EMR July 2022

Dear Reader

ECONOMIC FRAMEWORK

The current controversy is once again focused on the strategic role of interest rates and economic activity. Why, you might ask? Both variables provide a link between the financial environment and economic performance. They provide information about the interaction between the supply of savings and the demand for investment. Theoretically, there is broad agreement on the factors that influence interest rates. There is disagreement about the relative importance of the various instruments.

PRESENT SITUATION

We have no doubt that recent actions by, for example, the Federal Reserve Board to raise the fed funds rate (defined here as “i = interest rate” on banking sector deposits) should be seen as indicative of a tightening of monetary policy. How does this interplay work is the key question at this point?

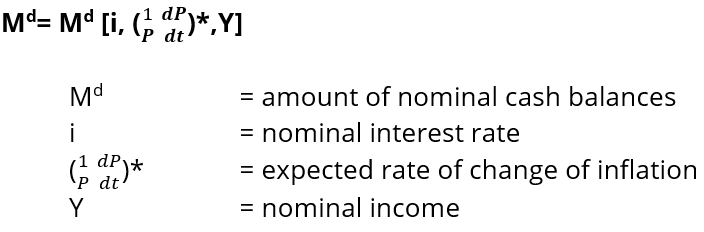

A simplified demand for money (Md) can be formulated as follows:

In other words: We speak of the “cost of holding cash” and, in particular in this context, of the cost of holding cash at the central bank. Both within the framework of economic theory and in ongoing, publicly available reporting, three deterministic effects can be derived:

- Price Expectations Effect (also known as the “Fisher Effect”),

- liquidity effect, and

- income effect.

We would like to emphasize that the function presented above is a highly simplified demand function. Nevertheless, it helps us to assess the current situation. We do not doubt that the Fisher or price expectations effect is particularly useful in the context of recent extraordinary central bank interventions. It explains the interdependence between interest rates and expected inflation. The two recent 0.75 % increases in the key interest rate were intended to reduce commercial banks’ overnight borrowing. When the central bank raises the key interest rate, it makes borrowing more expensive for both businesses and consumers by spending more on interest payments. An important effect of higher interest rates should be that they tend to lower inflation and prevent the economy from overheating. On the other hand, higher interest rates should also affect the stock market, while the price of existing bonds should fall. Consequently, new bond issues tend to offer investors higher interest income.

The liquidity effect is widely recognized in the context of monetary policy. In other words, it refers to the benefits that can be obtained by shifting money to assets.

Contextual changes in the money supply and interest rates can balance the actual and expected money supply. In the real world, however, one is confronted with the interactions of all the above determinants.

INSIGHTS FOR INVESTORS

When we look at the current environment, we see that the focus is on raising interest rates to counter inflationary pressures. The factual determinants of current inflation go almost unnoticed. If we assume that the rise in inflation is mainly due to factors (Covid-19 and the invasion of Ukraine) that have put dramatic downward pressure on crude oil and food prices above and beyond normal supply and demand trends, we should rather focus on how supply chain bottlenecks can be resolved. At this point, we believe that “extraordinary monetary tightening” could constrain demand without rapidly improving supply! Supply disruptions are expected to ease in coming quarters, while “financing costs” could rise.

We agree with Fed Chairman Powell that monetary authorities can manage demand, but not supply. Therefore, it would be worthwhile to distinguish companies whose prices move due to changes in demand from those that move due to changes in supply. In this context, we argue that the most promising investment approach would be the one that focuses on increasing supply while prices are falling.

The expected trigger is the quantification of the change in quantities and prices. We believe it is deterministic to focus on technological improvements as well as the adjustment of wages to the cost of living.

We advise investors to quantify the “expected turnaround” in global and local supply constraints, as we expect these to continue to be key determinants of the inflation trend and hopefully reverse it.

Comments are welcome.