the “power to tax”, which could end up as the “power to destroy”. In a capitalist environment, companies should not be excessively taxed to discourage the employment level of highly productive units that end up paying the price for policy missteps.

Pervasive socio-economic change

There is no doubt that we are faced with a new set of arguments primarily due to pervasive socio-economic change, a tendency to socialism and the implications of Covid-19. Economies in the developed world are driven in the short term by the multiple responses to the Covid-19 pandemic, while in the medium-to-long term they remain a function of technological advantage. It must be reckoned that the commonly used definition of productivity is output per man hour. Currently it is progressively determined by energy productivity and even more so by capital productivity.

The widespread, politically motivated assumption is that certain business owners should absorb these higher labor costs by cutting profits. However, since management and investors are usually not enthusiastic about this alternative, they will either try to raise prices to compensate for the increased costs or reduce employment, which will contribute to lower income growth. Neither option seems to make much sense at a time of “competitive disruption”, i.e. declining imports from low-wage countries. Nor does switching to cheaper substitutes seem to be a viable alternative. This seems to indicate that the fear of cost-driving inflation exists but is not as sustainable as generally expected. The switch to cheaper substitutes does not seem a feasible alternative either. What this seems to suggest is that fears of cost-push inflation exists but somehow not as sustained as widely feared or even expected.

