EMR January 2022

Dear Reader

Wishing you and those you love a HAPPY NEW YEAR 2022

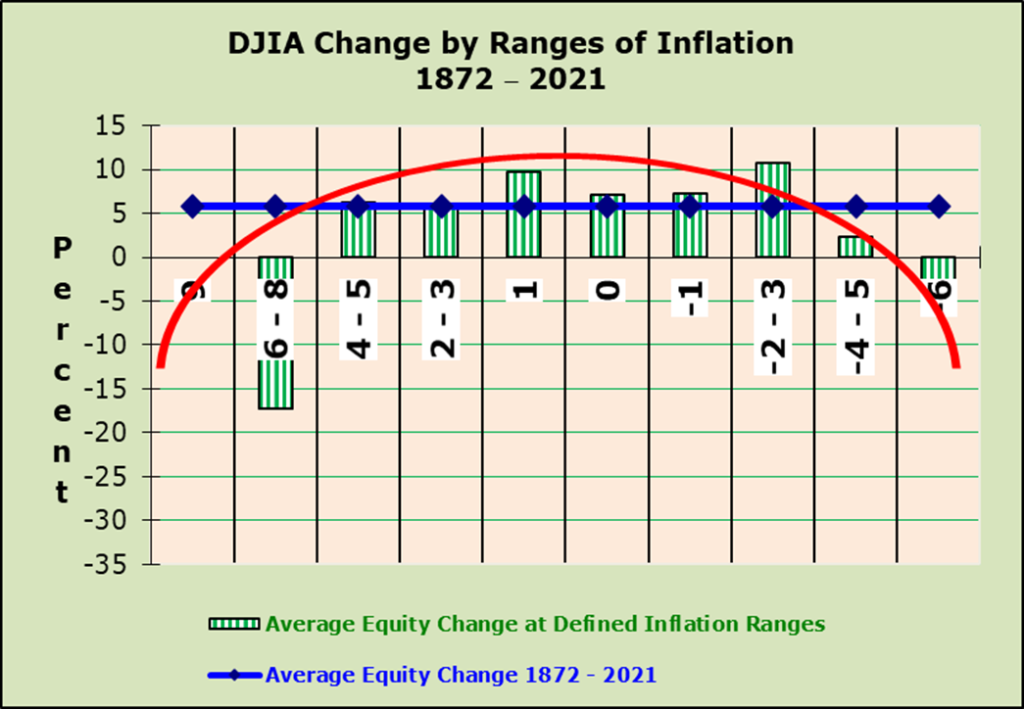

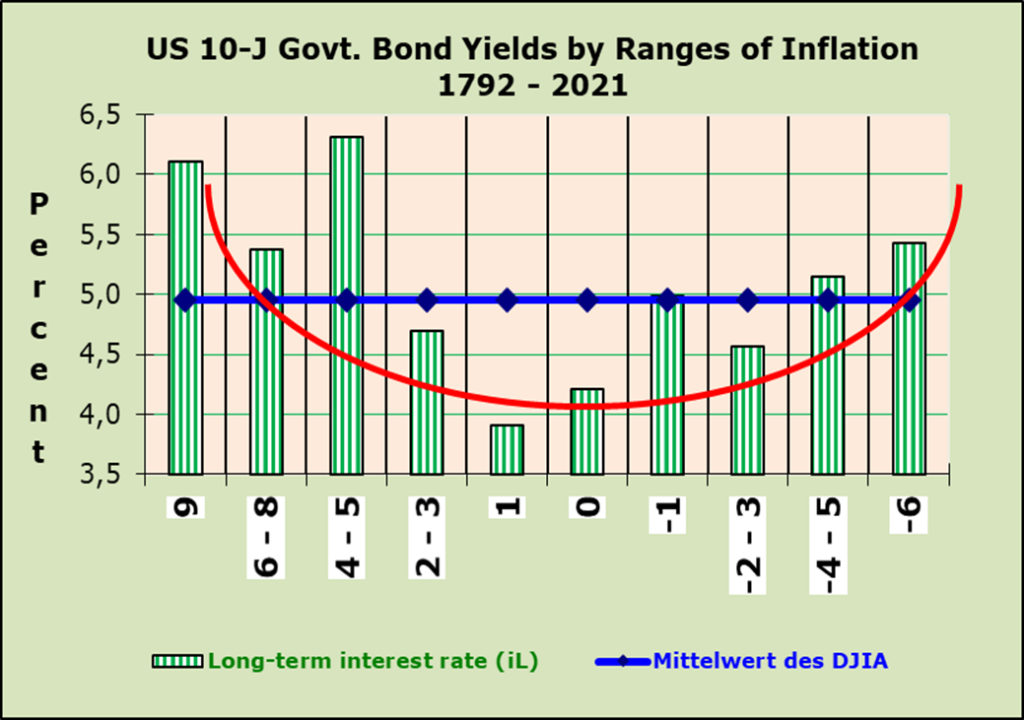

LET US START WITH A PUZZLE: What do the two rather tricky charts below show? Without specific information one cannot interpret the two-inverse developments. In a sense they stand for the situation we are currently facing, while writing about the outlook for the year just started.

Due to long-term data availability, as well as driven by the soaring fortunes of the US-tech giant companies dominating the stock markets, let us concentrate our attention to the US developments. Among the 100 most valuable stock market companies in the world, there are 64 from the USA alone, three more than in the previous year, according to a study by the consulting firm EY. According to the study, there are no European companies in the top ten and only two that are not based in the USA: Saudi Aramco (fourth) and the Taiwanese chip manufacturer TSMC (tenth). Apple, Microsoft and Alphabet are at the top of the list.

What are the expectations for the new year you may ask? Well, let me affirm that in my long career as an analyst, econometric model builder and user and also as common citizen, I have never been faced with such a confusing environment. In order to be set in the position to draw possible or expected conclusions, I will follow the logic of real GDP as commonly portrayed by the equation:

Y = C + I + G + (X – M)

Where:

Y stand for real GDP, C for Personal consumption expenditure, I for Gross private domestic investment, incl. Change in private inventories, G for Government consumption expenditures, and X – M for Net exports of goods and services.

There is no doubt to our mind that all the quoted contents of the equation will be impacted not solely by the Covid-19 pandemic. The principal assumption we make is that all variables stand either as a mover of supply and/or of demand. Three specific arguments are frequently reported in the media. The first and foremost made argument refers to the overall economy, which is expected to lose steam, while secondly prices and interest rates are assumed to increase, i.e. to be pushed up by Central Banks activities. However, the debt trap could force central banks to keep interest rates low in the medium to long