Recently, the policy focus has primarily been set on interest rate regulations. We, on our part, have repeatedly tended to disagree with the widespread consensus. Consequently, the focus of the present EMR is set on interest rate developments, and specifically on selected 10-year Government bond yields as plausible indicators.

FACTS AND INTERPRETATIONS

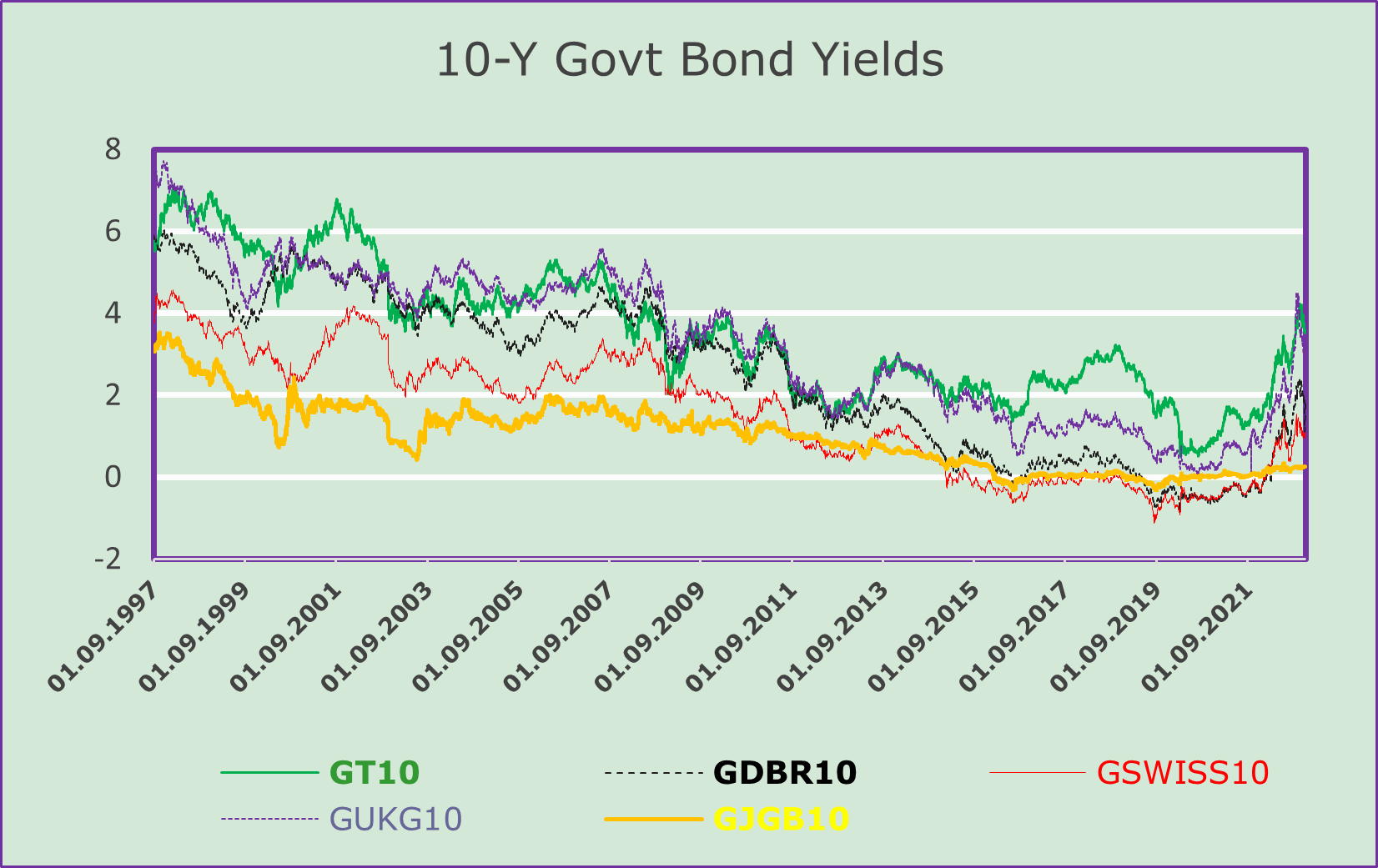

In order to show, why our assessment differs from the mainstream opinion, we present graphs of 10-year government bond yields of selected equity markets. The graphs of the pertinent interest rates, show significant developments, concerning the two most recent periods under examination. The following two charts point to the following significant disparities:

A differential path between the first half of the chart as compared to the second half.

The differential performance is significantly more pronounced in the second half, i.e. the most recent period.

The real question we ask ourselves is: what are the reasons for the disparate divergencies?

Examining the charts, we find that the performances are significantly more pronounced on the righthand of the chart; indexed to 1 on June 1, 2016. Why so, is the real question, is it not?

Recently, as we all know, economic policy has primarily been focused on managing inflation through interest rate adjustments by the respective Central Banks. As can be inferred from the shown charts, inflation has not received the attention it deserves from a large majority of analysts. To some extent, we fear that the current political environment is not sufficiently geared toward resolving the current economic stalemate with a significantly more coordinated approach.

We are aware of the fact that an evaluation of the current context, only on the basis of the above restricted representations, is a really complex task, as there are differences between the determining factors of the respective time series, such as:

Will Russia’s war against Ukraine and the wars in the Persian Gulf soon be over?

Will the outlook act as a driver of economic growth, or will politics continue to play the main destructive role?

Will the focus be mainly set on monetary policy and the corresponding actions of the respective central banks?

Or is, and ought to be, the traditional economic thinking be the “new leader”?

We are constantly told that the evolution of interest rates is fundamental to curbing the feared rise of inflation. Based on the available data, we wonder, which of the above hypotheses should and will actually be the valid and deterministic argument for the year 2026.

The recent focus of economic policy has been on managing inflation primordially by means of interest rate management by the Central Banks. Nevertheless, we disagree with this widespread assumption, implying that increased interest rates would solve the current economic impasse.

The graphs somehow puzzle us; thus, let us pinpoint the intriguing whereabouts.

As portrayed, the charts show two specific developments. One covering the period prior end 2019 early 2020 and the second the period thereafter. We find the specific developments as highly revealing.

CONCLUSIONS

Despite all the difficulties in forecasting, we prefer the Swiss franc and our domestic market – primarily for reasons of efficiency. We expect the CHF to remain in high demand. As can be deduced from the general conditions mentioned above, the war in Ukraine and the situation in the Middle East, particularly from a security perspective, are highly deterministic factors given their devastating impact on the availability of commodities such as gas and crude oil.

International diversification speaks for itself. In line with technological developments, investments in the US remain attractive despite the anticipated weakness of the USD against our own currency. Regarding EUR exposure, we are concerned due to the political uncertainties in France and Germany.

Will the focus continue to be primarily on monetary policy and the corresponding responses of central banks, and will this remain the case in the future?

Assessing the main determinants of economic developments has become extremely difficult, both in terms of duration and cyclical importance. As repeatedly pointed out in previous EMRs, we would like to state once again that the available long-term data, e.g., those on U.S. GDP, really seem to support our view that the outlook is not primarily as expressed by main stream analysts.

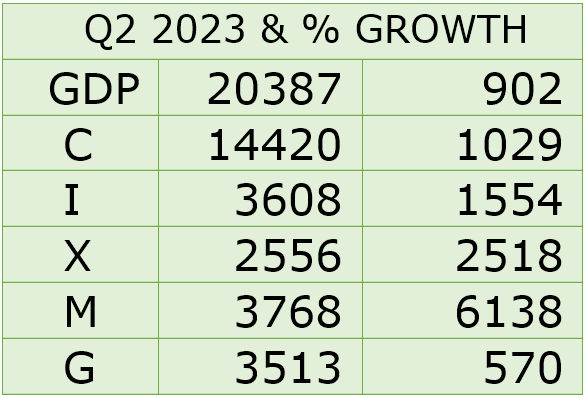

In order to explain what we mean; we kindly ask the reader to examine the following chart and accompanying table of US real Gross Domestic Product for the period 1947 to 2023. What we discover is puzzling indeed and at the same time highly revealing.

The chart on the levels of the major components of real GDP show the following:

1. Real consumer spending has been sitting, all along, in the driver`s seat, although its contribution to overall growth activity points to a slightly less pronounced growth performance, as compared to overall GDP. Contextually shouldn`t we speak of some weakness?

2. All other components seem to haven`t contributed much to overall economic activity; representing an astonishing development!

From the chart it can be deduced that the largest contribution to long-term GDP growth resides with consumer spending. Nevertheless, the chart points to an overtime less important average contribution. Overtime Consumer spending has tended to be less pronounced, that is, less propulsive. The divarication grew over-time. The growth differential is evident in the graph, while all other components of GDP seem to make only marginal contributions. Whether this assessment is “right” or “wrong” as a measure of the respective levels is at this time the appropriate question, is it not?

At this crossing we ask ourselves what this analysis implies both for the short as well as the longer-term outlook. Is the “level-comparison” the appropriate measure or are there other ways to assess the outlook?

For simplicity let us define the various variables in the Chart and Table: GDP stands for Gross Domestic Product. C for Consumer Spending, I for Investments, X for Export, M for Imports, and G for government Spending.

