EMR July 2026

Dear Reader

It is a known fact that the solution of economic crises takes place in rather differential and hard to compare phases. Today’s specific difficulty for investors refers to the timing of any pertinent, policy actions/reactions.

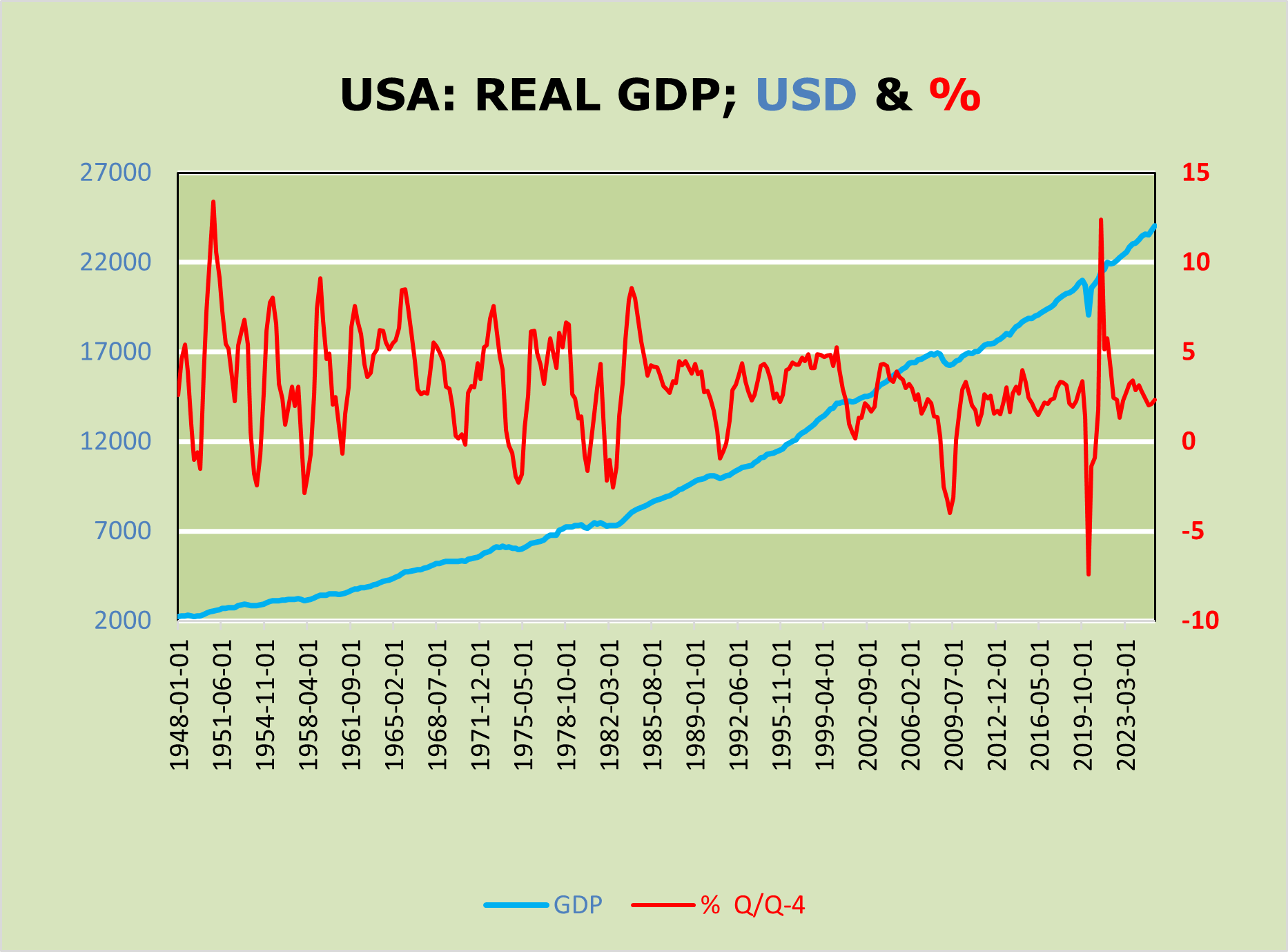

