EMR September 2023

Dear Reader

What has the “Buridan Donkey Paradox” to do with today`s economic assessments? Well, it stands for “when choosing not to choose becomes a bad choice”. It is a figure of speech referring to someone who, when faced with two equally valuable alternatives, does not make up his mind to choose one of them.

Examining the current investment setting, we are faced with an increasingly intricate and highly deterministic policy choice. Should we analyze the current outlook primarily from the demand side or the supply side? The public debate is undoubtedly preponderantly focused on the demand side. Even representatives of Central Banks overwhelmingly favor the demand-side approach. The sequence of interest rate hikes undertaken since mid-2022 speaks volumes, doesn`t it? The thorniest question to be answered, regarding the current “policy setting”, concerns expectations of an imminent adaptation, or possibly a reversal of monetary policy actions in order to avoid a feared economic recession?

On the supply side, the argument points to a growing need to explore new avenues of corporate finance. The requests are rather independent from the availability of liquidity or further monetary actions, while they increasingly point to new and growing needs of a changing economic environment.

So far, the outcome of this rather difficult assessment remains focused, preponderantly on a further reduction of the rate of inflation and, on the other hand, on hopes for an upswing in economic activity, which should result, in due course, also in further significant currency adjustments.

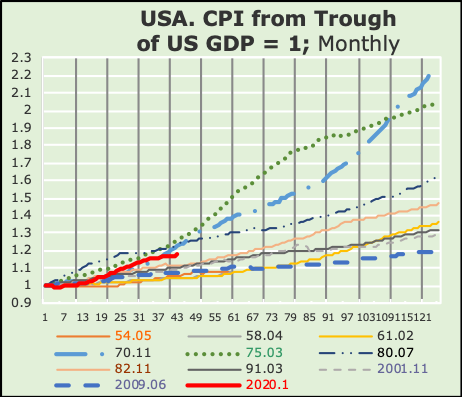

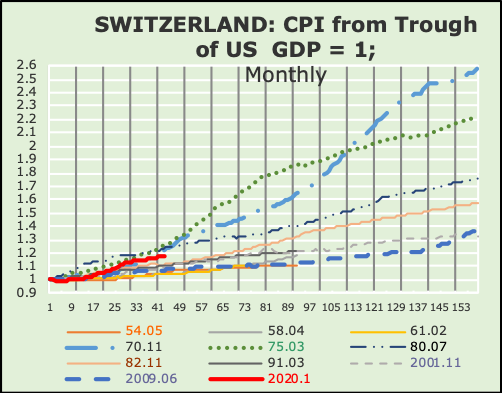

The dilemma can be implicitly derived from the chart of Swiss and U.S. inflation. The respective series are indexed to 1 for each specific cycle trough of US real GDP. The series portrayed in the chart show that, so far in the current cycle, inflation has fared better than for the cycles beginning in July 1980 as well as November 1970 and also March 1975.

CAUSES OF INFLATION

We cannot fully subscribe to the widely held view that the current economic setting ought to be primordially analyzed as a function of the “demand side” of the economy. Clearly, both consumer spending and business fixed investment as well as the respective balances of trade have required the known actions/reactions by the monetary authorities.

It is a known fact that both the Covid pandemic as well as the Russian war in the Ukraine have had, and continue to have a significant impact on the rate of inflation, economic activity as well as on currencies. We believe that these deterministic factors can hardly be managed solely by means of higher interest rates. In addition, the impact on international trade, as well as, the reorganization of economic transfer channels is hardly manageable by ever-higher interest rates.

We are not alone in assuming that inflation could persist regardless of monetary policy measures, and not only because of actions and reactions by Western economies. There are also increasingly explicit negative effects in the Chinese economy.

We assume that the monetary authorities ought not to be expected to remain prisoners of the metaphor of the Buridan Donkey. They will have to take the recessionary dangers into consideration. In other words, we would argue that, from now on, interest rate increases ought to be more moderate and coordinated with measures supporting a revival of economic activity. We assume that before long the focus will increasingly be on measures of revitalization of the domestic economic activity, while reducing the dependence on centralist states.

What can be argued at this time is, that a policy focused primarily on the demand side, will somehow yield to supply side economic measures. In other words, the focus will gradually be set on wider range of economic determinants, like domestic economic activity, international trade competitiveness as well on economic policy coordination, focusing both on the demand as well as on the supply side. Therefore, the future policy focus ought to be both on the needs and requirements of the production sectors in order to prevent shortages in the supply of goods and services.

EXPECTATIONS

The above-described environment speaks of a high level of uncertainty. The combination of monetary finetuning with a flexible supply management will require coordination both domestically as well as internationally, i.e., among the free economic countries.

EFFECTS ON INVESTMENT POLICY

Our scenario might be viewed as intricate and difficult to be implemented, especially over the short-to-medium-term horizon.

However, assuming that the domestic activity might stand to profit most, this would imply a specific focus on the domestic market, also taking into account the possible currency swings, and most importantly also technological change, induced by an increasing focus on domestic independence.

While the impact of the policy change will primarily determine the medium-to-long term outlook, we deem it necessary in order to prevent a collapse in the rate of economic growth, which we forecast as mostly driven by domestic activities. The outlook will also continue to be impacted by the outcome of Russia`s war against Ukraine.

Comments are welcome.