EMR June 2023

Dear Reader,

Due to the recent economic turmoil and diverging developments in the equity and foreign exchange markets, the economic environment in Switzerland, as in most other democratic countries, requires special attention. According to the latest press release of SECO (State Secretariat for Economic Affairs) of 30.05.2023, the economy is not yet in a recession compared to e.g. Germany. At the same time, Seco forecasts modest growth for 2023 and 2024, albeit at lower growth rates. The available data indicate a non-negligible economic resilience. The difficult international environment has slowed both manufacturing output and exports. Domestic demand, on the other hand, grew robustly, despite rising real import prices, especially in the energy sector. The available data show a non-negligible economic resilience. The challenging international environment curbed manufacturing output as well as exports. Domestic demand, on its part, showed robust growth, in spite of real import price increases, particularly in the energy segment.

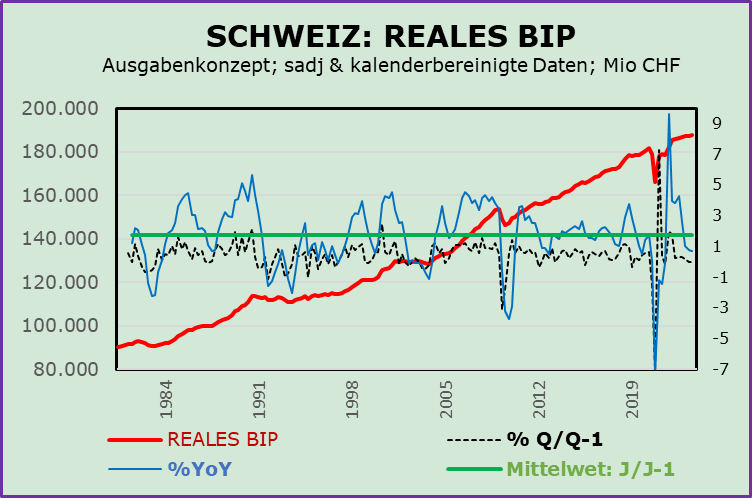

Examining the developments, as portrayed in the chart of Swiss real GDP, one can deduce the following:

1. The worst correction of the indexed real GDP, Q1 1981 = 1, took place in the second quarter of 2022!

2. The overall average change over the period 1981 to end 2022 amounts to 1.75%, compared to 0.82% in Q4 2022. It is worth noting that, compared with developments during the 2008-2009 financial crisis, the recent correction had a noteworthy, differential impact on real GDP. Investors should seriously consider the hoped-for or feared impact of the upcoming turnaround in favour of domestic production. The aim is to restore competitiveness in key technologies while increasing local production and productivity.

3. Noteworthy – in terms of forecasting relevance – is the comparison of the quarterly rate of changes vs. the yearly changes.

4. At this point, we advise investors to seriously consider the implications of reversing the trend in favor of domestic production in order to regain competitiveness in key technologies as part of the reconstruction process. Under the current circumstances, we ask ourselves what are or could be the main effects of today’s investment policy?

For simplicity, we focus here on the following two periods, i.e., between 2007 and 2009 and developments since 2019. We believe it is worthwhile to look at the sequence of the two crucial periods to draw appropriate conclusions for future asset allocation. Here are our key findings:

a) We believe it is advisable to closely examine the feared effects of a reversal in favor of domestic production in order to regain competitiveness in key technology stocks and rebuild local production and productivity.

b) The intervals between each “high” and subsequent “low” do not represent uniform fluctuations, neither in size nor in strength.

c) The variance of the individual growth phases (positive or negative) differs significantly from each other, both when evaluated on the basis of the respective index level and when adjusted to “1” on October 10, 1998.

d) In addition, it should be noted that the duration of the “correction phases” differ significantly from each other in both duration and extent.

e) The recent correction phase, due in particular to the Covid 19 pandemic and even more so to Russia´s war against Ukraine, has had and continues to have a devastating impact on international trade and on energy prices (both for crude oil and gas and for various industrial products). The associated price increases have led (and continue to lead) to price increases in consumer and industrial goods, due to the reduced availability of energy compared to all previous critical periods. The current environment is very difficult to adequately quantify in terms of the impact on asset allocation.

f) The time spans between a high and subsequent low do not all reflect coherent fluctuations, either in magnitude nor strength. Nevertheless, the data suggest increasingly large differences (between highs and lows). The magnitudes of the individual growth phases (positive and negative) differ significantly.