term, which could lead to a devaluation of purchasing power that can hardly be offset by bond investments. The third argument relies on the measures to defeat the Covid-19 pandemic. Our contextual assessment is a bit different. We see that the pandemic has reduced and continues to contain the flow of vital productive inputs from low-cost producers to the industrialized world. In this context it must be assumed that the return to normalcy will take longer time than widely foretold. In order to significantly increase domestic production, the industrialize nations require significant increase of manufacturing of intermediate tech-instruments. The primary reason is seen in the “demanding” advancement of non-democratic nations as a price setter. Thus, the focus on the engine of economic activity, and thus of income and employment, ought to be set on “Gross private domestic investments”. The world has become smaller while concentrated on a restricted number of suppliers. Such a development implies a complete change in economic policy both concerning Government spending as well as Gross private domestic investment. For the time being the widespread political view is still focused on redistribution of income instead of increasing production.

Taking current available forecasts of increasing inflation and of interest rates as a starting point, let us now examine the charts of the DJIA by ranges of Inflation and of US 10y Government bond yields and inflation. Telling indeed is the historic comparison of the developments of the DJIA when inflation rises over 2-3% resp. 4-5%. The chart points to an increase of the DJIA of around the long-term average (1872 to 2021) of 5.8%! The chart on the long-run tendencies of 10Y Govt bond yields by ranges of inflation sums, over the period 1792 to 2021 to a rather astonishing similar average of 4.95%, while long-term interest rates rise significantly, both when the rate of inflation is 2-3% (average of 4.69%), topping the increase in the 4-5% inflation range (average of 6.31%).

What do the two charts imply in the current setting? The foremost important assumption refers to the movers of economic activity, i.e. real GDP. The two most tricky assumptions concern the adjustment process of “Gross private domestic investment, incl. change in private inventories” and net Exports.