In US real GDP Table 12

Examining the chart and the table on US GDP & Components over the period since 1947, we wonder which component of U.S. GDP has really contributed most to overall growth? What can be inferred – both from the chart and the table – regarding the specific longer-term as well as shorter-term developments, in connection with the implemented policies on a worldwide scale?

Which component of GDP ought to get specific attention regarding the near-term outlook, most specifically in conjunction with monetary finetuning. A prima vista, on a level basis, as shown above, consumer spending speaks a clear language, doesn´t it? Nevertheless, we ask ourselves: Is this a correct way to analyze the most probable outcome, or are there other more important factors that ought to be taken into serious consideration? Yes we do, there are other telling variables. Interpreting the official data on US GDP and its main components requires a special focus of the developments of the international data set and particularly of imports and significanltly less so towards conumer spending. The calculated growth developments show, for the period since 1947 to an overall growth ratte of 6138 percent; 752.2 percent since 1980, 102.2 percent since 2000, and 14.3 percent since 2020.

The highest growth rates are to be found in imports and exports, followed by consumer spending! Nevertheless the policy approach remains intrinsically focused on further interest rate increases to reduce demand pressures, and with it inflation. Funny assumption is`t it? Foreign trade stands signficantly more for supply growth determinants of future policy developments and targets. We wonder why the focus continues to be set on local demand?

We persist in disagreeing with the widespread public assessment, that inflation can be managed via demand constraints. Recent developments clearly speak of rising electricity costs, rising transportation costs, rising gas prices, rising health care and insurance costs, and also a rising need to re-patriate some production lines (primarily in the technological field), etc., all determinants that focus mostly on domestic policies while inflation continues to remain primarily supply side determined.

EXPECTATIONS

In this intricate period, our scenario remains mainly determined by uncer-tainty and is therefore difficult to be implemented especially in the short to medium term. Monetary authorities are mainly concerned with restoring price stability.

INVESTMENT POLICY

At this time, investors expect further interest rate hikes as well as further exchange rate adjustments. As Swiss investors, with a relatively high home bias, we continue to expect the CHF to outperform the EUR and USD. In addition, we are concerned about the weakness of the European economy, which is largely due to German weakness, and the ongoing difficulties in China.

Nevertheless, the current assumption, concerns stagflation. The global economy is suffering from a weak economic outlook and inflation that is difficult to control, especially by means of rising and rising interest rates. A growing number of analysts are asking themselves how inflation can be re-duced primarily on the basis of further interest rate increases? Our answer, as also expressed in previous EMRs, requires a rapid reduction in specific imports – especially oil and gas – and an increase in domestic production of vital goods. The expressed arguments are our main reasons to set the main focus on investment in our local market, especially taking into account ex-pected-feared currency changes and, also, the technological developments that will be triggered by an increasing focus on domestic activities.

Although the impact of policy changes might affect mainly the medium- to long-term perspectives, we believe that it will mandatory to monitor a feared economic recession. At this stage, our outlook continues to be de-termined also by the outcome of Russia’s war with Ukraine.

What has the “Buridan Donkey Paradox” to do with today`s economic assessments? Well, it stands for “when choosing not to choose becomes a bad choice”. It is a figure of speech referring to someone who, when faced with two equally valuable alternatives, does not make up his mind to choose one of them.

Examining the current investment setting, we are faced with an increasingly intricate and highly deterministic policy choice. Should we analyze the current outlook primarily from the demand side or the supply side? The public debate is undoubtedly preponderantly focused on the demand side. Even representatives of Central Banks overwhelmingly favor the demand-side approach. The sequence of interest rate hikes undertaken since mid-2022 speaks volumes, doesn`t it? The thorniest question to be answered, regarding the current “policy setting”, concerns expectations of an imminent adaptation, or possibly a reversal of monetary policy actions in order to avoid a feared economic recession?

On the supply side, the argument points to a growing need to explore new avenues of corporate finance. The requests are rather independent from the availability of liquidity or further monetary actions, while they increasingly point to new and growing needs of a changing economic environment.

So far, the outcome of this rather difficult assessment remains focused, preponderantly on a further reduction of the rate of inflation and, on the other hand, on hopes for an upswing in economic activity, which should result, in due course, also in further significant currency adjustments.

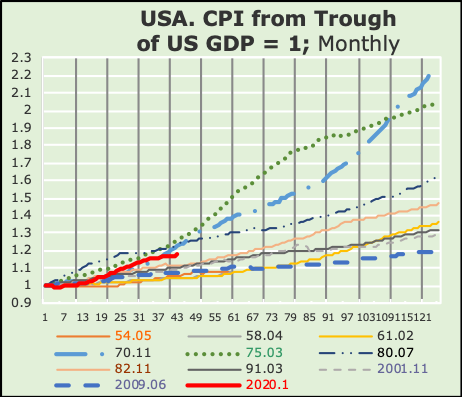

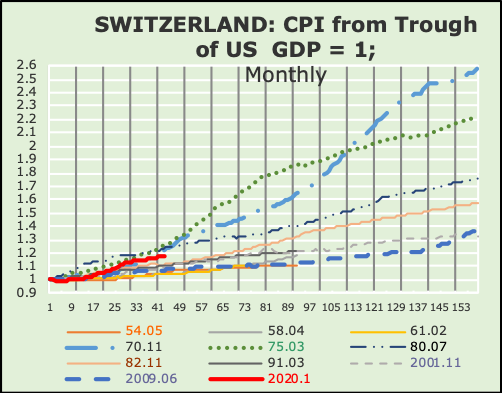

The dilemma can be implicitly derived from the chart of Swiss and U.S. inflation. The respective series are indexed to 1 for each specific cycle trough of US real GDP. The series portrayed in the chart show that, so far in the current cycle, inflation has fared better than for the cycles beginning in July 1980 as well as November 1970 and also March 1975.

CAUSES OF INFLATION

We cannot fully subscribe to the widely held view that the current economic setting ought to be primordially analyzed as a function of the “demand side” of the economy. Clearly, both consumer spending and business fixed investment as well as the respective balances of trade have required the known actions/reactions by the monetary authorities.

It is a known fact that both the Covid pandemic as well as the Russian war in the Ukraine have had, and continue to have a significant impact on the rate of inflation, economic activity as well as on currencies. We believe that these deterministic factors can hardly be managed solely by means of higher interest rates. In addition, the impact on international trade, as well as, the reorganization of economic transfer channels is hardly manageable by ever-higher interest rates.

We are not alone in assuming that inflation could persist regardless of monetary policy measures, and not only because of actions and reactions by Western economies. There are also increasingly explicit negative effects in the Chinese economy.

We assume that the monetary authorities ought not to be expected to remain prisoners of the metaphor of the Buridan Donkey. They will have to take the recessionary dangers into consideration. In other words, we would argue that, from now on, interest rate increases ought to be more moderate and coordinated with measures supporting a revival of economic activity. We assume that before long the focus will increasingly be on measures of revitalization of the domestic economic activity, while reducing the dependence on centralist states.

What can be argued at this time is, that a policy focused primarily on the demand side, will somehow yield to supply side economic measures. In other words, the focus will gradually be set on wider range of economic determinants, like domestic economic activity, international trade competitiveness as well on economic policy coordination, focusing both on the demand as well as on the supply side. Therefore, the future policy focus ought to be both on the needs and requirements of the production sectors in order to prevent shortages in the supply of goods and services.

EXPECTATIONS

The above-described environment speaks of a high level of uncertainty. The combination of monetary finetuning with a flexible supply management will require coordination both domestically as well as internationally, i.e., among the free economic countries.

EFFECTS ON INVESTMENT POLICY

Our scenario might be viewed as intricate and difficult to be implemented, especially over the short-to-medium-term horizon.

However, assuming that the domestic activity might stand to profit most, this would imply a specific focus on the domestic market, also taking into account the possible currency swings, and most importantly also technological change, induced by an increasing focus on domestic independence.

While the impact of the policy change will primarily determine the medium-to-long term outlook, we deem it necessary in order to prevent a collapse in the rate of economic growth, which we forecast as mostly driven by domestic activities. The outlook will also continue to be impacted by the outcome of Russia`s war against Ukraine.

