EMR August 2023

Dear Reader

What can be inferred from the following chart of the Dow Jones Index, based on publicly available data?

- Does the chart say anything about the appropriate environment for equity commitments?

- Is the current rather pessimistic assessment something new and therefore pointing to a somewhat unique constellation, or

- Are there historical periods that can help explain the current state of the economy?

The graph indicates that the DJIA’s performance has been quite poor in both years of inflation and deflation, while in years of relative price stability the DJIA has performed quite well. However, the implied data do not take into account the loss of purchasing power, which could result in a higher positive or negative compound return for the respective investment.

The annual inflation rate, as pointed out in the above chart, is revealing, is it not? Looking at the long-term graphical trend of annual inflation rates from 1983 onward, there is a sharp contrast to the long-term story. However, media attention is mainly focused on recent developments and the prolonged period of relative stability (since the early 1980s), pointing to “declining and rather stable” inflation rates! Recall that previous highs occurred in 1812, during the Mexican War of 1846-48, during the Civil War of 1861-1865, World War I of 1914-1918 and World War II of 1939-1945, as well as the subsequent Korean War of 1950-1953 and the Vietnam War of 1955-1975. Subsequent political and economic turmoil did not lead to similar increases in inflation rates. Economic turmoil did not lead to similar increases in inflation rates.

SOURCES OF INFLATION

In economics, the main causes of inflation are grouped into three specific categories:

- Cost push,

- Demand push and

- Inflation expectations.

Widespread skepticism, not only of analysts, speaks of a likely, economic “hard landing”. These expectations can primarily be explained by foretold interest rate hikes by the monetary authorities. The immediate result is a further increase in uncertainty. At this point, let us take a closer look at what are the real sources of the feared rise in inflation. For this purpose, we rely on the following chart.

Rising prices of domestic and/or imported goods, as seen recently, have driven up consumer goods and production costs. These developments are reflected in rising consumer and producer price indexes in Switzerland and the United States, as shown in the following graph.

Normally, the main causes of inflation are classified as in the diagram above. As pointed out in previous EMRs, we believe that in the current economic phase the main inflationary cause lies in the cost of commodities as a result of the significant reduction in supplies, for example, of crude oil and raw materials. All economies have been affected by declining supplies of many industrial and consumer goods. One concrete indication has been and continues to be the increase in crude oil prices due to Russia’s war against Ukraine and the need and obligation to reduce dependence on imports from hostile countries such as China and Russia. Another contributing factor is the wrong decision to relocate production to producers with lower production prices, such as chip production in the Far East.

DEMAND PULL

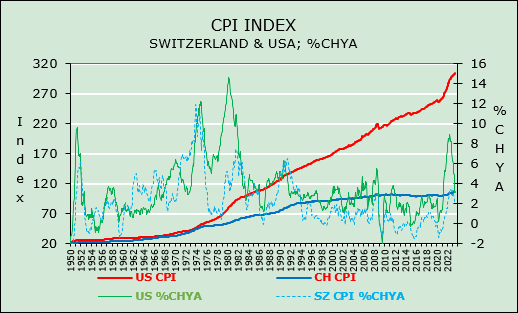

Rising prices of domestic and/or imported goods, as seen recently, have driven up the costs of consumer and production goods. These developments are reflected in the rise of consumer and producer price indexes e.g., in Switzerland and the United States, as shown in the graph below.

Considering the evolution of consumer price indexes in the United States and Switzerland since 1980, the following emerges:

- The implied growth rates of the indices presented show significant growth disparities. Between January 1950 and June 2023, the U.S. CPI increased by 1’190%, while the Swiss CPI increased by only 100.9%. A truly remarkable discrepancy!

- The trend in annual rates of change (on a monthly basis) shows a rather surprising development. The differences in the rates of change are really surprising. For example, the Swiss CPI peaked at 11.57% in January 1974, while the U.S. CPI reached 14.59% in March 1980.

- Recent inflation hikes have not been as pronounced. In June 2022, the U.S. CPI peaked at 8.93 percent, while the corresponding peak of the Swiss CPI was measured at 3.45 percent in August 2022.

These developments suggest that the real problem is not inflation itself, but rather its determinants.

EXPECTATION ON COST-PUSH INFLATION

An increase in the price of domestic and/or foreign inputs (such as crude oil or raw and basic materials) leads to an increase in domestic production costs. Firms that face higher costs to produce each unit of output tend to produce less and/or raise the prices of their goods and services. This can have cascading effects on the prices of other goods and services. For example, an increase in the price of oil, which is an important factor of production in many sectors of the economy, initially leads to an increase in the price of gasoline. Higher gasoline prices in turn make it more expensive to transport goods from one place to another, which in turn leads to higher prices for products such as food.

Cost-driven inflation can also occur as a result of supply disruptions in some sectors, such as due to unusual weather conditions or natural disasters. Large hurricanes and floods regularly occur, damaging large quantities of agricultural products and causing significant increases in food prices, which temporarily leads to higher inflation.

IMPORTED INFLATION AND THE EXCHANGE RATE

Exchange rate fluctuations can also affect prices. A depreciation of the do-mestic currency increases inflation in two ways. First, the prices of goods and services produced abroad rise relative to those produced domestically. As a result, consumers have to pay more to purchase the same imported products, and firms that rely on imported materials in their production pro-cesses pay more to purchase these inputs. Price increases in imported goods and services contribute directly to inflation through the cost-push channel.

Second, a depreciation of the currency stimulates aggregate demand. This happens because exports become relatively cheaper for foreigners, leading to an increase in demand for exports and higher aggregate demand. At the same time, domestic consumers and businesses reduce their consumption of relatively expensive imports and shift their purchases to domestically produced goods and services, which in turn leads to an increase in aggre-gate demand. This increase in aggregate demand puts pressure on domes-tic production capacity and increases the scope for domestic firms to raise their prices. These price increases indirectly contribute to inflation via the demand-pull channel.

In terms of imported Inflation, the exchange rate has a greater influence on inflation through the respective effects on prices of goods and services that are exported and/or imported (so-called tradable goods and services), while the prices of non-tradable goods and services depend more on do-mestic development.

IMPLICATIONS FOR INVESTMENT POLICY

The context outlined portends a rather difficult environment. Investing requires careful attention and consistent examination of the determinants of one’s investment position. This concerns both trading dynamics and long-term needs and requirements. It is no longer sufficient to focus on the monetary policy actions of central banks, both in terms of managing the money supply and fine-tuning interest rates. What is required is a specific knowledge of causes of inflation be they demand-pull, cost-push, or due to inflation expectations—or due to domestic and/or foreign policy constraints. A concrete assessment of the near future remains a cause of great concern.

The main arguments of our deterministic view lie in the need for repatriation of most vital production goods due to energy policy constraints as well as the production of critical metals—in particular to reduce supply bottlenecks for oil and natural gas. In this context, strong exchange rate fluctuations are to be expected, which could limit international diversification. In addition, there are fears about possible sanctions, which are difficult to assess. For these reasons, we are placing our investment, as far as possible, in the domestic market. Should the USD continue to depreciate against the CHF we would see it as another serious concern.

Nevertheless, our expectations remain cautiously positive, because overall demand is likely to increase due to rising spending by consumers, companies and even the government.

An important determinant is and remains the development of foreign trade.

Comments are welcome.