Gross private domestic investment ought to grow substantially in line with the significant governmental reliquification. Enterprises have learned that international trade disruptions (not just due to Covid-19) but, more importantly, by foreign governmental difficulties, require a readjustment of domestic supply of intermediate technical goods and services. The scarcity of electronic components and the lengthening of delivery times are seen as dangerous growth-limiting arguments; very difficult to be quantified with sizable precision. Nevertheless, the contextual developments ought to yield support to the equity market and local employment.

On the other hand, consumer spending is expected, at least short-term, to be contained as governmental financing is scaled down. Consequently, we assume that real GDP is not expected to rise significantly over the next few quarters. Net export, on the other hand, are expected to support real GDP activity mostly via a systematic reduction of imports of intermediate tech-supplies.

The toxic mix of increasing inflation, consistently due to rising energy costs in conjunction with bottlenecks in the global distribution system and the expected shift in industrial production, will continue to determine the growth differential and trend from country to country.

CONCLUSION FOR THE INVESTMENT POLICY

We continue to focus on equities from both the technology and value sectors. Our relatively positive stance is supported by the following arguments: First, we do not expect central banks to raise interest rates sharply, as there is a widespread expectation that the recent spurts of inflation will subside with the recovery in international trade anticipated for the coming quarters. With a slowdown in pandemic cases, imports of selected technology goods should recover from the devastating effects of the Covid-19 measures. Employment growth is also expected to recover, although short- to medium-term expectations are modest, compared with past economic developments. Consequently, business fixed investment should be the engine of economic activity. Contrary to our assumption, available forecasts continue to assume that interest rates will rise significantly, which would limit the attractiveness of fixed-income securities. The future will show who was right and why.

The toxic mix of increasing inflation consistently due to rising energy costs, together with persisting bottlenecks in the global distribution system and the ensuing shifts in industrial production, will continue to impact the growth forecasts from country to country.

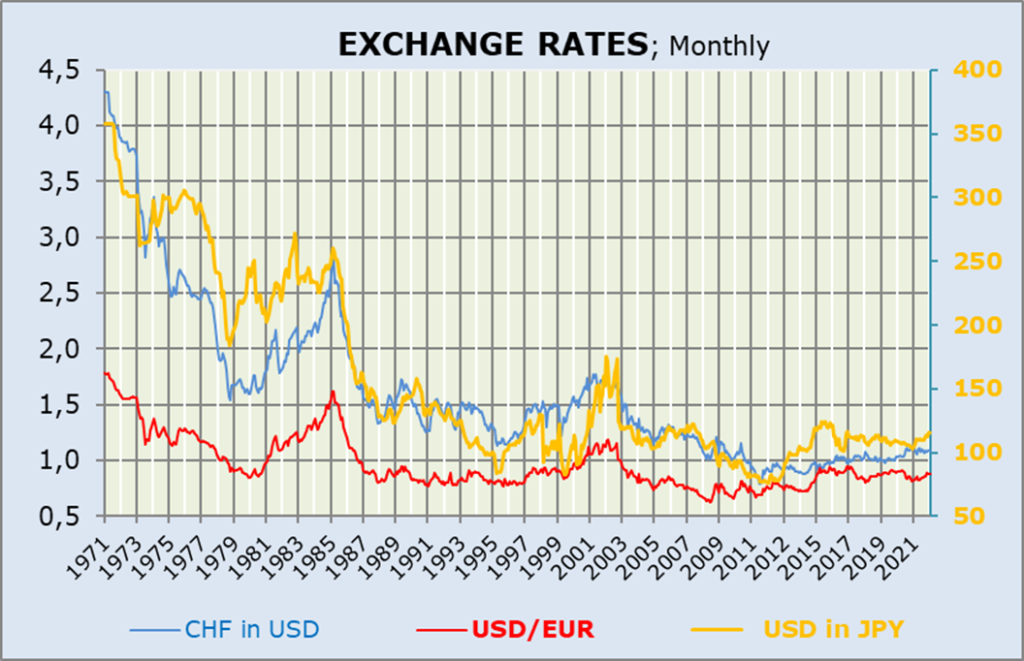

In addition, active managers should also keep an eye on currency fluctuations, even though we do not expect a dramatic change in the CHF/USD exchange rate at this point in time, as foretold by the chart below.

Comments are welcome.