EMR March 2026

Dear Reader

INTEREST RATES & INFLATION?

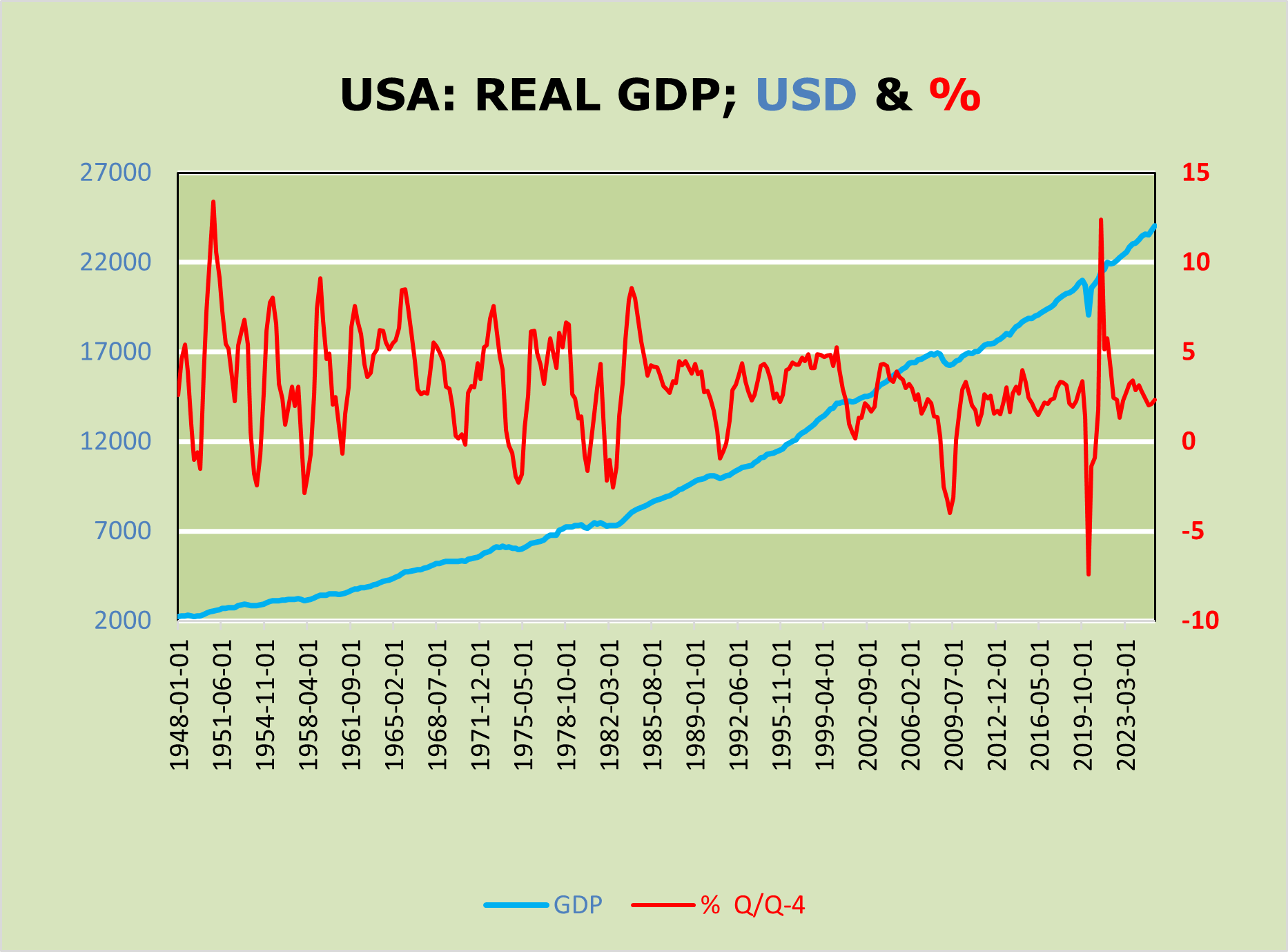

Examining the following chart of long-term US real GDP both on a level basis and on a percent change basis we can infer that, over the longer term, volatili-ty, on average, dropped significantly. The average until 2000 amount to 3.6%, while the average since 2000 amounts to 2.17%. We tale note, that without the turbulences of 2001, the average would be significantly lower. Determining fac-tors that we can infer from the data refer primarily on economic changes as well as of recently on political interventionism.

A determinant for a promising investment policy tells us, that from now on, it will be essential to look beyond short-term political jargoning by the Trump ad-ministration, while focusing on the intrinsic forces of market participants.

From a strategic perspective, we anticipate a further appreciation of the Swiss franc, a relatively stable Euro against the CHF, and a further depreciation of the US dollar against the CHF.