g) In the current correction phase the public attention remains focused on monetary policy, especially with regard to the expectation of higher interest rates. The fact is that the outlook for the financial environment is not easily comparable with developments in past decades. What the future demands is that various dislocations have created or will create a new need, namely the urgency for “greater strategic autonomy” in many sectors of democratic economies. In this context, the possibility of “repatriation” of production in the semiconductor sector, i.e., in the field of technology, should be increasingly considered. At this stage, the question arises as to what kind of economic leadership we are dealing with.

h) The periodicities between a high and subsequent low do not all reflect coherent fluctuations, either in magnitude or strength. Nevertheless, the data suggest increasingly large differences (between highs and lows).

i) While the current correction phase is primarily explained by rising consumer goods and energy prices, the public’s attention remains focused on monetary policy, especially with regard to the expectation of higher interest rates.

j) While the current correction phase is largely explained by rising consumer goods and energy prices, the public’s attention remains focused on monetary policy, especially with regard to the expectation of higher interest rates.

The thorny question that many analysts, and especially financial experts, are asking is, “How were we prepared in the face of this vulnerability?” Or, more proactively, “How are we preparing ourselves for the next phase of economic growth?” The fact is that the outlook of the financial environment is not easily comparable to the developments of past decades. What the future demands is that various dislocations have created or are going to create a new need, namely the urgency of “greater strategic autonomy” in many sectors of the democratic economies. In this context, the possibility of “repatriation” of production in the semiconductor sector, i.e., in the field of technology, should be increasingly considered. What economic leadership are we facing at this time, is the real question.

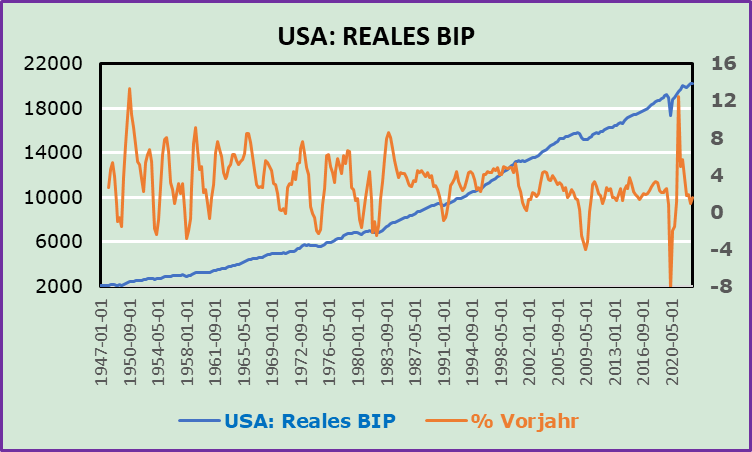

USA: GDP TRENDS

In most cases the outlook for the stock market can be predicted on the basis of real GDP growth and growth expectations. The following chart shows the evolution of economic activity in the United States since 1947. The data suggest that this might not be an easy task, as three distinct phases are implicitly known: the first from 1947 to 1984, the second from 1984 to 2018, and the third from 2018 to the first quarter of 2023. We emphasize that the current cycle (defined as the period starting in 2019) is the weakest and most volatile phase of them all.

PROSPECTS

We continue to believe that the economic outlook is difficult to quantify and yet remains deterministic, as illustrated by the two stock indices shown in the chart: “DJIA & SPI indices”. Again, we believe that the economic outlook should be analyzed in terms of external trade developments and the respective impact on consumer and capital spending. Accordingly, energy prices and especially the Russian war in Ukraine remain crucial. The most difficult question is how long the Russian war in Ukraine will last. This is definitely a sensitive issue, as it could remain an important determinant of inflation, which in turn and due course ought to influence central bank policy. We believe that consumer and investor expectations and activity will continue to be critical to central bank interest rate actions and reactions. This is definitely a thorny issue, which is hard to forecast with sizeable precision.

IMPLICATIONS FOR INVESTORS

We continue to expect several quarters of weak economic activity. Howev-er, a recession cannot and should not be ruled out, given the unquantifiable consequences of the Russian war in Ukraine and the associated impact on inflation and inflation expectations, as well as the interdependence with in-terest rates and related policies.

In the short term, despite rising volatility, we continue to view equities as promising, compared to fixed-income securities. After further interest rate hikes, a rebalancing may emerge over time. On the currency front, we continue to favor our local currency over the USD and EUR. The most promising investment advice one can give is to focus on high quality.

Comments are welcome.