EMR April 2021

In today’s context, economic forecasting is an attempt to predict the whereabouts of the investment environment. Every analyst uses a combination of important and widely followed indicators. In this EMR, we set the focus on real GDP and its major components using them as a guide to find out what the most promising investment strategy might be!

Editorial

Dear Reader The focus of this EMR is on the historic development of Swiss and US GDP and the respective subcomponents, i.e. deterministic variables such as currencies, inflation and interest rates. In our analysis we point out possible discrepancies between widespread expectations and the facts. Given the longstanding differences in the development of exports and imports of goods and services, factual, differentiated outlooks can be derived for economic growth, inflation and interest rates. To be precise we do not find evidence of an outcome, saying that inflation will rise and interest rates will be pushed significantly higher. Taking the flows of imports and exports of goods and services as a primary deterministic factor we arrive at a less pessimistic outlook. Sincerely, Adriano G.E. Zanoni, Ph.D. Chairman

GDP Comparison

Given that GDP in each country is measured in its country´s currency, in order to compare the differential performance, we ought to convert the data with the appropriate exchange rate. Given our interest in the developments of each country vs. another, independently from all factors included, we prefer to use percentage changes of GDP and its respective main components. We then set the starting point to 1 for each variable: GDP = Gross Domestic Product; C = Personal consumption spending, IFIX = Gross private domestic investment, X = Exports, M = Imports and Gov = Government consumption.

It is often claimed that different countries are led by changes and reactions of a “leader country”, mostly assumed to be the USA. Here we specifically examine the connections between the economic whereabouts of Switzerland and the U.S. In the charts, for sake of comparison, we use the exact same scale. We want to know what can we inferred from the following two charts regarding their mutual interdependencies?

Well, a first indication, is that Swiss growth rates differ significantly from those of the USA. Examining the charts, would you argue that the USA has been an important growth factor for Switzerland? The available data for GDP growth, for the period since Q1 1980, sum to 3.735 for Swiss GDP and 2.747 times for the US. The Swiss outperformance sums to 0.998.

Another issue is visible in the differential growth rates of US exports and imports, as compared to the Swiss counterparts. In the US case, net exports have a significant negative impact on US growth, while the Swiss exports have a positive impact on Swiss growth. Swiss net exports contributed to Swiss economic growth, while US net exports have been (and continue to be) a significant deterrent to US economic activity. Statistically spoken, the USA has incurred a sizeable net exports deficit of -77’300.1 Billion of chained (2012 dollars); seasonally adjusted at annual rates!

Influencing Factors

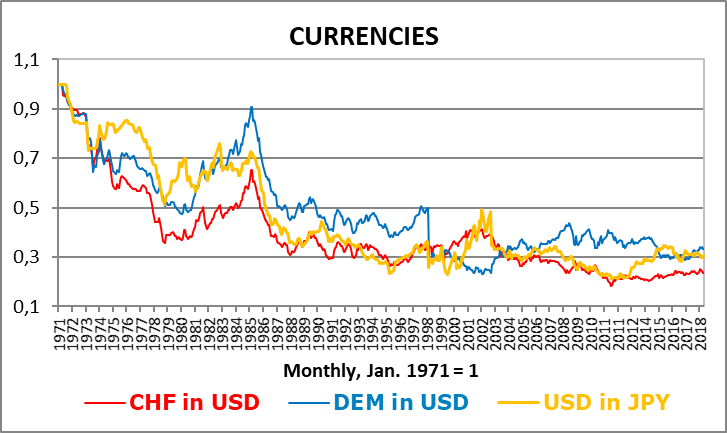

There is no doubt that the depreciation of the USD is not primarily due to political manipulation, but rather as a reaction to economic circumstances, be they of fiscal or monetary nature, or on the part of the business community. The US goods and services trade deficit can and should not continue to increase for too long. Why, you may ask? The hard reality implies that imports of goods and services have for years been higher and growing in comparison to US exports. These developments have been deterministic for the tendential USD devaluation. If the USD falls further, as foretold by vocal analysts, then we may ask: who will play as the lender of last resort? We sense that it cannot be another single country or any international organization in open contrast to a system of “free enterprise”, wouldn´t it?

