EMR Feb. 2022

Dear Reader

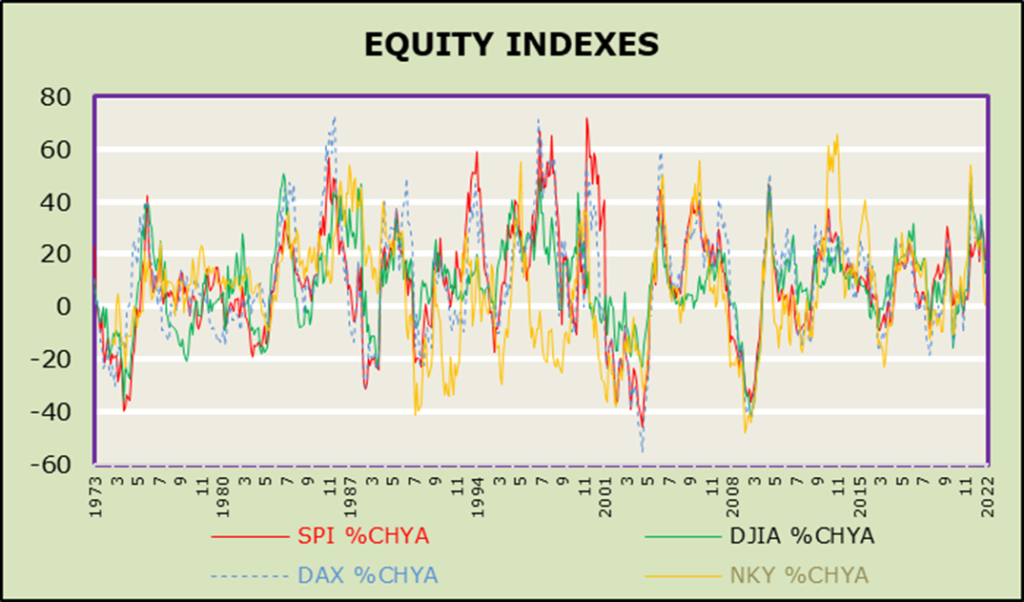

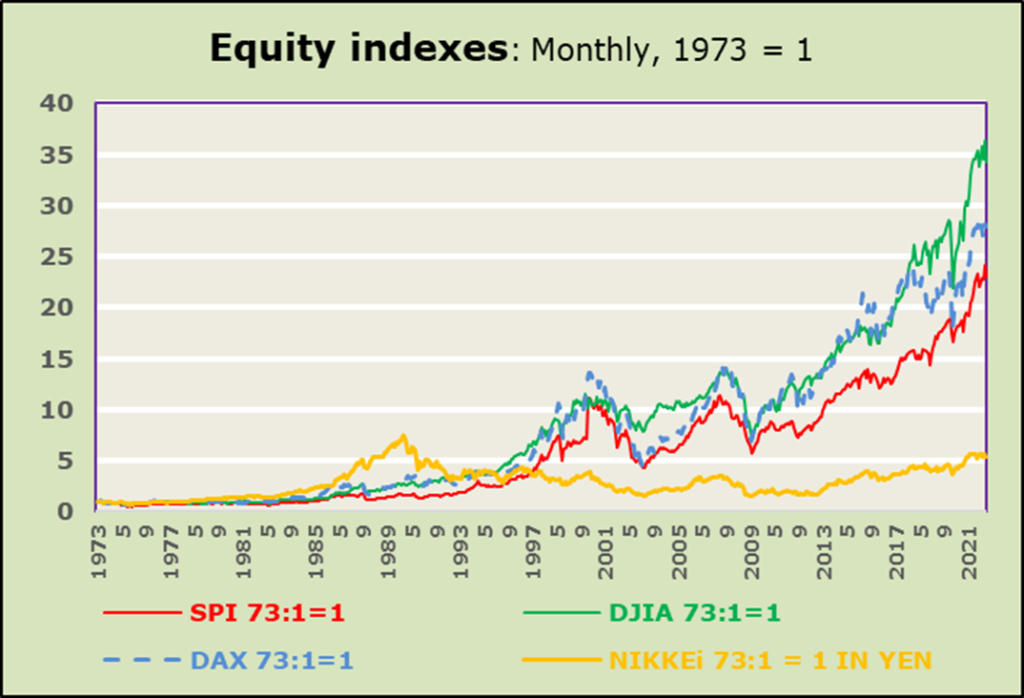

Most of our readers will recall the arguments put forward in the 1970‘s and 1980‘s concerning the world oil tank approaching empty. Then, as now, supply and demand were and are perceived as the reason for price increases. The developments of the 1990‘s are comparable to the current ones, but currently they are increasingly more complicated than during the previous oil crisis. The world economy faces several disruptive movers, which in a certain sense, render the current environment rather unprecedented, especially regarding its impacts on economic growth, inflation interest rates, employment and international trade. It´s a fact that many investors have turned significantly more pessimistic regarding the short to medium-term outlook. Our focus will be on equity markets, as implicitly shown in the chart of equity indexes: DJIA, SPI, DAX, FTSE, and N225.

What can be inferred from the charts? First of all, we find that the interpretation of past developments differs significantly when the focus is on percent changes on a year-over-year basis (first chart) as compared to the monthly level averages (second chart). The percent changes speak of significant volatility (see e.g. 1997 to 2003) while the chart of the monthly average levels speaks of significant long-term growth, particularly since 2009. Secondly, we find confirmation of a dramatic environmental change since the mid 1990‘s. Thirdly, the current pandemic Covid-19 situation is widely assumed to be inflationary. Fourthly, we have to take seriously into consideration that the differences to the oil-crisis are more intricate, both on the supply as well as the demand side of the economy. Our focus is not primarily on the long-term comparison as the shorter-term developments, i.e. since November 2019 into 2022.