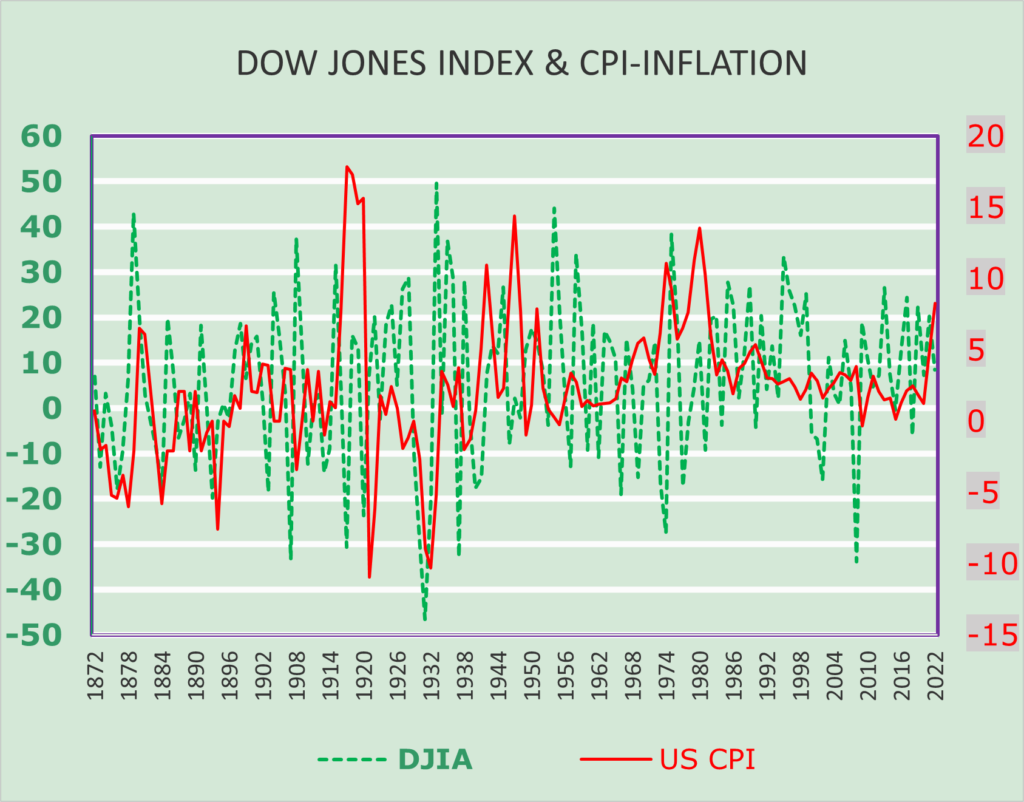

What can be inferred from the following chart of the Dow Jones Index, based on publicly available data?

Does the chart say anything about the appropriate environment for equity commitments?

Is the current rather pessimistic assessment something new and therefore pointing to a somewhat unique constellation, or

Are there historical periods that can help explain the current state of the economy?

The graph indicates that the DJIA’s performance has been quite poor in both years of inflation and deflation, while in years of relative price stability the DJIA has performed quite well. However, the implied data do not take into account the loss of purchasing power, which could result in a higher positive or negative compound return for the respective investment.

The annual inflation rate, as pointed out in the above chart, is revealing, is it not? Looking at the long-term graphical trend of annual inflation rates from 1983 onward, there is a sharp contrast to the long-term story. However, media attention is mainly focused on recent developments and the prolonged period of relative stability (since the early 1980s), pointing to “declining and rather stable” inflation rates! Recall that previous highs occurred in 1812, during the Mexican War of 1846-48, during the Civil War of 1861-1865, World War I of 1914-1918 and World War II of 1939-1945, as well as the subsequent Korean War of 1950-1953 and the Vietnam War of 1955-1975. Subsequent political and economic turmoil did not lead to similar increases in inflation rates. Economic turmoil did not lead to similar increases in inflation rates.

SOURCES OF INFLATION

In economics, the main causes of inflation are grouped into three specific categories:

Cost push,

Demand push and

Inflation expectations.

Widespread skepticism, not only of analysts, speaks of a likely, economic “hard landing”. These expectations can primarily be explained by foretold interest rate hikes by the monetary authorities. The immediate result is a further increase in uncertainty. At this point, let us take a closer look at what are the real sources of the feared rise in inflation. For this purpose, we rely on the following chart.

Rising prices of domestic and/or imported goods, as seen recently, have driven up consumer goods and production costs. These developments are reflected in rising consumer and producer price indexes in Switzerland and the United States, as shown in the following graph.

Normally, the main causes of inflation are classified as in the diagram above. As pointed out in previous EMRs, we believe that in the current economic phase the main inflationary cause lies in the cost of commodities as a result of the significant reduction in supplies, for example, of crude oil and raw materials. All economies have been affected by declining supplies of many industrial and consumer goods. One concrete indication has been and continues to be the increase in crude oil prices due to Russia’s war against Ukraine and the need and obligation to reduce dependence on imports from hostile countries such as China and Russia. Another contributing factor is the wrong decision to relocate production to producers with lower production prices, such as chip production in the Far East.

DEMAND PULL

Rising prices of domestic and/or imported goods, as seen recently, have driven up the costs of consumer and production goods. These developments are reflected in the rise of consumer and producer price indexes e.g., in Switzerland and the United States, as shown in the graph below.

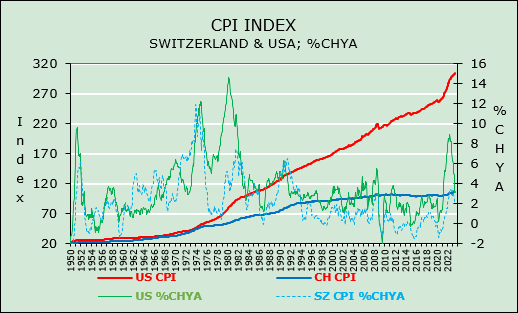

Considering the evolution of consumer price indexes in the United States and Switzerland since 1980, the following emerges:

The implied growth rates of the indices presented show significant growth disparities. Between January 1950 and June 2023, the U.S. CPI increased by 1’190%, while the Swiss CPI increased by only 100.9%. A truly remarkable discrepancy!

The trend in annual rates of change (on a monthly basis) shows a rather surprising development. The differences in the rates of change are really surprising. For example, the Swiss CPI peaked at 11.57% in January 1974, while the U.S. CPI reached 14.59% in March 1980.

Recent inflation hikes have not been as pronounced. In June 2022, the U.S. CPI peaked at 8.93 percent, while the corresponding peak of the Swiss CPI was measured at 3.45 percent in August 2022.

These developments suggest that the real problem is not inflation itself, but rather its determinants.

EXPECTATION ON COST-PUSH INFLATION

An increase in the price of domestic and/or foreign inputs (such as crude oil or raw and basic materials) leads to an increase in domestic production costs. Firms that face higher costs to produce each unit of output tend to produce less and/or raise the prices of their goods and services. This can have cascading effects on the prices of other goods and services. For example, an increase in the price of oil, which is an important factor of production in many sectors of the economy, initially leads to an increase in the price of gasoline. Higher gasoline prices in turn make it more expensive to transport goods from one place to another, which in turn leads to higher prices for products such as food.

Cost-driven inflation can also occur as a result of supply disruptions in some sectors, such as due to unusual weather conditions or natural disasters. Large hurricanes and floods regularly occur, damaging large quantities of agricultural products and causing significant increases in food prices, which temporarily leads to higher inflation.

IMPORTED INFLATION AND THE EXCHANGE RATE

Exchange rate fluctuations can also affect prices. A depreciation of the do-mestic currency increases inflation in two ways. First, the prices of goods and services produced abroad rise relative to those produced domestically. As a result, consumers have to pay more to purchase the same imported products, and firms that rely on imported materials in their production pro-cesses pay more to purchase these inputs. Price increases in imported goods and services contribute directly to inflation through the cost-push channel.

Second, a depreciation of the currency stimulates aggregate demand. This happens because exports become relatively cheaper for foreigners, leading to an increase in demand for exports and higher aggregate demand. At the same time, domestic consumers and businesses reduce their consumption of relatively expensive imports and shift their purchases to domestically produced goods and services, which in turn leads to an increase in aggre-gate demand. This increase in aggregate demand puts pressure on domes-tic production capacity and increases the scope for domestic firms to raise their prices. These price increases indirectly contribute to inflation via the demand-pull channel.

In terms of imported Inflation, the exchange rate has a greater influence on inflation through the respective effects on prices of goods and services that are exported and/or imported (so-called tradable goods and services), while the prices of non-tradable goods and services depend more on do-mestic development.

IMPLICATIONS FOR INVESTMENT POLICY

The context outlined portends a rather difficult environment. Investing requires careful attention and consistent examination of the determinants of one’s investment position. This concerns both trading dynamics and long-term needs and requirements. It is no longer sufficient to focus on the monetary policy actions of central banks, both in terms of managing the money supply and fine-tuning interest rates. What is required is a specific knowledge of causes of inflation be they demand-pull, cost-push, or due to inflation expectations—or due to domestic and/or foreign policy constraints. A concrete assessment of the near future remains a cause of great concern.

The main arguments of our deterministic view lie in the need for repatriation of most vital production goods due to energy policy constraints as well as the production of critical metals—in particular to reduce supply bottlenecks for oil and natural gas. In this context, strong exchange rate fluctuations are to be expected, which could limit international diversification. In addition, there are fears about possible sanctions, which are difficult to assess. For these reasons, we are placing our investment, as far as possible, in the domestic market. Should the USD continue to depreciate against the CHF we would see it as another serious concern.

Nevertheless, our expectations remain cautiously positive, because overall demand is likely to increase due to rising spending by consumers, companies and even the government.

An important determinant is and remains the development of foreign trade.

Industrial transformation, i.e., the change in the growth pattern of the last 20 to 30 years, is once again taking place at a rapid pace. Well, our search for evidence on the position of the global economy, and by extension the financial markets, led us to the Inflation Reduction Act of 2022 (IRA), passed by the U.S. Congress and signed into law by President Biden on August 16, 2022. Astonishingly enough, it goes almost unnoticed in the media. Now, one may ask what the scope of this act may be? Well, it is a law primarily aimed at curbing inflation by reducing the deficit and investing in domestic energy production while promoting clean energy. Among other things, the enacted legislation is expected to raise $738 billion and authorize $391 billion in energy and climate change spending and $238 billion in deficit reduction. Although the expected impact on inflation is somewhat controversial, it still indicates some economic progress. Indeed, the goal is to make substantial public investments in social, infrastructure and environmental programs throughout the country.