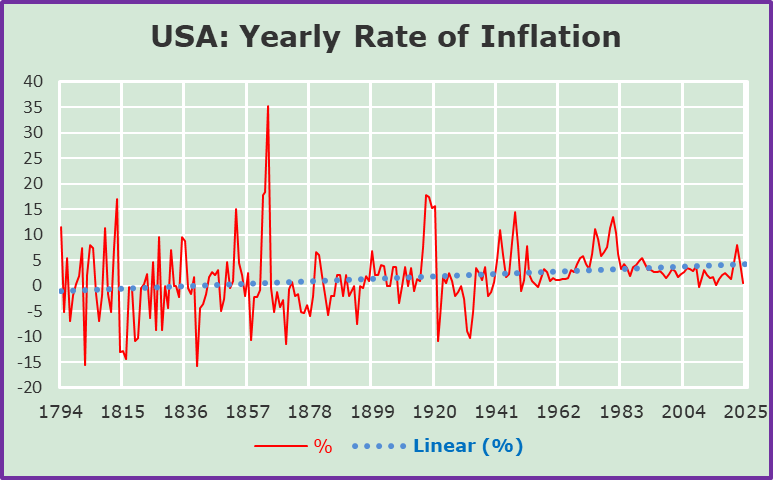

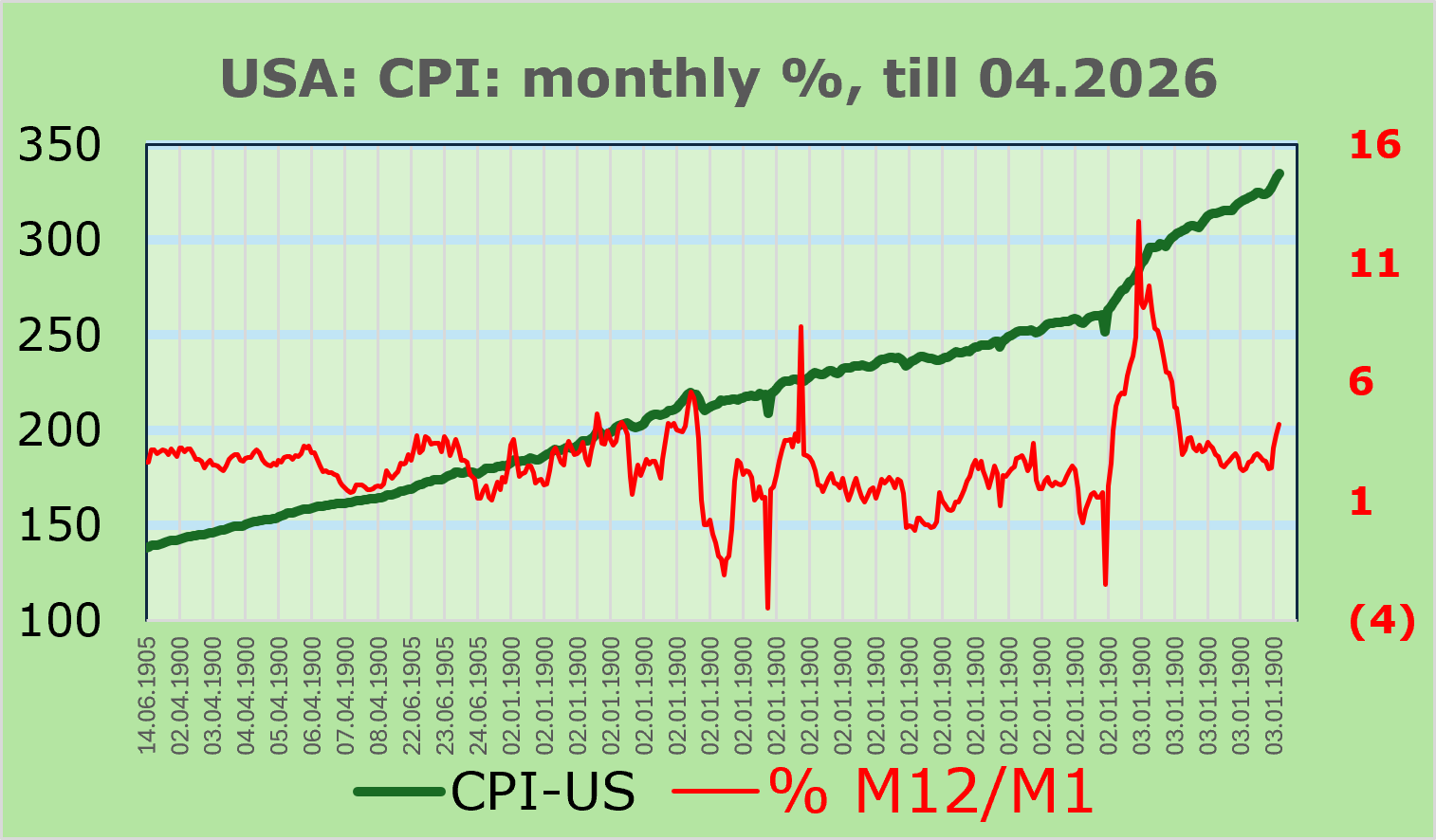

A pertinent example is shown by the long-term performance of the US rate of inflation, see following chart of the CPI Index (left scale), respectively the %-change on the right scale.

