EMR February 2023

Dear Reader

UNKNOWN = BIG CHANGES?

With its invasion of Ukraine, Putin’s Russia has challenged the balance that persisted since the end of the Cold War. Recently, the world has entered a very mixed phase of transition. We believe that this situation will persist in having a significant impact on consumption, investments, international trade, and currencies. This situation is expected to require a continuous updating of the investment policy.

The fact is that, in 2022, both the USD and CHF were among the few asset classes that tended to be spared from the Covid 19 pandemic and Russia’s war against an independent country. Rising inflation has been a worrisome side effect, mainly monitored by the Federal Reserve. At present, the focus is increasingly set on the whereabouts of economic activity. A growing number of analysts fear an imminent recessionary phase, including continued currency adjustments, as a consequence of the differentiated monetary policies.

CONSEQUENCES

Undoubtedly, the Russian invasion of Ukraine will force the economies of the free world to reduce their dependence on autocratic, pro-communist countries as quickly as possible. This is bound to entail, for example, a return to local production of many goods and services and an orientation toward other producers of oil, gas, etc.

First signs of this change are visible in the U.S. technology industry. See:: Chips Act [1], in which special attention is given to short-term inflationary pressures and thus to the specific responses of central banks. In Europe, too, there are proposals that go in the same direction, although there are still differences from country to country. There is no doubt that the invasion of Ukraine is a sign of an increasingly inevitable “de-globalization.”

Geopolitical tensions aside, the impact on international trade, and thus on consumption and investment, needs to be carefully monitored. The dreaded volatility of energy and gas prices will remain a source of confusion, both in terms of economic growth as a function of inflation, and in terms of the ups and downs of international trade, which currently speaks of continued volatility, and not just in the financial markets.

There is another serious difficulty: the increasing and high indebtedness of countries, companies and the general public. Fortunately, the current situation does not resemble that of the late 1970s, when Paul Volcker, chairman of the FED, was forced to intervene aggressively to fight inflation.