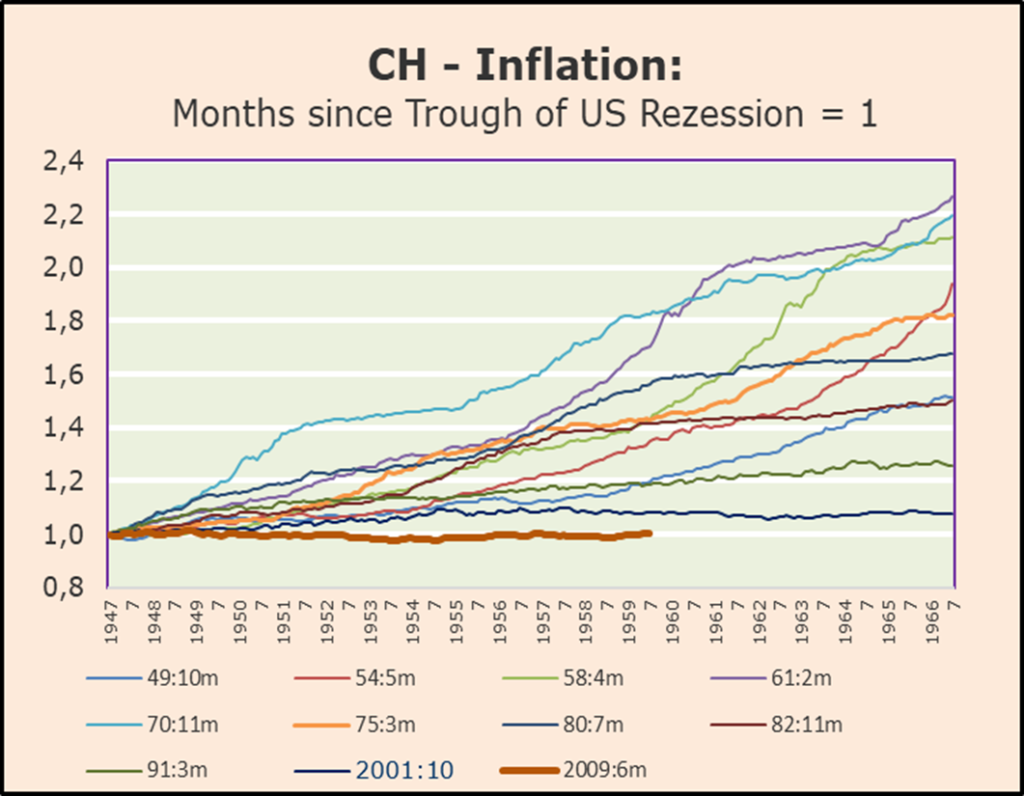

Given that recent hard economic data (for real GDP and components) are still missing, let us now turn to the implications on the demand as well as the supply-side of price changes, since the outbreak of the Covid-19 pandemic. Analyzing closely the performance of the Swiss consumer price index (CH CPI) along the lines of the US cycles for the period since 1949, will astonish most of the readers of this EMR and this due to the fact that the most recent cyclical growth rate of Swiss inflation is absolutely the weakest!

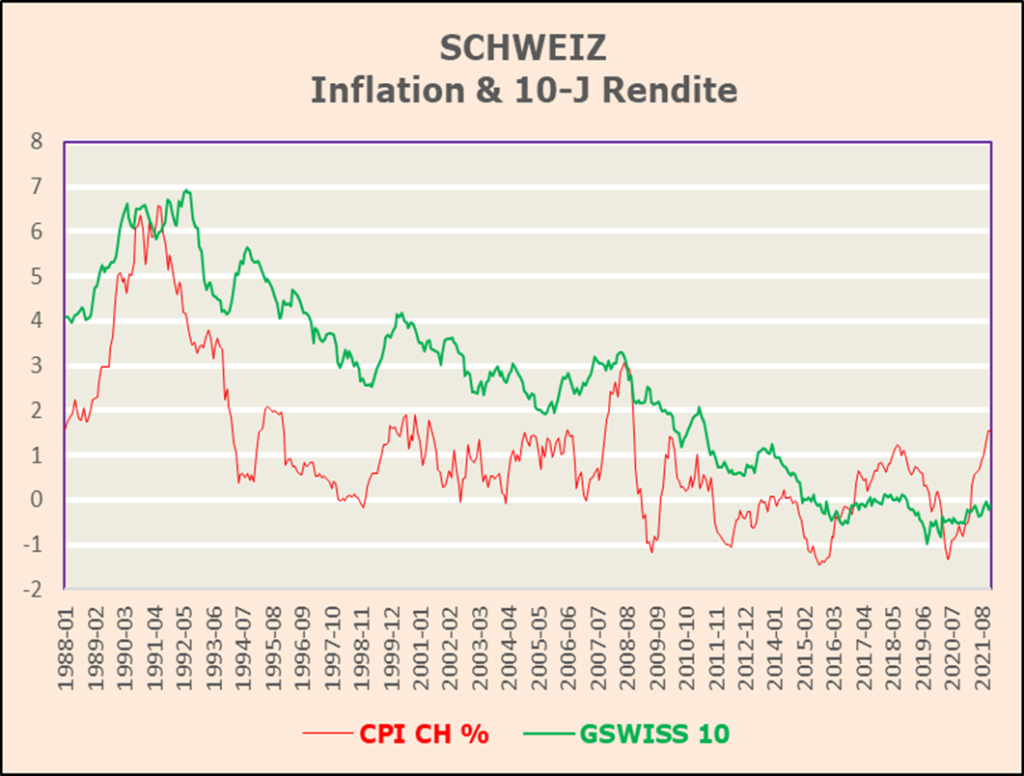

Comparing the recent inflation ups and downs, we find that since the top of August 1991 (6.57%) and the ensuing lower top of July 2008 (3.07%) rising to 1.53% in Dec. 2021 has not been accompanied by similar swings in the Swiss 10-year Government bond yields. The chart shows that since 1998 market participants were faced with a relative long period of price stability (despite short-term swings around 1%). At this juncture we stand at cross-roads. Will demand grow in the next quarters due to past liquidity injections by Governments and Central Banks, thus fostering consumption growth, and at the same time with improving imports of much needed tech-components? We believe that we ought also to take into account the expected domestic improvements on the supply side. In the short term this approach would imply profit maximization. At this time, we are not yet ready to subscribe to such a scenario. We believe that the comparison to the previous crude-oil crisis is not expected to be repeated. Why so? Well, we expect that shortages of imports of technological intermediates ought to come soon to an end, thus implying improving local production activity. In addition, taking progress – at various levels – toward solutions of the Covid-19 pandemic would speak for an improvement of economic activity feasible without significant inflation pressures.