From this ambitious program, one can infer the implicit intention to promote domestic economic activity. In other words, this legislative text favors domestic investment, which in due course will also mean a reduction in certain imports. Certainly, it will take some time for this to become apparent in practice, but it nevertheless requires careful and continuous analysis of foreign trade.

The said act implies “regulation” with the specific aim of balancing/protecting the local competitiveness of the national market from the oligopolistic aggressiveness of mainly multinational technology corporations and especially nations like China. The “act” presupposes an initial reaction by the governments of democratic states and thus a clear response to the Russian invasion of Ukraine. At this juncture, it is worth mentioning that the EU faces similar difficulties as the US, namely rising import prices. A key difference between the U.S. and Europe, especially the EU, is the lack of “decision-making power,” which is still based on the authority of the respective national authorities. In addition, it should not be forgotten that the EU also decided to suspend state aid regulation with the Temporary State Aid Framework of March 2022. Strangely enough, the focus was mainly on Germany.

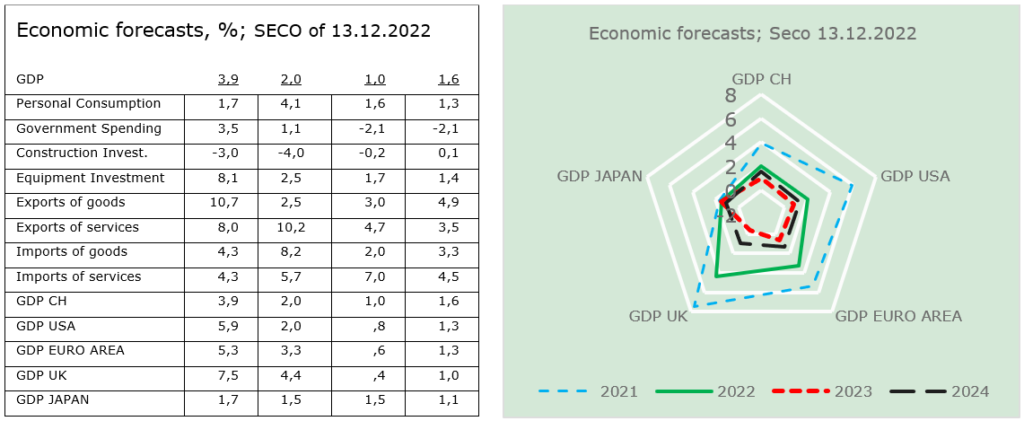

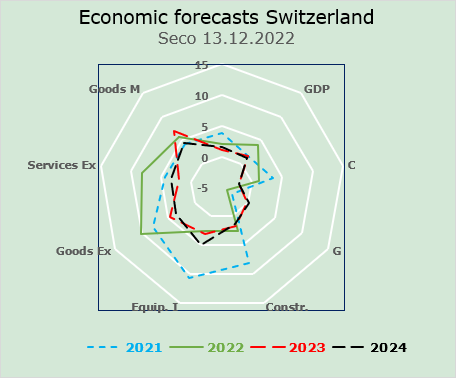

In the table and graph we show e.g., the SECO’s (State Secretariat for Economic Affairs) outlook in order to illustrate the specific interrelationships.

CONSEQUENCES

The annual data and forecasts tell us that the U.K. and U.S. real GDP growth rates were the highest in 2021 and 2022, while the other countries’ data were significantly more modest. The Brexit decision is somewhat visible in the UK GDP data. The Covid-19 years and recent actions on interest rates by central banks to reduce inflationary pressures are visible in the GDP data of the countries shown.

Recent weeks have witnessed a certain revival of optimism, albeit accompanied by understandable caution, especially in financial circles. This seems to be supported by an increasing number of macroeconomic signals, as evidenced by the recent “modest” increase in the benchmark interest rate by just 0.25 percent, which is a clear sign of the approaching end of the rate hike cycle.

The risk of recession is slightly decreasing, mainly due to the explicit willingness to give extensive support to fixed investment by local enterprises. In the context, there is talk of “repatriation” of production of technological goods, to reduce dependence on imports, from the Far East. The Seco data are really telling. We are often told that the rise in the consumer price index must be controlled by raising interest rates. The U.S. Federal Reserve took the lead and raised interest rates significantly. Other industrialized countries have followed suit. At this point, we would like to point out the potential impact of rising prices on asset allocation.

Nominal interest rate increases—such as those recently induced by central bank measures—argue in favor of exposure to fixed-income securities. This, due to the fact that increases in interest rates usually open up opportunities to earning money on fixed-income securities. However, there is also the risk of loss in times of rising inflation. It is necessary to check whether future real interest income is higher than the cost of inflation. If this is not the case, the risk of loss would have to be assessed. At this stage, we continue to favor investing in equities. Particular attention needs to be paid to various sectors such as technology and chemicals, with volatility to be closely monitored.

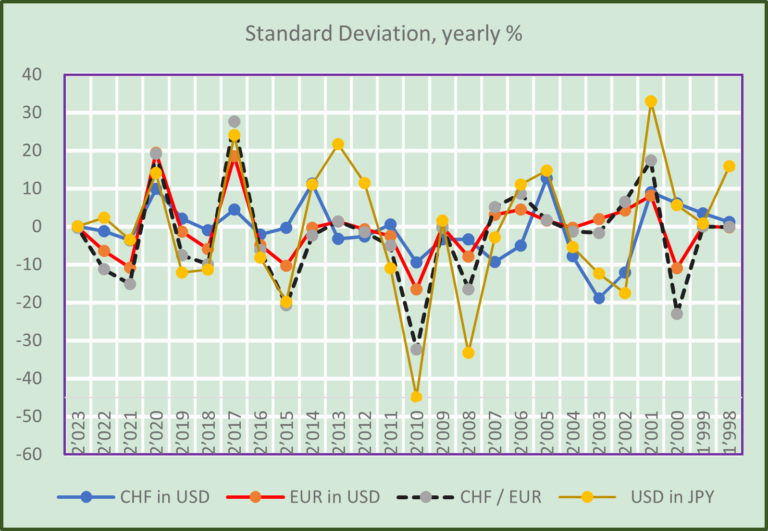

The fact is that the financial markets play an important role in the fluctuations of business cycles. Given that the current tightening policy could continue for some time, we think it is quite difficult to predict exactly which sector of the economy should be overexposed or underexposed and in which time frame. However, we consider the Russian invasion and war on Ukraine to be the most specific determinant of a worthwhile asset allocation. Geopolitical tensions aside, the impact on international trade and thus consumption and investment will need to be carefully monitored. In terms of international diversification, one should seriously consider the possible divergencies (STDEV) of the leading currencies in the following chart.

FOCUS ON SWITZERLAND

The Seco data on the primary sectors of the Swiss economy—see following chart—are telling indeed. Often, we are told, that the increase in the Consumer Price Index must be controlled via higher interest rates. The Federal Reserve Board has taken the lead in strongly pushing interest rates up. Other industrialized countries followed in a similar manner. Here, we would like to point to some other factors responsible for the increases in prices.

CONSEQUENCES

Undoubtedly, the Russian invasion of Ukraine will force the economies of the free world to reduce their dependence on autocratic, pro-communist countries as quickly as possible. This is bound to entail a return to local production of many goods and services and an orientation toward other producers of oil, gas, etc. First signs of this change are visible in the U.S. technology industry. See: Chips Act , in which special attention is given to short-term inflationary pressures and thus to the specific responses of central banks.

In Europe, too, there are proposals that go in the same direction, although there are still differences from country to country. There is no doubt that the invasion of Ukraine is a sign of an increasingly inevitable “de-globalization.”

Geopolitical tensions aside, the impact on international trade, and thus on consumption and investment, needs to be carefully monitored. The dreaded volatility of energy and gas prices will remain a source of confusion, both in terms of economic growth as a function of inflation, and in terms of the ups and downs of international trade, which currently speaks of continued volatility, and not just in the financial markets.

There is a further serious difficulty: the increasing and high indebtedness of countries, companies and the general public. Fortunately, the current situation does not resemble that of the late 1970s, when Paul Volcker, chairman of the FED, was forced to intervene aggressively to fight inflation.

In terms of international diversification, one should seriously consider the possible developments of the leading currencies.

OUTLOOK 2023

The above-outlined environment clearly indicates a dramatic change in the environment. Until recently, the focus was on fighting inflation; now the focus is much more on “repatriating” production. This is evident, for example, in the stimulus proposals [Inflation reduction ACT (IRA), Chips and Science Act, and Bipartisan Infrastructure Law]. Thus, the focus is clearly on renewable energy, semiconductors, and infrastructure, i.e., promoting local economic growth while reducing dependence on foreign manufacturers.

In both the United States and Europe, economic policy is no longer primarily focused on fighting inflation, but rather on rapidly renewing the domestic manufacturing sector to reduce dependence on imports from foreign manufacturers. This, if implemented coherently, would lead to a significant increase in local employment and economic activity. The specific objective is, among other things, to reduce dependence on China.

At this stage, our forecasts can be considered somewhat more optimistic than those currently circulating in the press. To some extent, our assessment is confirmed by a contradictory political attitude that is no longer so much determined by “cheaper producers” as much as by the “free market” or, at best, by an egalitarian mixture of both approaches.