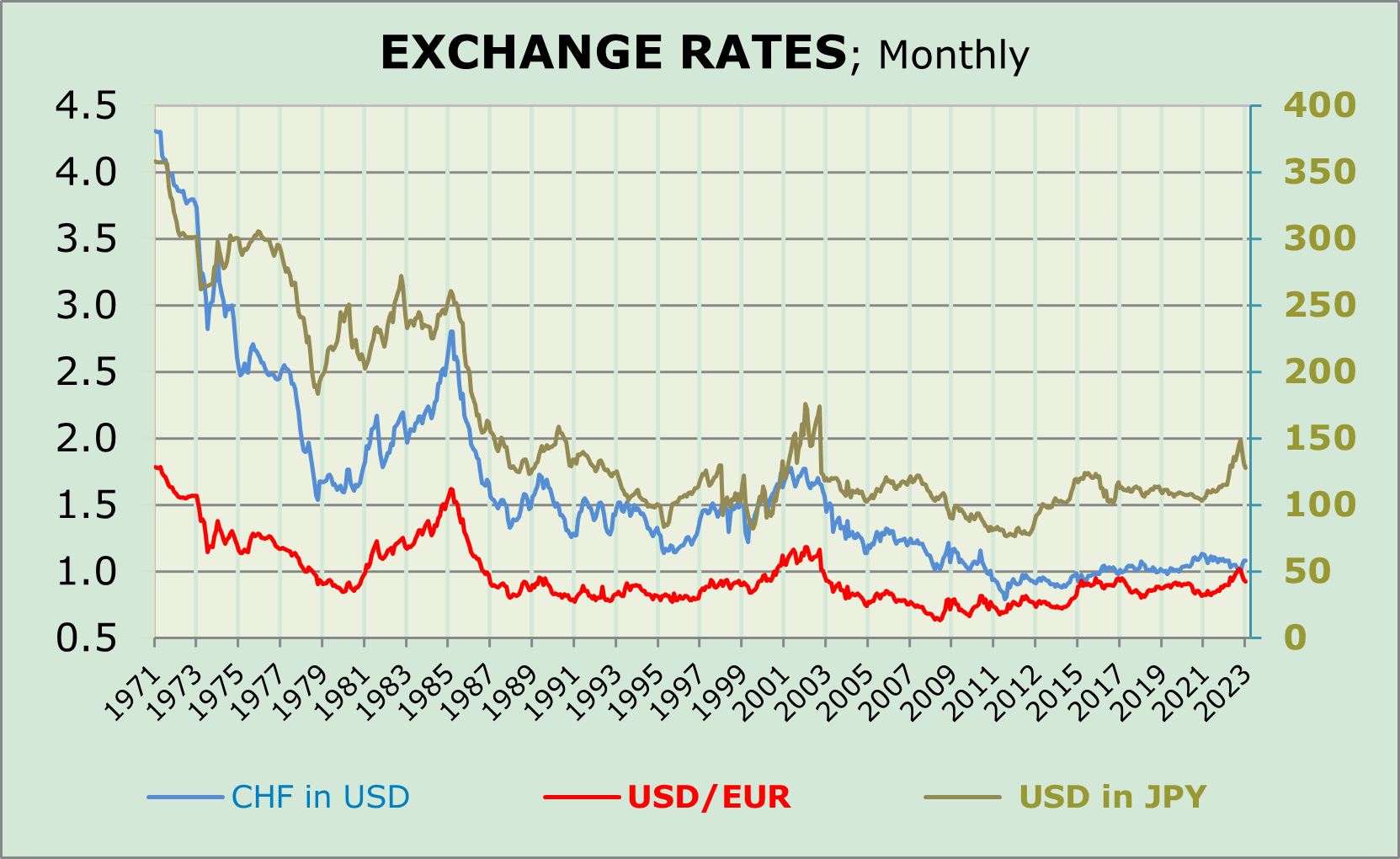

In terms of international diversification, one should seriously consider the possible developments of the leading currencies. See the graph below.

At this point, we wonder what can be inferred from the graph concerning the average, annual changes in monthly exchange rate fluctuations. We note that the differences in performance are indeed significant, as they could continue to determine the respective ups and downs as well as volatility.

OUTLOOK 2023

The environment outlined above clearly indicates a dramatic change in the environment. Until recently, the focus was on fighting inflation; now the focus is much more on “repatriating” production. This is evident, for example, in the stimulus proposals (Inflation reduction ACT [IRA], Chips and Science Act, and Bipartisan Infrastructure Law). Thus, the focus is clearly on renewable energy, semiconductors, and infrastructure, i.e., promoting local economic growth while reducing dependence on foreign manufacturers.

In both the United States and Europe, economic policy is no longer primarily focused on fighting inflation, but rather on rapidly renewing the domestic manufacturing sector to reduce dependence on imports from foreign manufacturers. This, if implemented coherently, would lead to a significant increase in local employment and economic activity. The specific objective is, among other things, to reduce dependence on China.

At this stage, our forecasts can be considered somewhat more optimistic than those currently circulating in the press. To some extent, our assessment is confirmed by a contradictory political attitude that is no longer so much determined by “cheaper producers” as by “administrators” or simply by the “free market” or, at best, by an egalitarian mixture of both approaches.

FINDINGS FOR INVESTORS

Assuming that investment growth will replace government spending as the main determinant of future economic activity, one needs to look beyond inflation ex-pectations and trends to define a successful investment approach. Therefore, we argue as follows:

- The era of runaway inflation is almost over; more price stability needs to be considered.

- If our assumption that inflation will no longer rise so sharply is correct, fixed-income investments could retain some attractiveness, at least in the short to medium term.

- Looking at the equity allocation as a result of the first paragraph of the of the “Consequences”, comment above, the focus on technology stocks, undoubt-edly looks more promising than any other sector.

- We continue to think the CHF is promising, as well as the USD.

Comments are welcome.

[1] In July 2022, Congress passed the CHIPS Act of 2022 to strengthen domestic semiconductor manufacturing, design and research, fortify the economy and national security, and reinforce America’s chip supply chains.