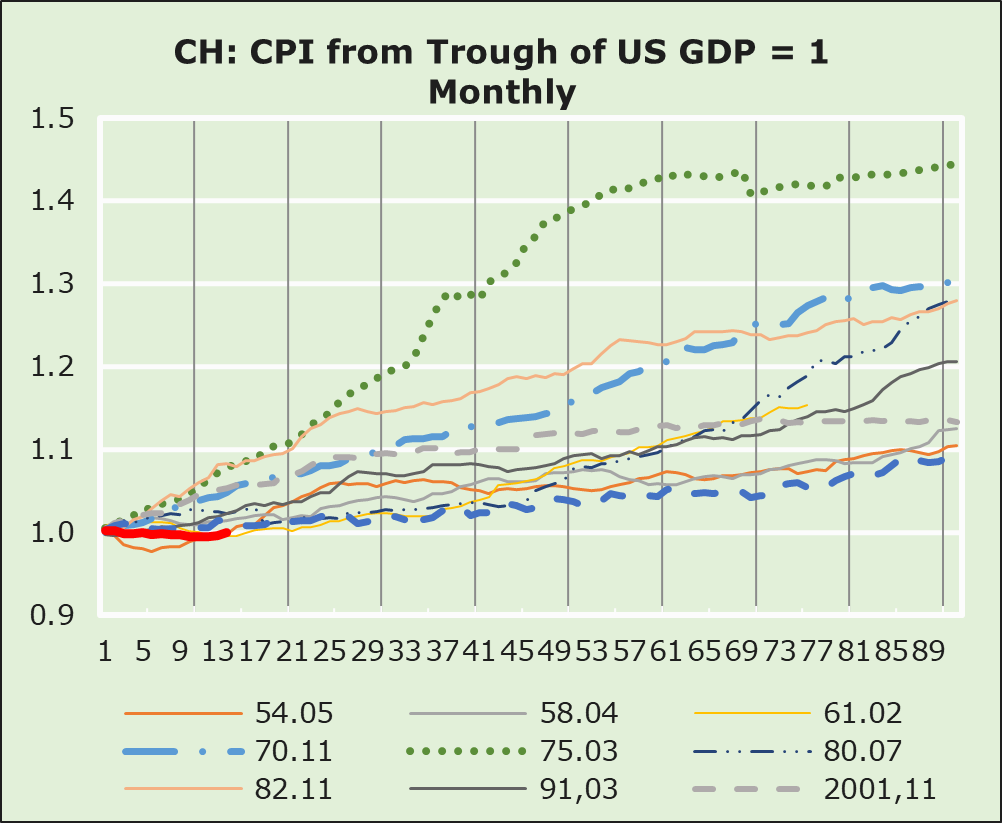

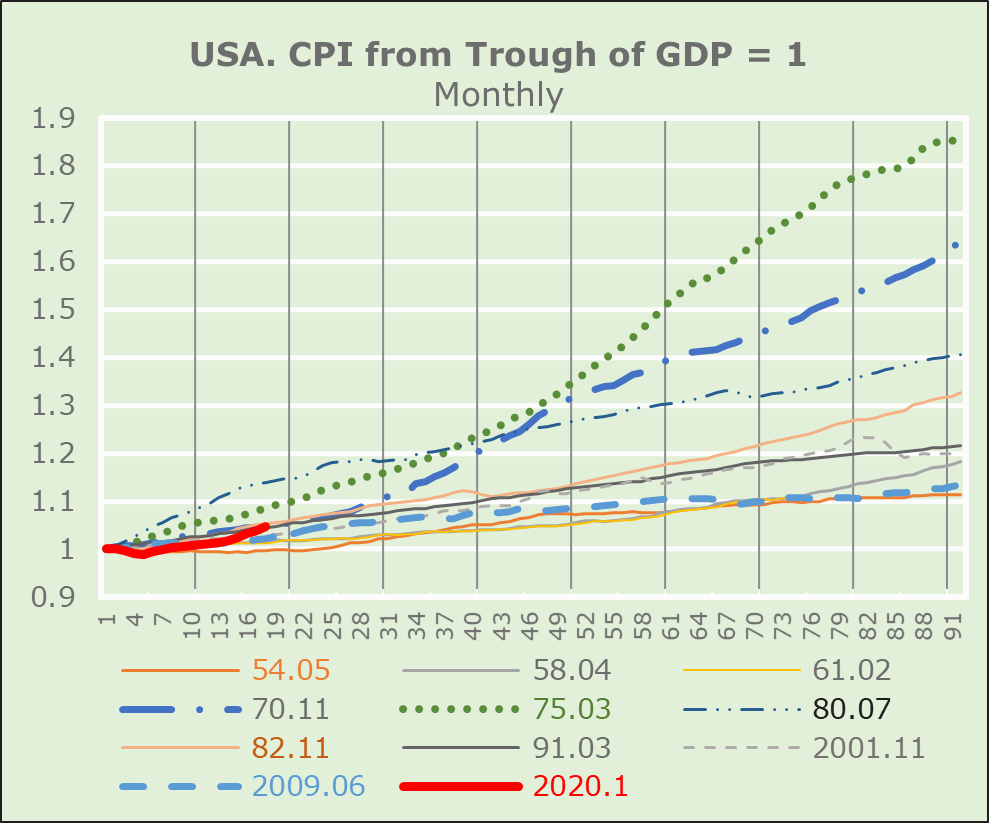

In addition, based on the considerations outlined above, we believe that the decisive factor is and will remain the return to local production relationships! The struggle between the USA, Europe and China is obvious. Dependence on a producer with a ‘slightly’ different attitude than we are used to do business can no longer be accepted. Currently the outlook is also driven by the impact of Covid-19. It is a fact that labor productivity in the USA increased rapidly during the pandemic compared with the previous decade. However, it is unlikely that this rapid pace will continue. Similar to the Great Recession, the main reasons for the strong productivity growth now are cyclical effects that are likely to dissipate as the economy continues to recover. For example, as the number of workers has fallen, capital per worker has increased, raising “labor productivity” , i.e. including energy productivity and capital productivity. How the pandemic itself will impact productivity remains to be seen.

Our approach to economic growth makes it clear that the extraordinary recent rise in productivity is primarily due to cyclical effects that are unlikely to last and could even reverse. While there is much speculation about how the pandemic itself will affect productivity, it is too early to reliably assess how strong these effects will be in the long run.

The growth accounting shows that the main causes of the recent increase in productivity are cyclical and unlikely to last. In particular, the decline in employment has boosted capital deepening; the post-Great Recession experience suggests that this temporary boost is likely to reverse. Moreover, because the employment decline was more pronounced among workers with less education and experience, the average job quality of those who kept their jobs rose. This effect has already begun to reverse and may reverse further as less skilled workers return to work.

Conclusions for investors

Our conclusions, are to be seen as a specific consequence of an extraordinary shift towards technological innovation away from traditional “output per man-hour”.

It also implies that even if inflation would narrowly fluctuate around 2%, historically seen, equities would continue to outperform fixed income securities and money market instruments.

Consequently, the USD is expected to rise vs. EUR, YEN, and GBP.

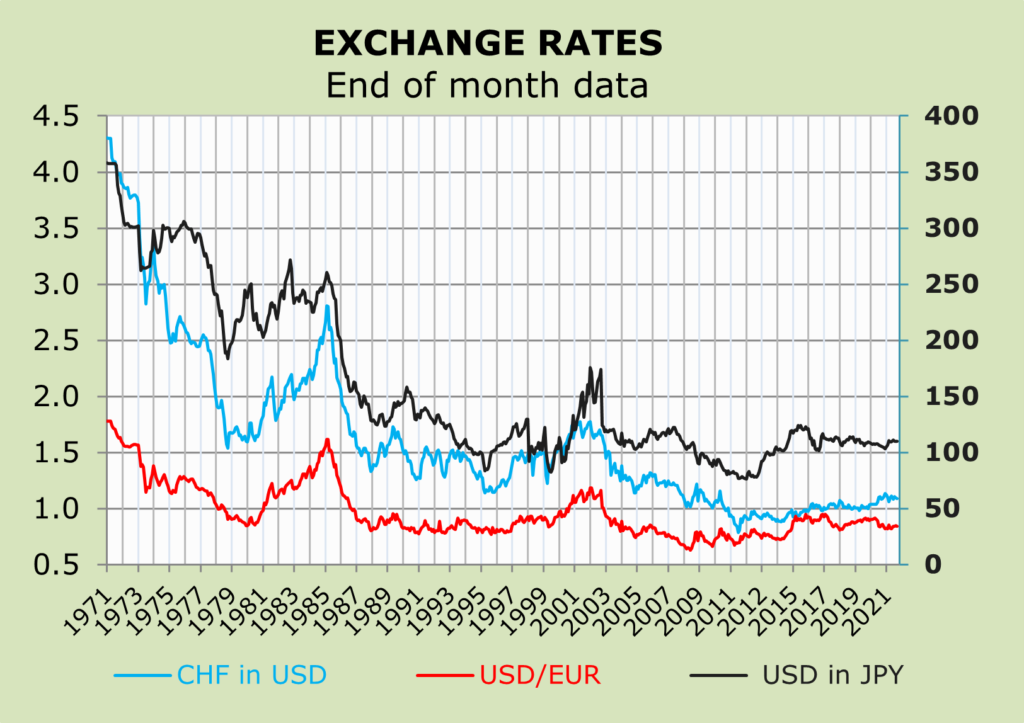

Keeping in mind that versus the USD, the CHF, the EUR and the JPY have fluctuated withing rather narrow bands, at this juncture we see no impending dangerous clouds in the currency sky.

Any suggestion is highly welcome.