Contextually, it is a fact that, e.g. in 2020, the US Federal Reserve has embarked on a policy of “Av-erage Inflation Targeting” as part of its long-run monetary strategy. We take note that recent in-creases of consumer prices in the USA and Europe have been strong indeed. Thus, in this EMR we will concentrate our analysis to the Swiss developments since January 2008. Swiss 10-year Govt. Bond Yields stood at minus 0.072% on January 2008. Subsequently they fell to a bottom of minus 0.975% on August 2010, to again “rise” to minus 0.127% in December 2021. The real question at this time is: will inflation rise to the levels of the comparable levels of the previous cycle or even higher? In such an unexpected case, inflation would definitively be a stock market negative. Interpreting the below shown charts one is confronted with a differ-ent perspective, aren´t we? Now let us recall that significant inflation acceleration in the past has been a negative. Given that in December 2021 the yearly rate of Swiss inflation amounts to 1.535%; matching the previous top of mid-2010, one has to fear or assume a dramatic rise over the medium term. We have a hard time to accept and to explain these negative expectations, mostly due the reliquification measures taken in recent quarters and the slow but ongoing economic revival of international trade developments in the mak-ing. The two most tricky assumptions to be made at this time, concern the adjustment process of “Gross private domestic investment, incl. Change in private inventories” and net Exports.

At this juncture we assume that Gross private domestic investment ought to grow substantially, in line with the significant past governmental reliquification. Enterprises have learned that international trade disruptions (not just due to Covid-19) but, more importantly, by foreign governmental difficulties, require a readjustment of domestic supply of intermediate technical goods and services. The scarcity of electronic components and the lengthening of delivery times are seen as a dangerous “limiting growth”-argument; very difficult to be quantified with sizable precision. Nevertheless, the contextual developments ought to yield support to the equity market and local employment.

On the other hand, consumer spending is expected, at least short-term, to be contained as governmental financing is scaled down. The Fed Chairman gave a special hint of this on January 26, 2022, by stating that the Fed was “determined” to raise interest rates in March to combat the highest inflation in decades. He also stated that there was a risk that inflation would not return to pre-pandemic levels in the foreseeable future and that price increases could accelerate. Consequently, we assume that real GDP is not expected to rise significantly over the next few quarters. Net export, on the other hand, are expected to support real GDP activity mostly via a systematic reduction of imports of intermediate tech-supplies.

The toxic mix of increasing inflation, consistently due to rising energy costs in conjunction with bottlenecks in the global distributive system, and the expected shift in industrial production will continue to determine the growth differential and trend from country to country.

CONCLUSION FOR THE INVESTMENT POLICY

History tells us that in times of accelerating inflation, rising interest rates and rather poor economic activity the stock market performs, to say the least, below the levels or the times of relative price stability (around 2% inflation).

In order to assess future developments, one must use a combination of many factors, subjective and objective, qualitative and quantitative. The current situation is not as easy as it could be, but if one assumes a modest economic recovery, one sees slightly higher interest rates, rather strong consumer demand as well as a resumption of international trade, and important shifts in the production environment both domestically as internationally. What are our contextual expectations?

- Equities stand once again to outperform bonds and money markets. The outperformance might not be as significant as it has been recently, but in any case, relatively promising. Sectoral selection will matter in terms of outperformance.

- Investment in fixed income securities ought to remain selective depending on the size and duration of interest rates moving higher.

- Currency adjustments must be factored in, in the international diversification approach.

- An unknown, which is not considered here concerns the conflict concerning the Ukraine. Depending of the specific whereabouts it could have devastating effects on the world economy and thus also on the financial markets.

Comments are welcome.