EMR March 2021

A specific assessment of the economic whereabouts is known as static state: in other words, it implies slow growth and slow decline. What we would like to point out in this specific context is that history repeats itself, and this as a function of the political, economic and social constellation.

The hard question we would like to answer as realistically as possible refers to: the mutual determination between Government spending and foreign trade high – and growing -imbalances. Does this intricate constellation help the world economy to escape from a recession?

Editorial

Liebe Leserin, lieber Leser In diesem EMR gehen wir der Frage nach, in wieweit es möglich und signifikant die entgegengesetzten Entwicklungen der staatlichen Ausgabenpolitik und den jeweiligen Handelsungleichgewichten zu quantifizieren. Bekanntlich liegt der primäre Fokus der Ausgabenpakete auf die Ankurbelung der privaten Konsumausgaben jedoch ohne genügende Berücksichtigung der gegenläufigen Auswirkungen des internationalen Handels. Die Geldpolitik scheint sich nicht sonderlich, um die Möglichkeit einer signifikanten Zunahme der Inflation zu kümmern. Darüber hinaus sind die Behörden weiterhin mit den negativen Wachstumsauswirkungen der verschiedenen Arten von temporären Lockdowns konfrontiert. Dies sind wichtige Bestimmungsfaktoren für die kurz-, mittel- und langfristige Wirtschaftsaktivität, Entscheidend, wenn auch sehr schwer quantifizierbar sind die Auswirkungen der Fiskalpakete auf Investitionen in Infrastrukturprojekte. Hierüber wird wenig geschrieben, obwohl es um den Fiskalmultiplikator geht, der für eine starke Stimulierung der Wirtschaft über "1" liegen müsste. Anzunehmen ist, dass der Multiplikator deutlich größer wäre, wenn die Staatsausgaben auf die Förderung von Investitionen in die Infrastruktur ausgerichtet wären anstatt auf Konsumausgaben. In diesem EMR liegt der Fokus auf der USA und der Schweiz. Freundliche Grüsse, Adriano G.E. Zanoni, Ph.D. Chairman

Political setting

In the short term, the policy focus will remain on resolving the pandemic caused by Covid-19. The daily data available on the impact on the economy remains difficult to quantify, making serious economic forecasting problematic indeed and, in some cases, highly contradictory. Our assessment is primarily driven by the feasibility of a rapid and sustained revival of economic activity through the “reopening” of most vital sectors of the economy. But there is no doubt that the negative economic consequences of Covid-19 have been disproportionately severe and, and, strangely enough, they could remain prevalent for some time. The corresponding quantitative inter-actions are foreseeable, and not just for low-wage workers. The interplay of these rather contradictory viewpoints should by no means be underestimated. Coherently, we assume a period of persistent uncertainty and volatility.

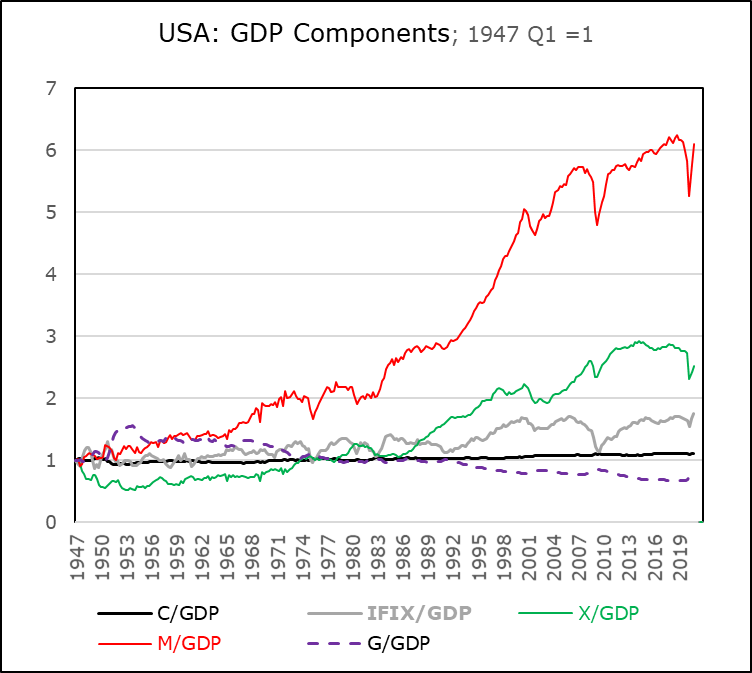

Disequilibria

The graphs of the corresponding components of real GDP for the U.S.A. and Switzerland are revealing indeed. This is not only true with regard to the different periods of the respective business cycles.