TREND – DETERMINISTIC ASPECTS

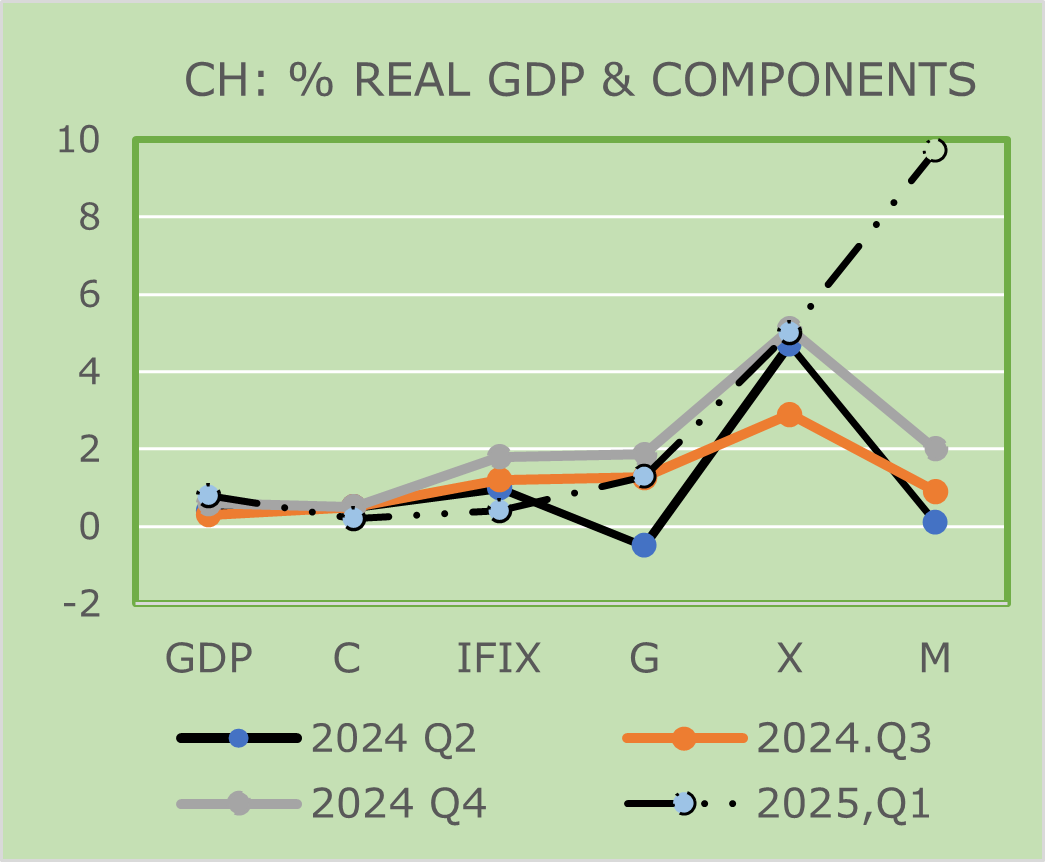

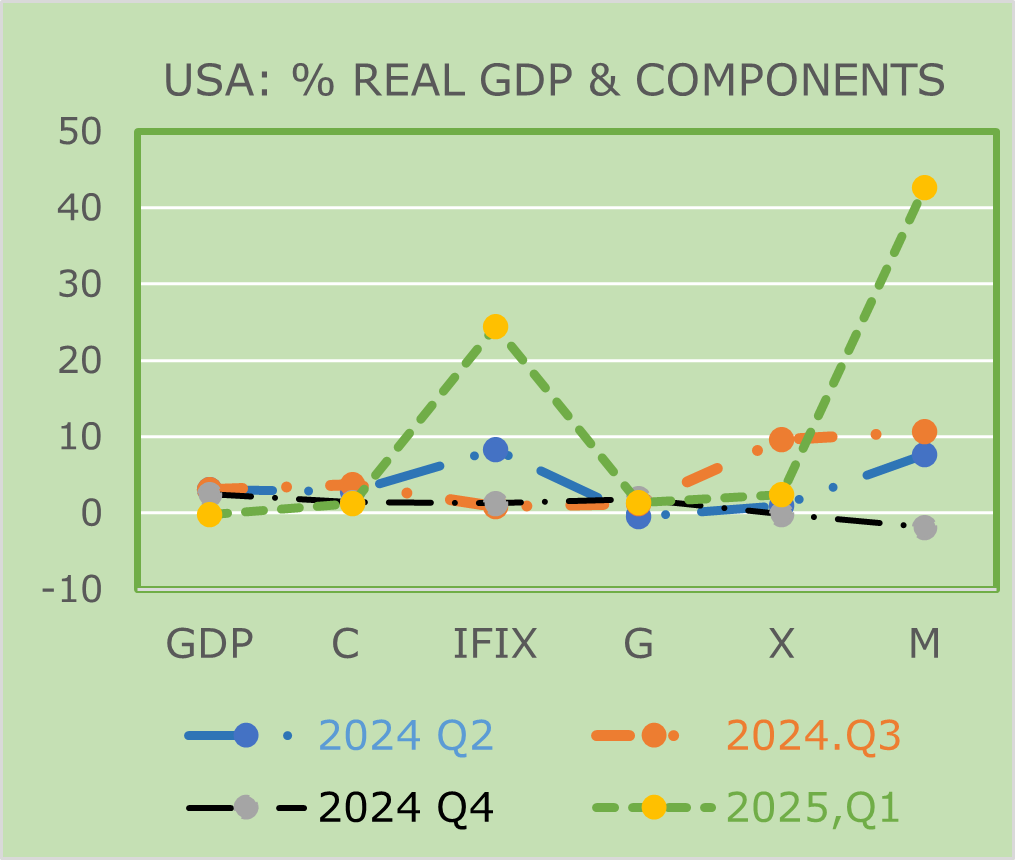

Examining the recent performances of the main components of the Swiss and US GDP data, as shown in the following charts, it is clear that in the Swiss case, public spending and foreign trade played a decisive role, while in the United States the main drivers have been foreign trade (Trump’s measures) and gross private fixed investment. We note that the available data clearly indicate that the impacts in the two countries differ significantly, requiring a coherent fore-casting approach.

ASSUMPTIONS FOR THE CURRENT INVESTMENT STRATETY

The current outlook is truly challenging. To be sufficiently comfortable, we will make the following specific assumptions:

- The first hypothesis concerns the rather confused political agenda of the Trump administration. Therefore, for 2026, we will have to deal with a US administration that might follow a path similar to that of 2025. Assuming that it is not possible to predict changes with a sufficiently high degree of operational credibility, we assume that the US administration will continue to call for interest rate cuts in order to contain inflation fears. Secondly, we as-sume that the persistent weakness of political leadership in Western coun-tries will continue to require considerable attention to their respective do-mestic markets and currency allocation.

- A second deterministic assumption, in terms of asset allocation, concerns the whereabouts of the respective currencies. At present, from the Swiss in-vestor’s perspective, we anticipate a strengthening trend for the CHF. In other words, we anticipate a weakening trend for both the USD and the EUR.

- A third hypothesis concerns the future of technological innovation, which ought to continue to play a decisive role in the asset allocation process.

- A fourth hypothesis concerns the attention to the main components of GDP. At this point, we continue to believe that the engine of economic growth lies primarily in consumer spending and firm fixed investment.

Consequently, our current assessment remains primarily focused on ex-pectations, with greater attention than usual being paid to the domestic economy, currency, and stock market.

SHORT-TERM EXPECTATIONS

We consider the tariffs imposed by Mt. Trump to be the primary determinants of the short- to medium-term outlook, as they undoubtedly represent a tax increase, especially in relation to consumer spending. Let us remember that consumer spending has recently been the engine of economic activity, i.e., the main driver of GDP growth, andd this not only in the United States!