FINDINGS FOR INVESTORS

Assuming that investment growth will replace government spending as the main determinant of future economic activity, one needs to look beyond infla-tion expectations and trends to define a successful investment approach. Therefore, we argue as follows:

The era of runaway inflation is almost over; more attention needs to be paid to price stability.

If the assumption is correct that inflation will not rise as strongly as it has recently, fixed-income investments should become somewhat more attrac-tive, at least in the short to medium term.

A reduction in dependence on autocratic countries, combined with a not in-significant increase in domestic production, would stimulate optimism in fi-nancial markets.

We continue to believe that the CHF remains promising, as does the USD.

With its invasion of Ukraine, Putin’s Russia has challenged the balance that persisted since the end of the Cold War. Recently, the world has entered a very mixed phase of transition. We believe that this situation will persist in having a significant impact on consumption, investments, international trade, and currencies. This situation is expected to require a continuous updating of the investment policy.

The fact is that, in 2022, both the USD and CHF were among the few asset classes that tended to be spared from the Covid 19 pandemic and Russia’s war against an independent country. Rising inflation has been a worrisome side effect, mainly monitored by the Federal Reserve. At present, the focus is increasingly set on the whereabouts of economic activity. A growing number of analysts fear an imminent recessionary phase, including continued currency adjustments, as a consequence of the differentiated monetary policies.

CONSEQUENCES

Undoubtedly, the Russian invasion of Ukraine will force the economies of the free world to reduce their dependence on autocratic, pro-communist countries as quickly as possible. This is bound to entail, for example, a return to local production of many goods and services and an orientation toward other producers of oil, gas, etc.

First signs of this change are visible in the U.S. technology industry. See:: Chips Act [1], in which special attention is given to short-term inflationary pressures and thus to the specific responses of central banks. In Europe, too, there are proposals that go in the same direction, although there are still differences from country to country. There is no doubt that the invasion of Ukraine is a sign of an increasingly inevitable “de-globalization.”

Geopolitical tensions aside, the impact on international trade, and thus on consumption and investment, needs to be carefully monitored. The dreaded volatility of energy and gas prices will remain a source of confusion, both in terms of economic growth as a function of inflation, and in terms of the ups and downs of international trade, which currently speaks of continued volatility, and not just in the financial markets.

There is another serious difficulty: the increasing and high indebtedness of countries, companies and the general public. Fortunately, the current situation does not resemble that of the late 1970s, when Paul Volcker, chairman of the FED, was forced to intervene aggressively to fight inflation.

In terms of international diversification, one should seriously consider the possible developments of the leading currencies. See the graph below.

At this point, we wonder what can be inferred from the graph concerning the average, annual changes in monthly exchange rate fluctuations. We note that the differences in performance are indeed significant, as they could continue to determine the respective ups and downs as well as volatility.

OUTLOOK 2023

The environment outlined above clearly indicates a dramatic change in the environment. Until recently, the focus was on fighting inflation; now the focus is much more on “repatriating” production. This is evident, for example, in the stimulus proposals (Inflation reduction ACT [IRA], Chips and Science Act, and Bipartisan Infrastructure Law). Thus, the focus is clearly on renewable energy, semiconductors, and infrastructure, i.e., promoting local economic growth while reducing dependence on foreign manufacturers.

In both the United States and Europe, economic policy is no longer primarily focused on fighting inflation, but rather on rapidly renewing the domestic manufacturing sector to reduce dependence on imports from foreign manufacturers. This, if implemented coherently, would lead to a significant increase in local employment and economic activity. The specific objective is, among other things, to reduce dependence on China.

At this stage, our forecasts can be considered somewhat more optimistic than those currently circulating in the press. To some extent, our assessment is confirmed by a contradictory political attitude that is no longer so much determined by “cheaper producers” as by “administrators” or simply by the “free market” or, at best, by an egalitarian mixture of both approaches.

FINDINGS FOR INVESTORS

Assuming that investment growth will replace government spending as the main determinant of future economic activity, one needs to look beyond inflation ex-pectations and trends to define a successful investment approach. Therefore, we argue as follows:

The era of runaway inflation is almost over; more price stability needs to be considered.

If our assumption that inflation will no longer rise so sharply is correct, fixed-income investments could retain some attractiveness, at least in the short to medium term.

Looking at the equity allocation as a result of the first paragraph of the of the “Consequences”, comment above, the focus on technology stocks, undoubt-edly looks more promising than any other sector.

We continue to think the CHF is promising, as well as the USD.

Comments are welcome.

[1] In July 2022, Congress passed the CHIPS Act of 2022 to strengthen domestic semiconductor manufacturing, design and research, fortify the economy and national security, and reinforce America’s chip supply chains.

At the beginning of the new year, we may ask ourselves which of the following statements may be considered correct and thus a valid indicator of the most likely future developments:

Is significant inflation acceleration, plus 4% or more, a negative for the equity markets?

Is significant decrease, minus 2% or more, a positive for the equity markets?

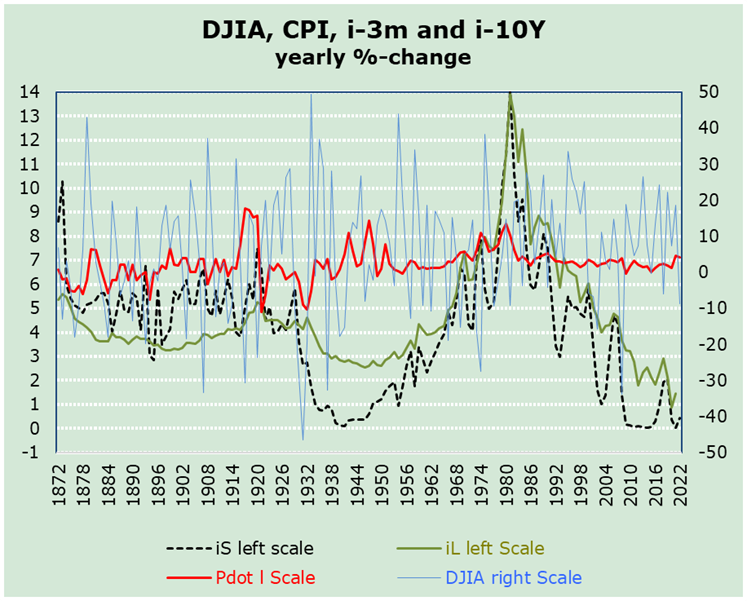

Bevor answering the two above posed questions let us portray the historic developments of the leading economy, the USA, as shown in the chart.

What does the historic representation of the yearly average changes of the DJIA and the yearly rate of change of the US Consumer Price Index tell us? Our interpretation of the graph shows several interesting things:

The analysis of the annual rate of change indicates that changes in the DJIA are much more volatile than for the consumer price index.

Both the development of the inflation rate and that of the DJIA, before 1945 and since 1945, differ considerably from those of the preceding period. This makes predicting future developments – for both indicators – somewhat more difficult than generally assumed.

The rather contained inflation rate swings since 1980 do not point to a significant growth in the equity index.

After a thorough analysis of the diagram, we come to the following conclusions:

First, we note that the actual annual changes in the inflation rate are less volatile than those in the DJIA index. This suggests, in our view, a deterministic distinction between the two categories under consideration. In other words, the respective trends are not primarily determined by the same factors for the DJIA and the CPI-Index.

So far into the current cycle, inflation has not (yet) risen as in the late 70’s nor in the previous cycle. The real question at this time is which of the two series used here will be the deterministic factor: the DJIA or the CPI? Any suggestions?

OUTLOOK 2023

Recalling the various expectations and taking into account the available hard facts as compared to the known developments in 2022 as a starting point, we firmly believe that the outlook for 2023 remains characterized by known and also imponderable features. The challenging question to answer at this time concerns, first of all, the hoped-for end of the disastrous Russian invasion of the Ukraine. This “hoped-for return to normalcy” would undoubtedly lead to lower crude oil and gas prices and, as a result, would also lead to a reduction in fears of persistently high inflation and would consequently encourage the inflow of much-needed technological inputs. The result would be a significant pickup in economic activity, instead of the recessionary outcome currently feared.

For Central Banks, this would imply a deterministic reduction in recession fears and the abandonment of restrictive monetary policy. This, in turn, would promote an economic recovery that should boost stock markets and, to some extent, fixed-income investment as well. High inflation rates historically have been associated with financial losses, as they have also been in the recent past. History teaches us also, that patience is a promising attitude, especially when the causes of inflation are due mainly to factors that are not so much monetary as economic or even worse political.

FINDINGS FOR INVESTORS

Assuming that the Russian invasion of the Ukraine is unsuccessful, it can be assumed that Russian oil and gas supplies will slowly increase, which should tend to reduce the inflation rate. This makes it unlikely that domestic banks will continue to push interest rates up, as they have done recently. In other words, the appeal of fixed-income securities may be limited to the next few months of 2023. However, we believe that the appeal of fixed income is likely to be limited to the coming quarters, limiting the appeal of equities in the first quarters of 2023.

Our assessment depends largely on the size and length of the expected economic slowdown, which, in turn ought to bring inflation down. The necessary and sufficient condition for this to happen, is that inflation begins to fall in line with the decline in energy costs. In any case, special attention should be paid to currency fluctuations when diversifying internationally. Highly indebted companies should be avoided. As Swiss investors, we continue to prefer the local market, at least until the end of the cyclical interest rate increase will manifest itself. In any case, in the international diversification process, special attention should be paid to currency fluctuations. Highly indebted companies should be avoided. As Swiss investors, we continue to prefer the local market, at least as long as the end of the interest rate cycle is in sight.