One major difference relates to foreign trade. The ratio of exports to imports is not only negative for the USA compared with Switzerland, it is also one of the most important determinants of the overall economic growth rate. In context, we sense a growing unease among policymakers and the public. This is due to the fact that trade deficits are undesirable as they crowd out domestic production and are certainly detrimental to jobs and workers. One of the most deterministic effects of trade imbalances is their influence on the productive sectors of the economy. It is well known that goods markets are competitive, while international trade is subject to trade costs that are a sensitive decision factor in terms of future economic and employment growth. A further important difference is the weakness of the domestic growth contribution of consumer spending, business fixed investment and government spending as compared to the losses due to trade imbalance.

in: 2021 GDP indexed

The two above shown charts speak of dramatic environmental changes over the past 20-30 years, depending on the component. They clearly imply the significant counterproductive developments of the trade imbalance.

Possible adjustments

Now, we know that the American voters did not appreciate the policy of the previous Administration to significantly contain imports growth and at the same time to boost domestic production in order to increase employment.

The fact is that the ratio of US consumer spending to GDP has been relatively stable since 1947: fluctuating between a low of 0,927 (in Q1 1952) and a high of 1,108 (in Q3, 2019) showing an increase of 19%). Imports on the other hand rose from a low of 0.908 (in Q3 1947) to a high of 6,247 (in Q4, 2018) representing an increase of 588%! What these numbers undoubtedly imply is that the focus of the Biden Administration on busting consumer spending does not promise neither a fast nor a sustainable support to the much a promised rebalancing of the above shown imbalances. We fear that “helicopter money” will boost imports from low-cost countries such as China and other low-cost producers, fueling the imbalance to even higher, unsustainable levels. Before long, the new US-Administration will have to address the negatively skewed situation. In the Swiss case, one can assume that the much-hoped increase in economic activity will further boost Swiss exports growth. Such a scenario speaks for improving employment while lowering the unemployment rate in Switzerland.

Should the implicitly above assumed scenario materialize, it would undoubtedly require active currency management, as so disparate economic growth rates together with the enormous amount of “helicopter money” would imply significant interest rate adjustments. This scenario, if it materializes, would be a deterministic factor of a promising asset allocation process. What would it mean for currency adjustments? The following chart suggests that we should start thinking about a currency reversal. Focusing, as implicitly summarized in our (above) overall assessment, we feal that whit the endogenization of the huge trade imbalances, we ought to assess its impact on the labor market.

Deterministic will also be the assumption of shifts between sectors; important for quantifying expected discounted profits. What should not be underestimated is that goods markets are perfectly competitive, while international trade involves specific trade costs. A relevant indicator of these developments will be visible in the relocation of relevant manufacturing jobs. Although the environment remains positive, thanks to the loose central bank policy and the strong fiscal stimulus, we expect that on the one hand assets can benefit from the economic acceleration and higher (?) inflation, while on the other hand market participants increasingly fear an equity price correction.

Asset allocation

While the focus of financial investors is on “reflation,” we remain somewhat less optimistic due to the conflicting effects of loose fiscal and monetary policy vs. the impact of increased imports. We assume that both consumers and entrepreneurs will focus on cheaper imports of goods and services. Foreign trade is expected to significantly reduce the effect of the Biden spending plan. In addition, we must assume that the cost of unemployment will cause considerable volatility.

The macroeconomic shift in international trade and developments in vaccines, along with the recent historic rise in equity prices, ask the question of what comes next? Well, short-term active management and increased attention to currency fluctuations do indeed seem promising. Interest rates and currency adjustments are in the driver’s seat of a promising investment strategy; both domestically and internationally. With interest rates expected to rise significantly over the next 6-12 months, they are likely to curb the attractiveness of fixed income instruments. Our regional focus remains locally skewed as the CHF is expected to strengthen against USD, EUR, GBP and JPY. Gold is somehow viewed as a potential hedge vehicle, at least until it become clear what policy the Biden administration will actually embark on.