The tariff increases decided by Trump are considered to be as effective as a tax increase. In this context, we should bear in mind that President Trump’s trade policy represents a significant, i.e. deterministic, reduction in the supply of goods and services, with expected negative effects on inflation.

As implicitly shown in the charts above, we consider the historical comparison to be truly astonishing. We conclude that Trump’s opaque tax policy could contin-ue to be an extremely important factor for economic activity and, at the same time, have a strong deterministic influence on the development of inflation, and this not only for the US. We expect significant effects on a global scale.

Consequently, we expect – or worse, we fear – a fairly deterministic warning of a decline in economic activity, caused in particular by consumption and invest-ment spending on a global scale.

SUMMA SUMMARUM

The coming quarters are likely to see a slowdown in economic activity, particu-larly in the United States and, in due course, also on global markets. From an investment perspective, these trend forecasts will undoubtedly be significant. If we assess the situation correctly, they point to a clear HOME BIAS for both equi-ties and currencies. The most promising approach remains DIVERSIFICATION, which currently ap-pears to be the only “free lunch” that holds promise at both the local and inter-national levels

RECENT DEVELOPMENTS

Since February 28, 2026, the escalation between the US, Israel, and Iran has significantly heightened geopolitical risks in the Middle East. At the heart of the economic consequences is the partial restriction of shipping traffic in the Strait of Hormuz, one of the most important bottlenecks in global oil trade. As approx-imately one-fifth of global crude oil exports pass through this route, energy markets are extremely sensitive to any form of blockage or uncertainty. A pro-longed bottleneck is likely to tighten global supply and noticeably increase risk premiums in oil prices. In the short term, a significant rise in prices is therefore expected, particularly for Brent (North Sea oil) and WTI (US crude oil).

Should the situation escalate further, prices above the previous highs of 2025 (>USD 80/barrel) would also be realistic. Rising energy prices would, in turn, generate inflationary pressure and influence monetary policy expectations. En-ergy-intensive industries and import-dependent economies would be particular-ly affected. Financial markets would then experience increased volatility, capital flows to safe havens, and greater currency fluctuations.

The crucial factor for further developments remains whether a rapid de-escalation occurs or whether the disruption of the Hormuz route becomes struc-tural in nature.