SURPRISING DEVELOPMENTS

Suddenly, in Mid-Year 2026, the political world seems to be on the way of a dramatic, unexpected improvement/change. The discussion is about the opening of the Strait of Hormuz, i.e. reopening of the waterway between the Persian Gulf and the Gulf of Homan. The strait is about 104 miles long with a width varying from about 24 to 60 miles. Knowingly, the Strait of Hormuz provides the only sea passage from the Persian Gulf to the open ocean and is one of world’s most strategic impasses.

Which are, at this crossing, the economic and political repercussions of this political U-turn, is the real question, is it not? Knowingly, it provides the only sea passage from the Persian Gulf to the open ocean and is one of the world’s most strategical passages.

From the economic point of view, if the announced project takes hold, it is supposed to alter the determinants of the economic assessment. While, as of recently, the focus has been on interventions of the monetary authorities by means of interest rate adaptations, the new setting concerns economic activity, primarily consumer spending and foreign trade developments. In other words, we argue that it might not be, interest rate management, as recently has been the case, to manage inflation, as much as real economic whereabouts. The ensuing chart of US CPI – inflation is revealing indeed.

As implicitly showed in the chart of the US CPI, the environment has recently been worrying, although more recently, we find it a bit less worrying. In addition, the short-to-medium-term outlook remains still rather difficult to quantify with a high degree of precision. Let us point out that the current US president’s policies remain rather tricky to assess with a high degree of precision.

A certain slightly more positive consensus seems to be back in the markets. At this intriguing crossing we believe that the focus will, or ought to be, on economic growth, instead of the management of interest-rates, while setting the focus on the control of inflation.

Assuming that the agreements concerning the reopening of the Strait of Hormuz remain in place, we ought to reckon with a sizeable and prolonged phase of lower rates of inflation (representing a sizeable contradiction to the current believes). No doubt, such an environment would propel the world economy on a worldwide spread scale.

A disturbing factor that does not get the necessary attention regards the Russian persisting attacks, not solely concerning the Ukraine, but the entire free world.

CONCLUSIONS

Specific decisions about the effective timing of the economic policy decisions, to come, are tricky indeed, especially taking into account the vulnerability of the current US Administration, as well as the general public focus on inflationary finetuning, by means of interest rate adjustments instead of a pertinent focus on real economic activity. We ask ourselves what is implicitly deducible from the above portrayed chart of the US CPI by means of interest rate finetuning.

The question we ask ourselves at this crossing refers to what is really going on, and what will take place in the near future? When, and on which mutually agreed conditions, will the definitive opening of the Strait of Hormuz really take place is, at this point in time, an open question. Which will the mutual agreed conditions really determine the current investment policy, is the tricky question. A first assumption points towards a rather imminent opening of the impasse. The next assumption points to a rather undefinable path, rendering the forecasting exercise rather difficult. The implications call for a phase of further forecasting insecurity. The primary assumption spoke for less inflation, thus less necessity of monetary policy actions. What about the next step. Any suggestions?

Now after a possible postponement of the opening of the Strait of Hormuz a new question mark arises: When and under which conditions will the opening of the Strait of Hormuz actually take place? Many analysts believe that Central Banks could continue to adhere to an unwritten rule, which implies that “Supply shocks” are ignored and interest rates are no longer adjusted, as monetary policy cannot influence supply anyway. In addition, we fear that, currently, inflation is rising, while economic activity is fragile, while the risk of stagflation is rising. In such an environment we assume that the Central Banks might not be interested in further rising interest rates.

Assuming that not before long the opening of the Strait of Hormuz will really take place, it will undeniably matter, in terms of the future policy implications, to correctly assess the future developments of interest rates, inflation and particularly real economic growth. We deem it worthwhile to define an appropriate investment policy, depending also on the respective currency of reference. The time frame matters, especially taking note of the impending currency adjustments, as a consequence of the specific economic growth propellants: private consumption and fixed investment and this particularly in conjunction with the relative currency of reference.