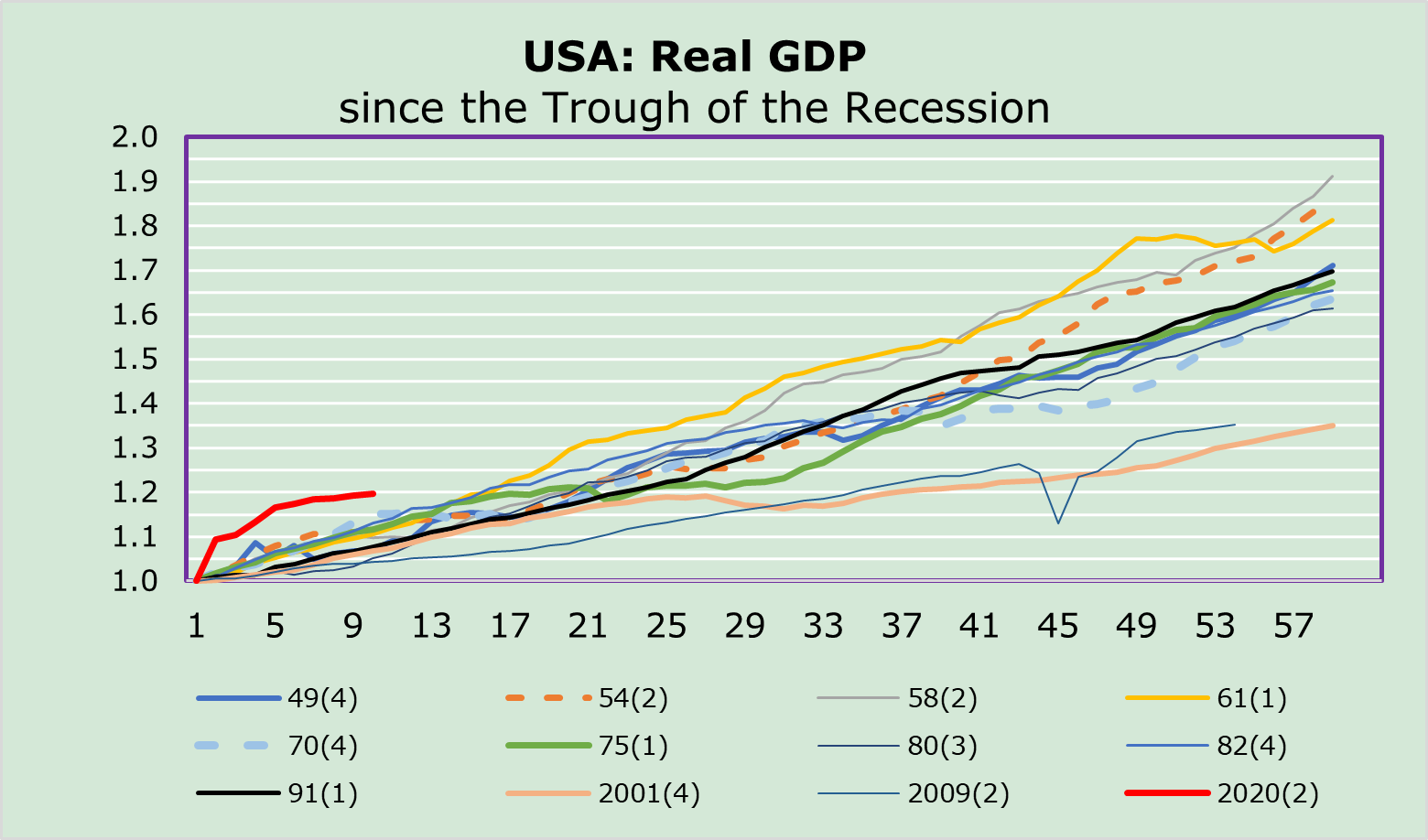

Forecasting is a demanding exercise. Depending on the data quality of the series one uses it is possible to asses a “promising” outlook. In this EMR, we focus on the development of real GDP in the U.S. – depending on the business cycle – compared to the developments of stock indices.

What does the US real GDP chart describe the past cyclical developments and what can we deduce for the near future?

The recent cycle does not confirm the widespread pessimism. Actually, so far into the new cycle real economic activity has been sustained and has been surpassed only by the 1949/Q4 recovery.

Examining the longer-term cyclical developments, one finds that the divergence increases from cycle to cycle.

Are we facing a short-term correction of 2020/Q4 to 2011/Q2 or even a longer-term correction i.e., recessionary phase?

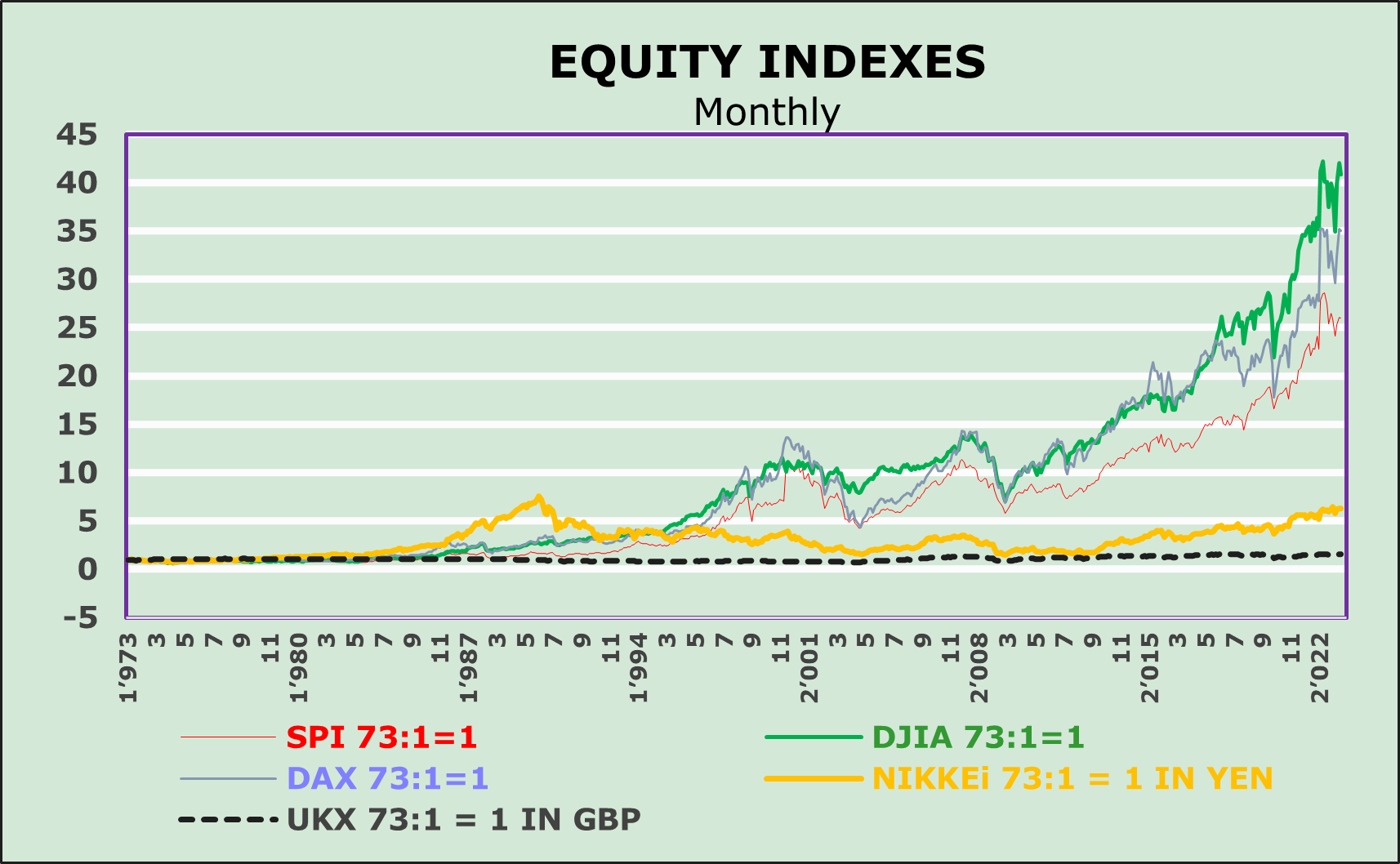

Given our interest in financial investments let us now analyze the developments of selected equity market indices since 1973.

What can be inferred form the chart?

What does the graph of stock indexes imply about their respective changes, both on an “index-by-index” basis and in cyclical comparison? What dependencies can be inferred regarding a promising investment policy?

The graph demonstrates, especially in the long run, a significant deviation between one stock index to another.

The trends of the DJIA, the Dax and the SMI indexes, while moving mostly in the same direction, add up to a significant performance differential, specifically since the early 1990s.

The performance of the UKX and NKY indexes is really amazing, aren’t they?

Contextually, it is really worth asking what the role of currencies has been, both in the long and short run, and also in relation to sectoral economic changes.

At this point in time, it is also worthwhile to examine the developments of 10-Y government bond yields, as shown in the following chart.

Our analysis tells us that a sizeable number of analysts have omitted to take into serious consideration the interplay between supply-side and demand-side determinants of the economy, the rate of inflation as well as of the financial markets.