A further significant influencing factor of economic activity, which currently does not get the due attention, is that a significant, further drop of USD prices of goods and services exported and imported from and to the U.S. would imply a disproportionate and mostly unsustainable change in the economic environment. Who would stand to profit from such a trend-reversal? Opinions hereupon vary significantly, mostly as a function of political points of view, instead of economic reality. The answer, as we see it, must quantify how fast and how much production and employment can be repatriated to the USA?

A further significant USD-drop, as forecasted by many an analyst, would be expected to push prices of goods and services (sold to the US) higher, which would help American industry in its effort to repatriate production. As import prices would be expected to rise, a drop of goods and services imports ought to be factored in. A significant drop in imports will, ceteris paribus, yield support to US economic growth, while e.g. China, Europe and other countries would lose, while US exporters would be the winners.

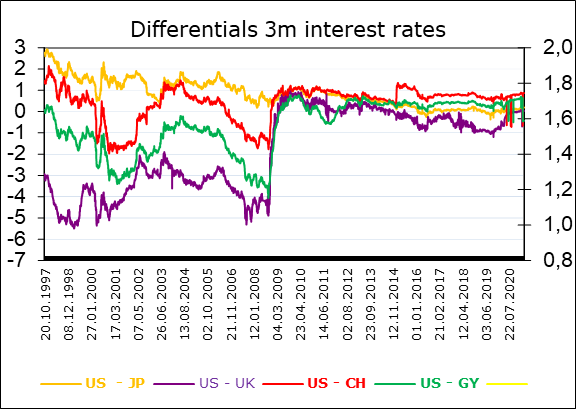

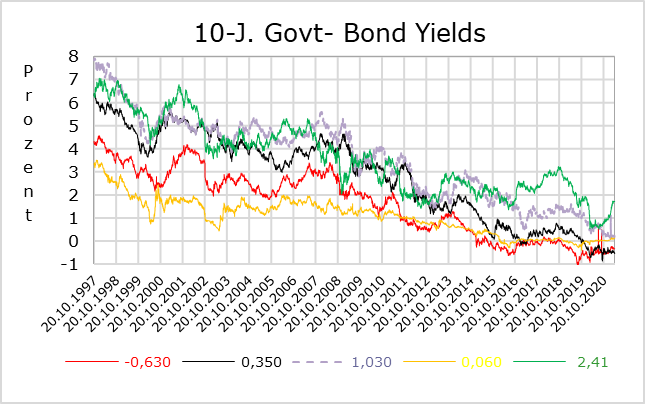

Assuming that, in such a setting, exporters (to the US) would cut prices of goods and services, would call for lower rates of inflation as compared to the generally forecast increase. Let us state that so far, we haven´t heard anybody talking about such a “positive” outlook. Should our scenario stand a chance, we should expect no significant increase in interest rates. A theme that, despite the recent mild increase (while an outbreak from the longterm down sloping trend is not yet visible) would imply that the “revitalization” process of the Biden Administration (1900 billion USD investment program) would favor investment in the US and thus require significantly less need to push prices and also interest rates higher.

Assuming that over the short term, the policy focus ought preponderantly to remain focused on resolving the Covid-19 pandemic, we find it tremendously difficult to forecast a dramatic interest rate increase. The accompanying charts remain difficult to interpret, aren`t they?

Available data do not really facilitate a clear-cut forecast of the major determinants of financial markets´ expectations. Economic forecasting remains problematic indeed and, in some cases, it will remain highly contradictory for some time to come.

Our assessment is primarily driven by the feasibility of a rapid and sustained revival not only of U.S. economic activity through the “reopening” of most vital sectors of the economy. The fact is that the negative economic consequences of Covid-19 have been disproportionately severe and, oddly enough, will remain so for some more time. The corresponding quantitative interactions are foreseeable, and this surely not just for low-wage workers. The interplay of these, rather contradictory viewpoints, should by no means be underestimated while defining the appropriate investment strategy. Coherently, we foresee a period of persistent uncertainty and volatility.

Asset Allocation

Mostly due to the vaccine rollout now on the way, together with the huge US stimulus package, promise a return to economic growth before long. Even if we assume a short-term increase in interest rates, we are confident that “there continues to be no alternative to equities”.

A fact we haven´t taken into specific consideration will continue to be visible in the repercussion of the green-evolution, on inflation and currencies. Prices of fossil fuel ought to be an excellent indicator for short-term inflation expectations, ensuing actions/reactions the Central Banks.