Central banks on their part acted and reacted mainly to demand-side determinants. During the pandemic, debt-financed funds were “generously distributed.” This expansionary policy led, as expected, to higher demand, which, combined with rising energy prices, led to dramatic energy supply shortages. Consequently, prices of intermediate goods began rising as well. The “unexpected” result has been an increase in consumer prices, which in due turn pushed wage-demand higher. The world economy found herself in the midst of a vicious cycle. In response, central banks began to push interest rates higher at an unprecedented pace. Analysts and a sizeable number of market participants reacted with portfolio-adjustments, resulting in a sizeable equity market sell-off. Given that economic data are lagging indicators, they focused on selling stocks while switching to fixed-income securities.

OUTLOOK 2023

Recalling the errors incurred in 2022 we ought not to forget that the prospects for 2023 remain characterized by well-known imponderables. The difficult question to be answered at this juncture clearly concerns the end of the disastrous Russian invasion of the Ukraine. This “hoped-for” return to normalcy would undoubtedly lead to lower crude oil and gas prices, and in due time, reduce also fears of persistently high inflation – and stimulate the flow of much-needed technological inputs. The result would be a resumption of economic activity.

For Central Banks, this would involve deterministically reducing recession fears and abandoning restrictive monetary policy. This, in turn, would promote an economic recovery that should revive stock markets.

Historically, high inflation rates have been known to cause stock losses, as it was the case in 2022. However, history teaches us that patience is a promising attitude.

FINDINGS FOR INVESTORS

Assuming that the Russian invasion of the Ukraine will not be successful, it may be assumed that Russian oil and gas supplies will slowly increase, and that this should tend to reduce the inflation rate. This suggests that it is unlikely that national banks will have to continue to raise interest rates as sharply as they have done recently. In other words, the longer-term attractiveness of fixed-income securities is likely to diminish.

We believe that bond yields should tend to reduce the attractiveness of equities in the first two quarters of 2023. Our assumption remains largely dependent on the economic slowdown. The necessary and sufficient condition is that inflation begins to fall in line with the decline in energy costs.

Our current reading of the facts seems to suggest that the need for national banks to continue raising interest rates, as sizably as they did in the last half of 2022, is unlikely to persist much longer. In other words, the appeal of fixed income is likely to be limited to the next few months. We believe that bond yields could curb the appeal of equities in the first two quarters of 2023. Our assumption in this regard is largely driven by the economic slowdown, which will lower inflation in due course. In particular, the necessary and sufficient condition for the inflation rate to start falling will be a reduction in energy costs. In any case, special attention should be paid to currency fluctuations in international diversification. Highly indebted companies should be avoided.

As Swiss investors, we continue to prefer the local market, at least as long as the end of the interest rate cycle is in sight.

Both the Covid-19 pandemic and Putin’s war against Ukraine are increasingly determining economic analysis, both in the short and long term. Also going almost unnoticed by the public debate are the consequences of “digital nomadism” and, in particular, the tax consequences of the migration of highly qualified professionals who take advantage of the opportunity to work at a computer in places where taxes are low.

DEMAND VS. SUPPLY ANALYSIS

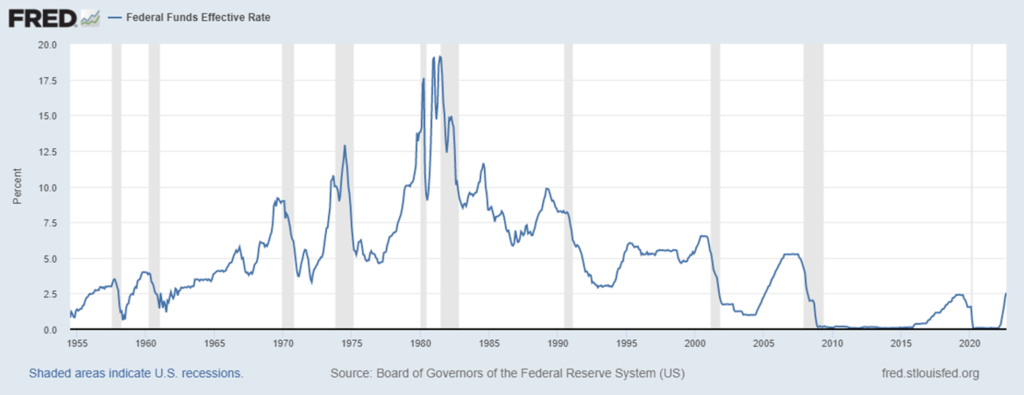

As a result of both the Covid 19 pandemic and the war against Ukraine, two specific and deterministic aspects can be found regarding the short- to medium-term economic outlook. Monetary authorities have emphasized a policy of “extraordinary” monetary tightening to combat inflation, i.e., unprecedented increases in interest rates, as evidenced by the recent trend in the federal funds rate relative to developments since 1955. See table and chart.

FOMC Meeting Date

Rate of Change (bps)

Federal Funds Rate

Sept 21, 2022

+ 75

3.00% – 3.25%

July 27, 2022

+ 75

2.25% – 2.50%

June 16, 2022

+ 75

1.50% – 1.75%

May 5, 2022

+ 50

0.75% – 1.00%

March 17, 2022

+ 25

0.25% – 0.50%

Indeed, it is instructive to elicit the logic behind policy responses. As far as policy adjustments are concerned, we face a real dilemma. Are the actions and reactions in curbing inflationary conditions more supply or more demand-driven?

By even superficially reading newspapers, listening to the radio or watching television, we find that the focus is on “demand.” Why is that? Well, Central banks are pushing interest rates sharply up to contain rising inflation. Thus, when interest rates are raised quickly and sharply, one must assume that the goal of containing rising inflation is to reduce demand, especially of business investment (i.e., fixed investment, construction activity, and net exports). At this point, it is worth recalling that the recent rise in prices in all major economies is not primarily due to an increase in demand, but to a sharp reduction in the supply of essential economic goods. More specifically, prices are being driven up by “policy-induced” cuts in crude oil and gas exports, primarily by Russia. Recently, there has also been a significant decline in imports of engineering components from China. It is a fact that the countermeasures taken by the EU and the U.S. should also be taken seriously.

We are currently facing a new phase in the economic cycle. The positive trends of the period prior to the advent of the Covid-19 pandemic and the invasion of Ukraine have turned into a restrictive phase, particularly in the area of procurement of vital goods and production components. In our view, this emerging change requires a radical rethinking of the economic behavior. This should entail a rethinking of the interdependencies between the economy, finance and monetary policy. In other words, it is not about inflation per se, as much as on rapidly improving the supply of key intermediate goods and products.

However, if we assume that policy should focus on supply-side rather than demand-side constraints, as has been the case recently, then we can assume a dramatic policy-driven shift away from rising interest rates toward improving domestic supply, with more emphasis on the local investment sector. What we can envision is a shift back in the production of intermediate goods and change in energy supply. This readaptation would require a shift away from “cheaper” imports to increasing domestic production. The focus should (and will) be on improvements for the local investment sector to the detriment of imports.

FINDINGS FOR INVESTORS

A closer look at the current environment shows that the focus is on raising interest rates to coun-ter inflationary pressures. The actual determinants of current inflation are almost ignored. As-suming that the rise in inflation is mainly due to factors (such as Covid-19 and especially the in-vasion of Ukraine and China’s threat to invade Taiwan), the rise in crude oil, gas and food prices would increase dramatically beyond the normal supply and demand trends. Therefore, the focus should rather be on how to solve the bottlenecks in the supply.

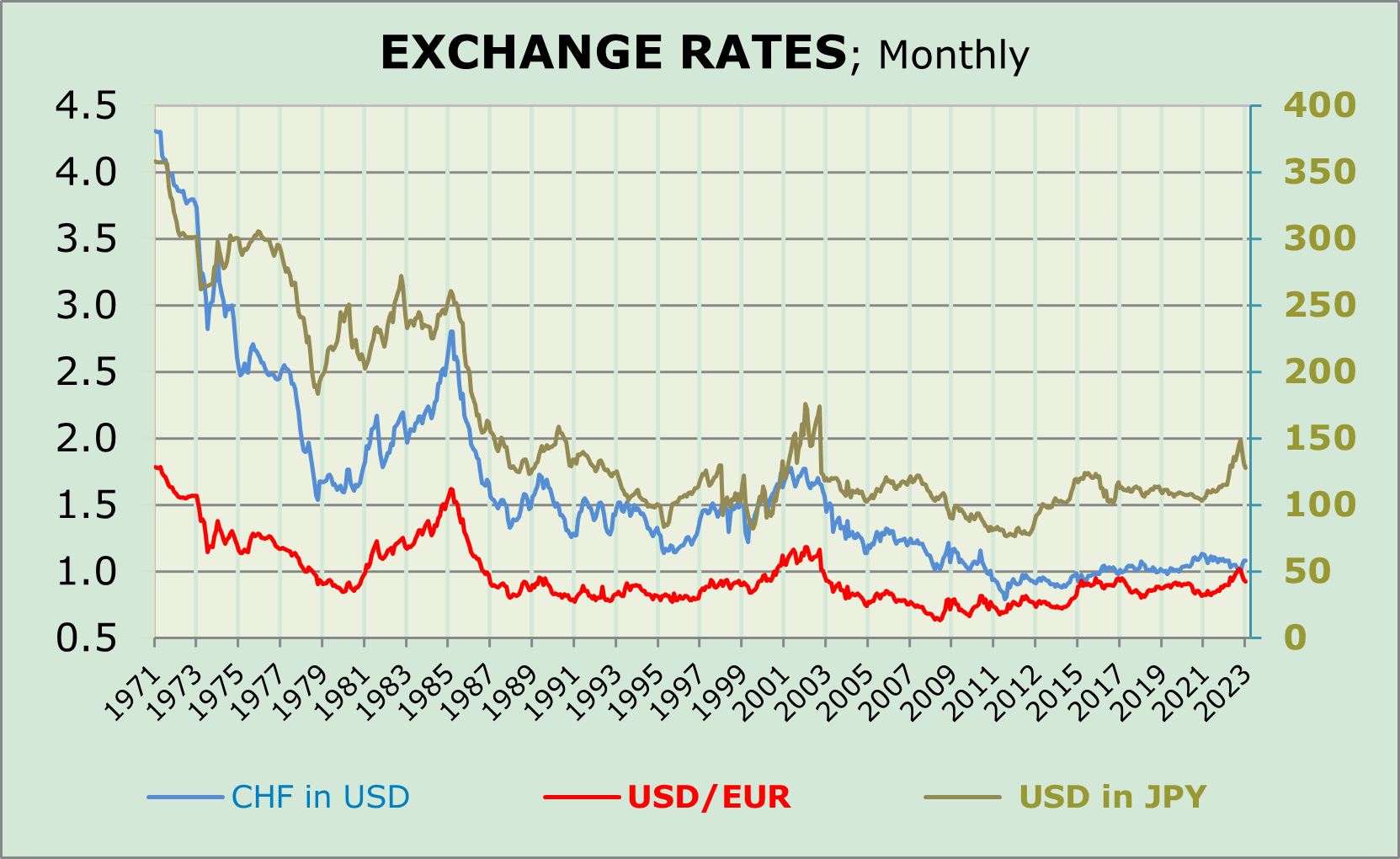

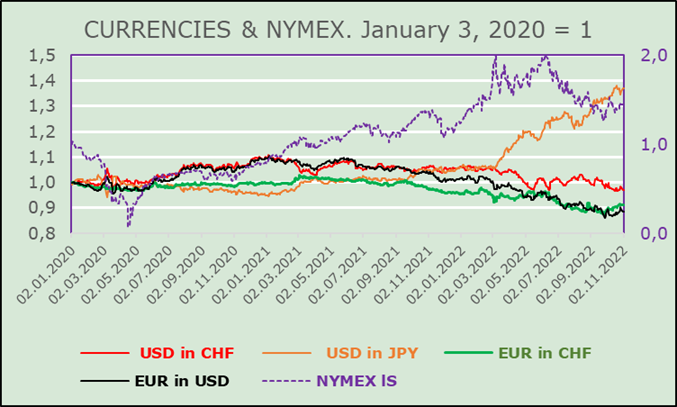

In October 2022, there were increasing calls from international institutions to slow the pace of monetary tightening because of the unexpected impact on exchange rates, as shown in the charts on currency and NYMEX.

It should be considered that the U.S. dollar increasingly tends to mimic crude oil and gas price trends. These similarities portend an imminent reversal in the fight against inflation. Thus, one may wonder whether the phase of interest rate hikes by central banks is coming to an end. Re-markably, so far, calls for moderation of the pace of monetary policy have not increased. An im-portant reason for a probable reversal of interest rates is given by the voices of international in-stitutions, speaking of an impending recessionary phase.

In the current economic policy environment, it is tricky to draw conclusions about a promising asset allocation. We believe that the Swiss investor should continue to focus primarily on the do-mestic currency market (and also the US dollar), as a positive development can be expected here. Secondly, we believe that it is premature to invest in money markets and/or fixed income instruments, at least as long as the high interest rate phase persists. Thirdly, it is necessary to quantify, as precisely as possible, the depth and duration of the much-touted recessionary phase. For our clients in particular, it seems advisable and necessary to assess the impact on the real estate market. An undoubtedly arduous task not only for the experts at Swisschange.

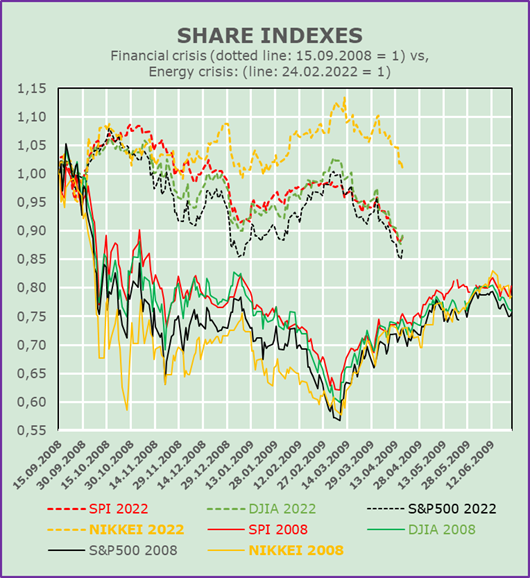

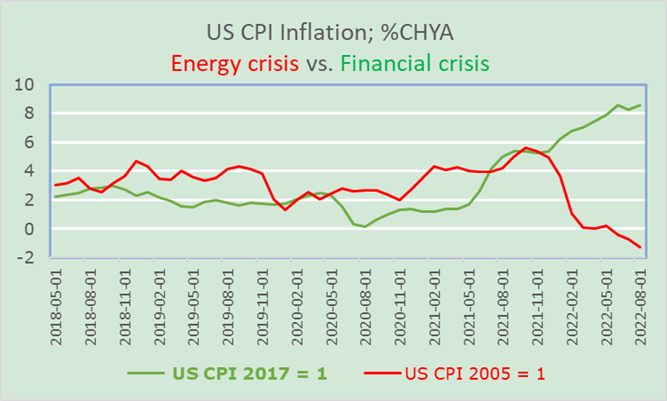

Increasingly we read and hear analysts and market participants asking the following question about the markets whereabouts: Is the 2022 energy crisis comparable to – or even more insidious than – the 2008 financial crisis?

In this context, we would like to ask the reader to closely analyze the following chart of selected stock indices. To simplify the comparison of the two periods, we have normalized the stock indices to 1 at the beginning of the respective period and superimposed them. The first period begins on 15 September 2008, the collapse of the investment bank “Lehman Brothers”, the second period on 24 February 2022, the invasion of Ukraine by the Russians.

FINANCIAL VS. ENERGY CRISIS

How did and do the stock indices react to the two states of disorder mentioned above? What does the chart suggest?

IMPLICATIONS FROM THE CHARTS

A first, summary assessment, points to differential trend movements from a one equity index to another. As each crisis perdures they become significantly less marked for the energy crisis than for the financial crisis.

A second assessment refers to the differential rates of growth, which, so far, have been significantly larger during the financial crisis than so far in the energy crisis.

A third assessment points to the shorter-term “trend reversals,” which imply a differentiated view of the actual determinants, be they inflation, interest rate policy or the ongoing war against Ukraine. In our view, these factors have determined the short-term trend much more than the longer-term one in both periods. Do they say anything about comparability? Yes, they do indeed, as we will highlight below.

Given today`s public focus on inflation, as the primary determinant, let us examine the inflation trend of the two periods, as shown in the chart on US CPI-Inflation. The chart has been comparable until July 2021, since, it has moved higher for the period of the ongoing energy crisis, while contracting in the period of the financial crisis! The real question at this crossing refers primarily to the differential interventions by the Central Banks: expansionary in the financial crisis and restrictive in the energy crisis. In addition, we should take into account that the financial crisis turned into a currency crisis as well as into a sovereign debt crisis. This setting made it easy to raise capital during the financial crisis, while making it difficult in the ensuing energy crisis.

INVESTORS` DILEMMAS

Trying to quantify the outlook based on forecasts of an impending recessionary phase, accompanied by rather persistent inflationary pressures and – for political reasons – higher interest rates, and the feared influence on financial markets and currencies, we lean toward a slightly less pessimistic assessment. There are certainly reasons why our optimism might be considered somewhat surprising and difficult to accept. Nevertheless, we believe that inflation might not be as easily reduced via higher borrowing costs. Inflation, in our assessment is determined significantly more by restrictions on the supply side than sustained demand. We would like to stress the importance of oil and gas prices as well as of food products as well as the dependence of technological components. They should fade as the Russian invasion of the Ukraine will be resolved.

In our opinion a sustained trend reversal of inflation can only take place with the end of the war against the Ukraine. This would imply a revival of international trade relations as well as an improvement in local economic activity. In addition, we expect an increasing repatriation of technological components in order to reduce – especially in Europe – the dependence on autocratic and undemocratic nations.

FINDINGS FOR INVESTORS

A closer look at the current environment reveals that the focus is on raising interest rates to counter inflationary pressures. The actual determinants of the current inflation are almost ignored. If we assume that the rise in inflation is mainly due to factors such as Covid-19, the invasion of Ukraine and China’s threat to invade Taiwan, dramatic pres-sure on the rise in crude oil, gas and food prices above and beyond normal supply and demand trends would be the consequence. So we should rather focus on how to solve the bottlenecks in the supply chains, while continuing to remain focused on the domestic market and currency.